The Wall Street Journal claims the Personal Savings Rate is a Surprising Bulwark for the U.S. Economy.

> On the eve of the last two recessions, American households were unprepared. Years of appreciating stock portfolios, rising home values and improving job prospects had convinced consumers that they didn’t need to save much of their income.

> So when unemployment rose and asset prices fell in the downturns that started in 2001 and in 2007, consumers drastically reined in spending and the economy contracted.

> Until a few weeks ago, some economists feared history was in the process of repeating itself. Official numbers suggested saving was again out of style as the current expansion enters its 10th year.

> Recent data has altered the picture. Households have been saving significantly more of their after-tax income for several years, according to revised data released last month by the Bureau of Economic Analysis.

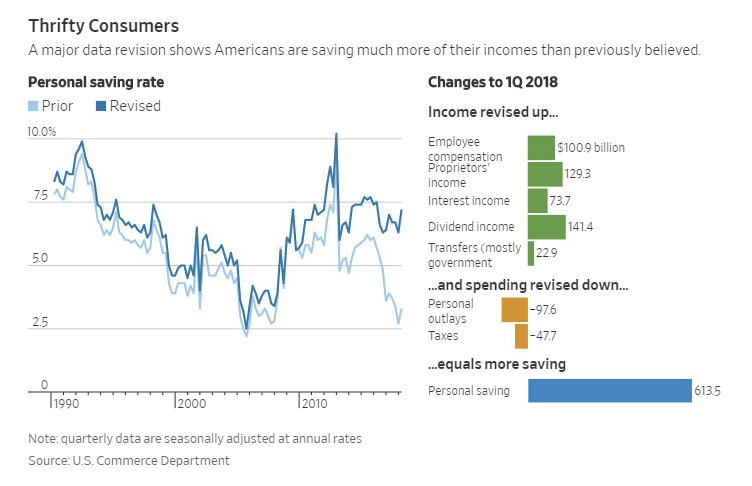

> Take just the first quarter of this year: The agency more than doubled its estimate of the personal saving rate–the difference between disposable income and spending—to 7.2% from the 3.3% estimated previously.

> The new number exceeds the 6.4% average rate recorded since 1990, and is almost three times the most recent low of 2.5% in 2005.

> The first-quarter changes alone amounted to $613.5 billion in additional saving, at an annual rate, recovered from between the statistical couch cushions—enough money to buy more than 20 million Ford F-150 pickup trucks or more than 600 million iPhone Xs.

> While slight adjustments to economic data are common, the revision to the personal saving rate was the biggest since at least 2002.

> “That was an amazing set of revisions,” said economist Joel Naroff, who until recently thought consumers were “largely tapped out” and represented a major risk to the economic outlook. Now, he says, the picture is “a lot less negative.”

Revision Story

Let’s tune into the BEA’s Comprehensive Update: 1929 Through May 2018 report to see what happened.

Personal income was revised up $107.4 billion, or 0.8 percent in 2013; $173.6 billion, or 1.2 percent in 2014; $166.6 billion, or 1.1 percent in 2015; $196.4 billion, or 1.2 percent in 2016; and $401.9 billion, or 2.4 percent in 2017.

That’s an amazing $1.0459 trillion revision.

By Year

- For 2013, the revision to personal income primarily reflected a $118.3 billion upward revision to nonfarm proprietors’ income.

- For 2014, the revision to personal income primarily reflected a $129.9 billion upward revision to nonfarm proprietors’ income and a $44.5 billion revision to personal interest income.

- For 2015, the revision to personal income primarily reflected a $100.4 billion upward revision to nonfarm proprietors’ income and a $70.8 billion revision to personal interest income.

- For 2016, the revision to personal income primarily reflected a $113.2 billion revision to personal dividend income and a $83.1 billion revision to nonfarm proprietors’ income.

- For 2017, the revision to personal income primarily reflected a $143.3 billion revision to personal dividend income, a $111.2 billion revision to nonfarm proprietors’ income, a $100.6 billion revision to wages and salaries, and a $45.9 billion revision to personal interest income.

Who Got Da Money?

- Proprietors Income: $542.9 Billion

- Dividend Income: $256.5 Billion

- Interest Income: $161.2 Billion

- Wages and Salaries: 100.6 Billion

Curiously, that adds up to $1.0612 trillion so there are some small losses elsewhere.

