by Mish

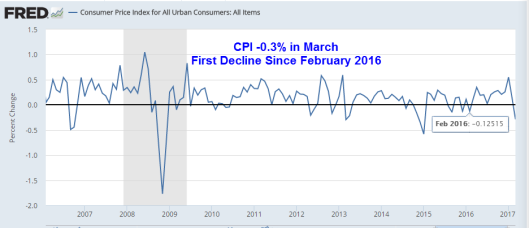

The Econoday consensus estimate was the CPI would be flat, instead, the BLS reports a decline of 0.3%.

This is the first month-over-month CPI decline since February 2016.

Highlights

Yesterday’s producer price report set up the disappointment for today’s report on consumer prices where the headline fell a very sharp and unexpected 0.3 percent in March. The core rate (less food & energy) fell 0.1 percent which is also unexpected.

Energy prices fell 3.2 percent in the month with gasoline down 6.2 percent. But excluding just energy, prices are still in the negative column, at minus 0.1 percent.

A special negative in the March report is communications which fell a very steep 3.5 percent and reflects cell phone plans which subtracted 1 tenth from both the headline rate and core. Yet other categories are also weak including apparel, down 0.7 percent, and transportation where prices, due to weakness for vehicles, fell 1.4 percent. Housing and medical, two centers of price traction, managed only 0.1 percent gains.

Year-on-year rates also moved lower, to 2.4 percent overall for a sharp 3 tenths decline and to 2.0 percent for the core which is 2 tenths lower. An increase for this closely watched core rate was expected.

The lack of price traction ultimately points to softness in overall demand for consumer goods and services. And though demand in the labor market is very strong, wage improvement has been only marginal. A report like this points to the need for steady monetary stimulus and will push back expectations for Federal Reserve rate hikes.

CPI Percent Change From Year Ago

CPI Components

Reality Check

Supposedly, health care commodities are up 3.9% and health cares services up 3.4% from a year ago. Does anyone believe those numbers?

For someone on Medicaid, Medicare, or those with a huge Obamacare subsidy, perhaps those numbers make sense. For those picking up their own insurance, those numbers likely look like Fantasyland lowball estimates.

The same applies to housing where the BLS does not look at actual home prices but instead looks at Owners’ Equivalent Rent (OER). Anyone looking to buy a home and anyone living in an area where rental units are in relatively short supply will have a completely different measure of price inflation than someone living in much of rural America or areas where there are no significant supply constraints.

Supposedly this all balances out. I assure you it doesn’t. Moreover, most prices other than raw commodities cannot be accurately measured in the first place.

Effect on GDP

From the point of view of a Fed that clearly wants to hike at least twice more this year, these are awful numbers. However, benign price inflation numbers will serve to boost real first-quarter GDP estimates.

Mike “Mish” Shedlock