Point2Homes notes 18 North American Cities Saw Home Prices Jump Over 50% in Just 5 Years

- 18 of the 83 largest North American real estate markets saw home prices jump over 50% in just 5 years. Of the 18 markets with the most explosive growth, 11 are in the US, 6 in Canada, and 1 in Mexico.

- Only 2 cities witnessed a drop in home price compared to 5 years ago, and both are located in Alberta, CA: Calgary and Edmonton.

- San Francisco boasts the highest net increase of all the cities in the study ($550,000), followed by 2 Canadian cities: Vancouver ($417,913 CAD) and Surrey ($395, 287 CAD).

Top Ten North America Price Jumps

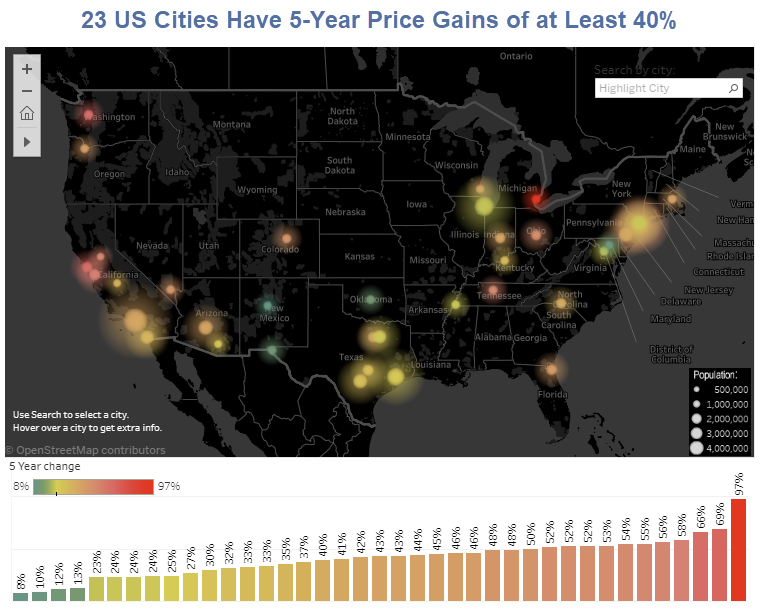

40% and Over Club USA

- Detroit, MI: 97% *

- San Francisco, CA: 69% *

- Seattle, WA: 66% *

- San Jose, CA: 58%

- Sacramento, CA: 56%

- Nashville, TN: 55%

- Bronx, NY: 54% **

- Columbus, OH: 53%

- Queens, NY: 52% **

- Brooklyn, NY: 52% **

- Fort Worth, TX: 52%

- Denver, CO: 50% *

- Las Vegas, NV: 48% *

- Milwaukee, WI: 48%

- Jacksonville, FL: 46%

- Portland, OR: 46% *

- Philadelphia, PA: 45%

- Boston, MA: 44% *

- Phoenix, AZ: 43% *

- Los Angeles, CA: 43% *

- Indianapolis, IN: 42% *

- Staten Island, NY: 41% **

- Charlotte, NC, 40% *

* Denotes member of Case-Shiller Top 20 Metro Areas by size, not price.

** Part of New York City which is in the Case-Shiller top 20.

12 cities in the above list (grouping the NY Burroughs as 1), are in the 40% or greater price appreciation group.

Case Shiller Top 20 Metro Areas

Atlanta, Boston, Charlotte, Chicago, Cleveland, Dallas, Denver, Detroit, Las Vegas, Los Angeles, Miami, Minneapolis, New York, Phoenix, Portland, San Diego, San Francisco, Seattle, Tampa and Washington, D.C.

Case Shiller Top 20 Price Index

Methodology

Unlike Case-Shiller, Point2Homes factors in both new and existing home prices. Case-Shiller only looks at resales.

Sticker Shock

I will ask Point2Homes for an analysis of the Case-Shiller top 20 metro area from the March 2012 bottom to now, grouping NYC as a single entity.

