by Mish

Durable goods in April fell 0.7% vs an Econoday consensus estimate of -1.0%, but the good news (if you call that good news), stops there.

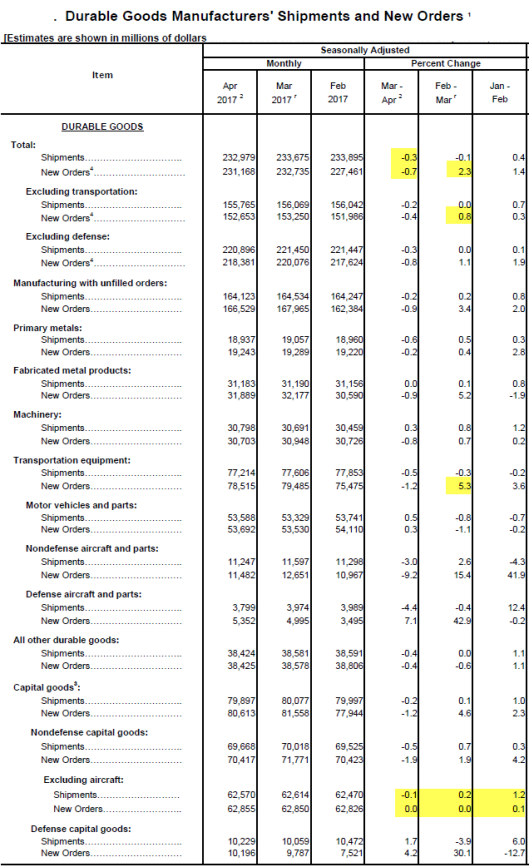

Highlights

Yet another piece of the second-quarter puzzle is not favorable. Durable goods orders, down 0.7 percent in April, do not confirm the month’s big jump in industrial production nor all the strength in the regional factory reports. Aircraft is not a factor in today’s report as the ex-transportation reading is also negative, at minus 0.4 percent which is well below Econoday’s low estimate. Also below the estimate are orders for core capital goods (nondefense ex-aircraft) which came in unchanged following a downward revised unchanged reading in March.

Manufacturing output soared in the industrial production report but shipments in this report fell 0.3 percent and follow March’s 0.1 percent decline. Shipments of core capital goods, which are an important input into second-quarter GDP, also fell 0.1 percent. And the weakness in capital goods orders does not point to shipment strength in June or July.

Inventories edged only 0.1 percent higher but, given the decline in shipments, the inventory-to-shipments ratio moved one notch higher to a less lean 1.69. A plus in the report is unfilled orders which, after long contraction, have put together two straight positive months, at 0.2 and 0.3 percent.

Regional Manufacturing Strength?

Econoday cited strength in the regional factory reports. What strength is that?

- April Empire State Manufacturing Survey: Empire State Manufacturing Survey Turns Negative: Welcome News?

- April Richmond Fed Index Plunged from 20 to 1: Is the Manufacturing Growth Slowdown No Longer Welcome? Already?

Durable Goods New Orders and Shipments

Despite the upward revision in new orders to 2.3% March, this was a weak report. Excluding transportation, new orders in March were up a more modest 0.8%. Excluding transportation, new orders in April fell 0.4%.

Shipments, which feed into second-quarter GDP were negative.

Core capital goods (non-defense capital goods excluding aircraft) were very weak. Core capital goods are a measure of manufacturers’ willingness to expand.

Aircraft orders play out over many years and will not affect GDP in upcoming 2017-2018 quarters.

The second quarter is off to a very weak start.

Second Quarter Reality

- April Durable Goods shipments down 0.3%, new orders down 0.7%: April Durable Goods: Yet Another Weak Second-Quarter Report

- Wholesale Inventories: Down 0.3% in April. March revised lower from 0.2% to 0.1%.Retail Inventories: Down 0.3% in April. March revised lower from 0.5% to 0.3%. For details, please see Fed Eyes Second Quarter Recovery, Expects Trump Fiscal Policy Will Expand Economy

- Trade deficit in April widens by 3.8% with exports down and imports up: Trade Deficit Widens, Exports Weak: Economists Miss the Mark

- Tax Receipts: Federal Tax Receipts Running Below Expectations

- April New Home Sales: New Home Sales Contract 11.4%: Sales Barely Up Year-Over-Year

- April Existing Home Sales: New Home Sales Contract 11.4%: Sales Barely Up Year-Over-Year

- April Existing Home Sales: Spring Housing Flop: Existing Home Sales Decline 2.3 Percent, Inventory Issues Persist

- April Housing Starts: About that Strong April Recovery: Housing Starts and Permits Flop, March Revised Lower

- April Empire State Manufacturing Survey: Empire State Manufacturing Survey Turns Negative: Welcome News?

- April Retail Sales: Sales were at least positive (+0.4%), but they were well under economists projections: Retail Sales Disappoint Again: Department Stores Clobbered in 2017

Mike “Mish” Shedlock