by Mish

Only a handful of sites including MishTalk, ZeroHedge, and Jack Dean at Pension Tsunami discuss the problem with any frequency.

On a recent Friday, Dean posted multiple stories on the California Public Employees’ Retirement System, the country’s largest pension program, as well as a budget cliff facing San Francisco, six Los Angeles public safety officers who collected over $1 million apiece last year in pensions, and eight cities that could face bankruptcy when the next recession hits. But the day’s headlines also included the latest on the fiasco unfolding in Dallas, an update on Houston’s less awful situation and features on states that have become the site’s other usual suspects — Connecticut, Illinois and New Jersey. And that was a slow news day.

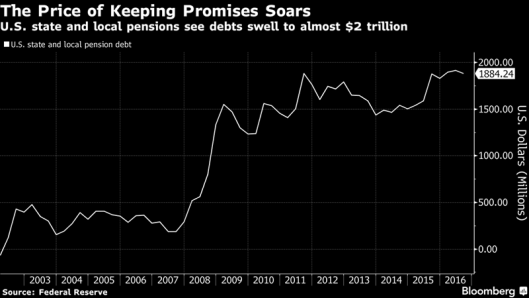

The question is why haven’t the headlines presaged pension implosions? As was the case with the subprime crisis, the writing appears to be on the wall. And yet calamity has yet to strike. How so? Call it the triumvirate of conspirators – the actuaries, accountants and their accomplices in office. Throw in the law of big numbers, very big numbers, and you get to a disaster in a seemingly permanent state of making. Unfunded pension obligations have risen to $1.9 trillion from $292 billion since 2007.

Federal Reserve data show that in 1952, the average public pension had 96 percent of its portfolio invested in bonds and cash equivalents. Assets matched future liabilities. But a loosening of state laws in the 1980s opened the door to riskier investments. In 1992, fixed income and cash had fallen to an average of 47 percent of holdings. By 2016, these safe investments had declined to 27 percent.

It’s no coincidence that pensions’ flight from safety has coincided with the drop in interest rates. That said, unlike their private peers, public pensions discount their liabilities using the rate of returns they assume their overall portfolio will generate. In fiscal 2016, which ended June 30th, the average return for public pensions was somewhere in the neighborhood of 1.5 percent.

Corporations’ accounting rules dictate the use of more realistic bond yields to discount their pensions’ future liabilities. Put differently, companies have been forced to set aside something closer to what it will really cost to service their obligations as opposed to the fantasy figures allowed among public pensions.

So why not just flip the switch and require truth and honesty in public pension math? Too many cities and potentially states would buckle under the weight of more realistic assumed rates of return. By some estimates, unfunded liabilities would triple to upwards of $6 trillion if the prevailing yields on Treasuries were used. That would translate into much steeper funding requirements at a time when budgets are already severely constrained. Pockets of the country would face essential public service budgets being slashed to dangerous levels.

What’s a pension to do? Increasingly, the answer is swing for the fences. Forget the fact that just under half of pension assets are in the second-most overvalued stock market in history. Even as Fed officials publicly fret about commercial real estate valuations, pensions have socked away eight percent of their portfolios into this less than liquid asset class. Even further out on the risk and liquidity spectrum is the 10 percent that pensions have allocated to private equity and limited partnerships.

How Long Can This Go On?

How long everyone can remain complacent over a brewing pension crisis is a mystery.

It will not even take a market crash to cause panic. A major pension fund blowing up could do it. Chicago and Dallas are possibilities.

A recession could trigger a panic, especially if bond yields rise and equities sink simultaneously. A simple earnings scare could cause panic.

Meanwhile, market valuations are the most stretched in history by many measures.

GMO 7-Year Expected Returns

Source: GMO

*The chart represents local, real return forecasts for several asset classes and not for any GMO fund or strategy. These forecasts are forward‐looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Forward‐looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forwardlooking statements. Forward‐looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ materially from those anticipated in forward‐looking statements. U.S. inflation is assumed to mean revert to long‐term inflation of 2.2% over 15 years.

Forecast Analysis

GMO forecasts seven years of negative real returns. Allowing for 2.2% inflation, even nominal returns are expected to be negative for seven full years.

Even +3.0% returns would wreck pension plans, most of which assume six to seven percent returns.

Dealing With Insolvency

Some states have bankruptcy provisions to deal with insolvencies other states don’t. For example, Illinois does not allow municipal bankruptcies even though a number of Illinois cities and retirement funds are insolvent.

Image from Municipal Bankruptcy State Laws.

Congressional Help Needed

To help address the eventual problems, Congress needs to get in on the act because states, especially Illinois, will not do what is necessary.

On March 14, I reported Illinois General Assembly Retirement System Only 13.52% Funded: Overall, Illinois Pension Debt Interest Hits $9.1 Billion Per Year.

Many other Illinois pension plans are among the walking dead.

How about dealing with the problem before panic sets in rather than after?

Mike “Mish” Shedlock