Had Point2Homes gone back one more year, the price gains would have been even more incredible.

Mike “Mish” Shedlock

That Toronto “data” is nonsense. As is Vancouver’s.

At least one house in my desired neighborhood is still 20% below the price paid in 2008. It may have to do with the state being in the top 5 population decrease.

No story here. This part and parcel of the credit cycle. We no longer live in business cycles but in credit cycles. If credit contracts, there will be a big problem. The economy couldn’t handle the threat of the Fed removing support and continuing to raise rates so they stopped. My guess is they don’t hike and let things overheat. Trump will either be the hero or the goat come 2020. There were high hopes for the Fed when Powell was appointed. Now we know he shrank from the task and was read the riot act by someone. Extend and pretend.

One could guess from these charts that there has been an accumulation of high-paying jobs in certain cities — both more of those jobs and higher salaries within them. Software devs start at $60K in Portland easily. That figure would be much higher in the Bay Area and Seattle.

If you are not a fresh faced or recent college grad (under 30),you have close to zero chance of actually getting Hired for one of these jobs. That is the bottom line truth whether or not you want to believe it

It’s true, prices only go up for RE, that’s inflation or dollar worthlessness at it’s best though, because we find homes that are junk, often it’s the land. Then, rural of course as the trend is to move into the cities, or like China does, just build cities! Build it, and they will come. We did trend down some, back when hey bubbled it.

Real estate “going up,” is an artifact of the exact means by which freshly printed money is entered into the economy. Print more money, and prices of stuff goes up. But because, in our particular version of the printing rackets, new money is created by way of credit creation, it is the prices of credit intensive goods that are most affected. Most chewing gum purchases are not financed. Living/working space is.

Then throw in how government is, instead of enforcing anti monopolistic behavior, specifically encouraging and underwriting it wrt real estate, and you end up with the current morass. Imagine the cell phone makers which existed in 1985 getting to vote about whether anyone else would be allowed to build a factory competing with them, and you have zoning/land use laws exactly correct….

So, you have a situation where aspiring competitors are barred from supplying more product despite being able to at a fraction of prevailing prices; while at the same time money is being created out of thin air by the trillions, explicitly by a mechanism that drives up demand for the product noone is anymore allowed to increase the supply of; and you end up with the civilization destroying degeneracy that is the Western “real estate” rackets.

I don’t know about where you live, but around me I watch new houses come on the market at ridiculous prices, then the prices of those houses stay level for about 5 years when the rest of the market catches up with them, then they get on the growth curve.

Thus, from my observations, new houses sell at a premium to the market for similar stock. In fact, the houses being built today are jammed together and on lots barely bigger than the footprint, and older houses have lots usually double the size.

I think that an unimproved 15-25 year old house is the best buy – the money you save on an improved house can be used to improve the house in the style you want.

That is you can find one that a flipper hasn’t bought, fixed then priced it at a premium, I agree the fixer is the best value. Our area has lot’s of homes that are overdone pricing them out of the neighborhood.

Property taxes as well. The total property tax bill on a $550,000 house are easily$12,000 a year on Long Island NY. You have to add on another$1000at least to the monthly principal and interest payment.

In Idiotopia, the dupes are told to celebrate, when they get to pay more and more, for the exact same cellphones and shacks which were cheaper 5 years ago……. That’s how they are told value is being created…

You have a point regarding cell phones – but if you inflation adjust them, they have been pretty stable. Also adjust for productivity gains and they will have decreased in cost, thus they effectively cost less for anybody whose income has kept up with inflation and productivity.

Houses are pretty much the same cost when adjusted for inflation and productivity.

The problem is that in the last 20-40 years there has been a divide in the population – some have exceeded inflation/productivity income growth, some have fallen behind. This is recounted in an interesting book by Charles Murray (yes, “The Bell Curve” guy) titled “Coming Apart”.

