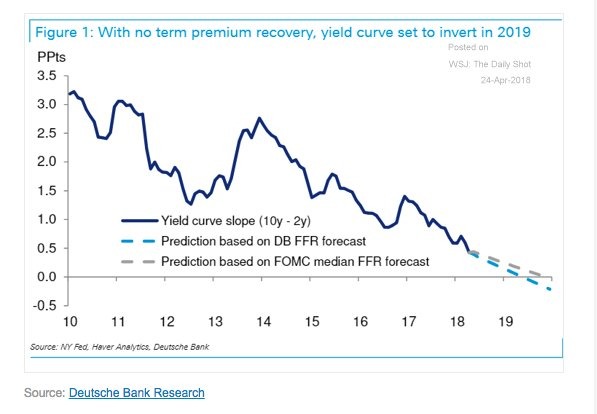

The inversion chart came in a Tweet. I do not have a link to the analysis.

If the Fed gets in 4 hikes this year, I would expect the curver to invert sooner. CME Fedwatch shows a nearly 50% chance of at least four hikes.

It’s also possible the economy falls to pieces and the next move is a cut. Under that scenario, inversion may be a long time coming.

Mike “Mish” Shedlock

They have to get that bond auction off the ground screw the yield curve full speed ahead

CME Fedwatch is not the Fed or based on the Fed. Rather, it reflects bets of futures traders.

The main reason the Fed wants to hike as fast as they can and reduce the balance sheet, is to have some dry powder ammo for the next recession

I believe the Fed, under Powell, won’t back off the pace. There are just too many financial/economic claxtons blaring to ignore any longer if they’re to preserve even a modicum of political independence when it all hits the wall next time.. They’ll go for four, and not so much because the bank casinos and business interests are obviously now addicted to easy money, but increasingly because so many now need a recession’s license for a kitchen sink quarter to close the yawning gap between GAAP earnings and fantasy earnings.

“For progressives the ends justify the means.” Really? For which political block does that not apply these day?

Given that as rates are raised, the PE ratio of stocks will fall, I think that raising rates will accelerate the pension crisis, not post-pone it. It would help a pension fund that was solely invested in short term interest instruments, but hurt one that was invested in stocks, and most likely hurt one that was invested in long term bonds.

Yes, they can artificially affect long term interest rates, too, but it is significantly more difficult for them. Lowering long term rates requires them to buy a large quantity of long bonds, and inflate their balance sheet tremendously. They are trying to do the opposite, normalize their balance sheet somewhat.

The simple act of the Fed “raising” rates back to historical norms does not force an inversion. The Fed can raise short term rates, but if long term rates also rise, there is no inversion. In any case, an inversion does not cause a recession, but, as you said, historically it has been a predictor of them.

And as in prior cycles, the Fed will tighten until “something breaks”. Whether that happens four (+100 bps) rate increases from now or not is the question. I happen to believe that the stock market – and by extension, the real economy – will force them to stop – and then reverse course – after another one or two.

Correct.

The Fed is desperate to reload. It can’t sell, nor will the public accept, negative interest rates after a decade of plundering the savers to restore the TBTFs.

The Fed might want to cause a recession in 2019/2020 so as to lower probability of Trump’s reelection. For progressives the ends justify the means.

THE REASON THE FED IS RAISING RATES IS TO POSTPONE THE PENSION CRISIS. When the sovereign debt contagion starts to spread, which will be obvious with another 1% rise in rates, not to mention the impact of a rising dollar on foreign balance sheets, who would want to own long-term govt paper? When this happens in the next 1-2 years, LT rates will rise much faster than ST. https://www.armstrongeconomics.com/markets-by-sector/precious-metals/gold/gold-v-dollar-3/

Historically, the yield curve inverted for economic reasons and was a good indicator of impending recession, but when it’s forced to invert by fed actions, it’s not.