Median Person Q&A

- Does the median person benefit from Proprietors Income? No

- Does the median person benefit from Dividend Income? No

- Does the median person benefit from Interest Income? Perhaps to a small degree

- Does the median person benefit from Wages and Salaries? Yes, but the bulk of income gains went to the high end

Assuming about 25% of the wage and salary benefit and 15% of interest income went to the bottom half, the bottom half got about $49 billion.

I will take a stab that the median household benefit of that $1+ trillion adjustment was in the range of $40 to $80 billion.

Revolving Debt

During the same period as the ballyhooed revisions, revolving debt alone rose by $191 billion.

It is difficult to know the distribution of that debt, but it is the bottom 50% that carries credit card debt every month.

Weather the Next Recession Storm?

This recovery primarily benefited those with assets. The median person does not rent houses or get dividend income.

The “average” person may be better off than in 2013 but the “median” person is likely worse off.

And are these revisions accurate in the first place?

Mike “Mish” Shedlock

I can only guess the savers are all higher incomes, to many scrape by on low salaries. I could be saving an extra $6000 a year, OR driving a nice car if only I would have a living in room mate. Instead I have an empty room that I pay extra property taxes on. Everyone I know doing health care work is literally rolling in it, it’s the one monopolistic sector of our economy that is out of control. They have no choice but to save, sure you can go look at the parking lots of the insurance companies and health care clinics and see they are doing just fine. I put out 10 thousand a year for that, now that’s allot of change for just one single person going out the door. If it were not for those two things, (health care/roof expense) my retirement would be possible, as is, it’s not. Until then work until your dead. I also know many who work so they can have health care benefits, working until 65 is the new norm.

This is how free money and artificially low interest rates are supposed to work: They allow for replacing the debt that the connected foolishly took out to buy assets, with free money stolen from the rest via debasement.

When debt bubbles grow too big to be sustainable, there are only two possible resolutions: 1)Widespread bankruptcy, which clears the debt, but simultaneously returns the accompanying assets to those who were not foolish enough to parttake in the bubble blowing. And 2)bailing out the debt, replacing it with free money. Such that the fools get to keep their assets free and clear, and can start over with borrowing and accumulating. Shouldn’t take a Rothbard to figure out which one is the chosen one in a nation ran by, and for, incompetent fools.

Every civilized society, since the dawn of time, have evolved remarkably similar bankruptcy law. While every late stage Rome, Marie Antoinettistan, Chavezistan and 21st century America have been busy replacing that, with option 2. In order to better entrench their ruling classes’ privilege, so that they can run around calling themselves “job creators” and “pillars” of something other than crass theft.

“Does the median person benefit from Proprietors Income? No.

Does the median person benefit from Dividend Income? No.”

I’m not so sure about either of those “Nos” I know a few people who have rental property, two brothers who run a very busy small business, another former coworker who has an up and coming advertising agency, and I get a fairly good dividend from my employee stock purchase plan (which is outside of a 401(k) and uses after tax money). Sure it is anecdotal, but I don’t have a very large circle of friends and acquaintances. So if I can easily name a few people who fit that category that can’t be a small number.

Seems like it would easy to verify. You can use income tax withholding as a proxy for income and bank deposits as a proxy for savings.

Thanks for your analysis. When I read that article in the WSJ this morning I was worried that I was misinterpreting the US macro economy. Thanks for straightening me out!

I see no reason to assume this data isn’t true. If I were the top 1%, and I am most decidedly not, how many yachts and houses do I actually need? I’m thinking maybe four yachts and 10 mansions at the most. A couple of Gulf Streams might be nice too, but at some point, I’ve got enough stuff. And, with everything at peak asset price, keeping the extra billions in the bank might just make sense.

“Until a few weeks ago, some economists feared history was in the process of repeating itself.”

History always repeats itself. The question is always the timing. There is a recession coming. They always come. It is a cycle.

Do the increased savings matter, if the G20 changed the rules for depositors and made us unsecured creditors to the banks, when X% of banks go under at the end of the current expansion? What does being prepared matter if the savings are confiscated as being bank capital, by failing banks?