Inflation adjusted Apple Phone Costs:

If you can arbitrarily “adjust” anything and everything, you can, trivially, make any statement true. But in the process, you also make it irrelevant.

Try using median per capita, or household, energy consumption as a measure of wealth. Not because Moses came down from Sinai with instructions that this is THE ONE TRUE WAY to measure it. But simply because it is a measure which has always been highly correlated with wealth, and one that is a lot harder to arbitrarily fudge, than any measure which can simply be printed up out of thin air and “adjusted” hither and yonder, in order to look maximally flattering for the guys doing the “adjusting.”

Then, look at cost of a fixed quality of X square foot covered space in San Francisco, measured in terms of this harder to fudge measure of wealth. And similarly, look at the processing power, storage sizes, screen resolution etc.per the same metric… It doesn’t take a Galileo to see which “sector” has contributed to wealth creation, and which one has simply sat on it’s rear, while government and The Fed has redistributed that which others have created in their direction.

Your point regarding sitting on their rear is accurate – but the wealth that is generated by the improvements technology brings has to be spent on things people want – and obviously housing is near the top of most people’s lists.

Another point that has been made here fairly frequently (this being a fairly libertarian crowd) is that housing policy causes an artificial shortage and thus, even things being equal, increased population causes tighter markets.

In a free market, of the kind the one for cellphones still sort of is, people having more money to spend, doesn’t result in them being forced to spend ever increasing sums for the same old decaying stuff. Instead, because suppliers are free to innovate and add to supply whenever they can produce something for less that its prevailing price, both the quantity and quality of cellphones keep improving year in, year out. IOW, they get cheaper and cheaper for any given amount of quality and quantity purchased. And this is exactly what economic growth consists of.

If, OTOH, those who happened to own a cellphone in 1990, got to vote over whether someone else should be allowed to jump in and produce cheaper phones, you would have a pretty much exact analogue of the “real estate” rackets: A few outdated phones, which the already wealthy could then rent out, or sell, for a fortune, to those who needed them. With the government always there to ban new competitors from adding to supply, solely to ensure those who are already wealthy, get to extort ever larger sums in unearned usury from everyone else.

Construction technology is no different from cell phone technology: It improves every year. Making it cheaper and cheaper to keep building the exact same thing, and making it first possible, then economically feasible, to build ever better houses and other buildings.

At the extreme corner case, of congestion so great that it would require a moonshot like engineering exercise to add another floor to the prevailing building height, prices could eventually start to rise despite technological improvements. Just as cell phone prices could conceivably start rising due to running out of sand to make silicone from…

But neither are even remotely the case in any US city. Where the sole reason prices for housing keep going up, is a government always ready to step in and mandate monopolistic dysfunction for the relative benefit of its favorite idle well-connecteds, rather than leave free people to improve the world the way free people always do, whenever they are not explicitly barred from it.

Meanwhile, 5 year return on Gold is right around 0%. Which also, btw, failed once again to break out of its trading range.

As far as I can determine, the Case-Shiller index does not take inflation into account.

To see the above chart inflation adjusted, look here:

Go down to the inflation adjusted chart, clear all the boxes except “USA” and all the hand-wringing disappears.

Put the left coast cities back in and all you see is that the economies of California and Washington State are kicking butt. The rest of the U.S. is just ticking along – no drama.

Also, if you could adjust for productivity gains, the U.S. numbers would flatline. All my life I’ve been told we are in a housing bubble, only once has it been accurate.

Looks like the rest of the country needs them some West Coast style Democratic leadership to get the economy going 😉 [cue MAGA freak out]

Mono, how could you forget to point out the city at the top of the list, which has been controlled by Democrat politics for 57 years now.

That is why I said “West Coast Democratic Leadership”.

Anyway, I was only yanking your chain 😉

No actually the NYC metropolitan area is doing better than anywhere on the West coast and there is somewhat decent public transportation. You don’t need to spend another$800 on car payment and insurance every month

Wow Detroit is up 97%! Looks like you would have to pay $1.97 for a home there now.