A Federal Reserve Bank of San Francisco (FRBSF) macro economic letter discusses the Yield Curve and Recessions.

Here is the paragraph that caught my attention.

“Recently, Engstrom and Sharpe (2018) have argued that a spread of short-term Treasury rates—the difference between the six-quarters-ahead forward rate and the three-month yield (forward6q–3m)—might be preferable as a [recession] predictor because it focuses on expectations of the near-term path of monetary policy.”

I do not know where the SF Fed came up with the six-quarters-ahead expectations data, but but it exactly matches a 2-year forward rate minus the current 3-month rate.

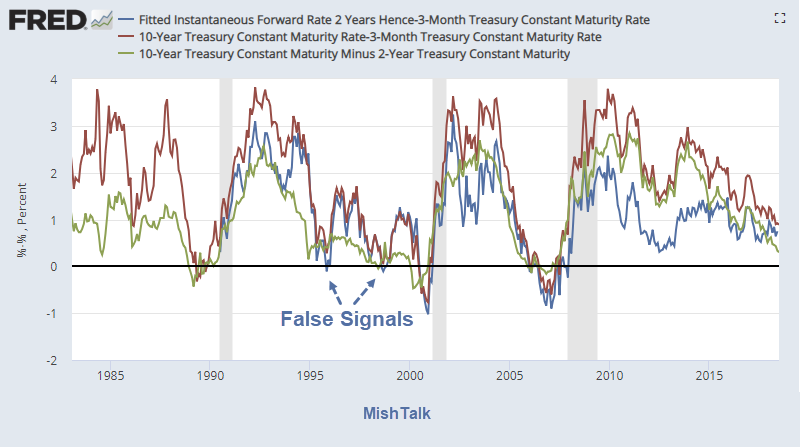

Spreads vs Recessions

Predictive Power

False Signals

The problem with the idea of using forward rates as a recession indicator is the false signals they provide.

I added the two main ideas in the SF Fed letter to the spreads vs recessions chart I created the other day.

Spreads on August 27, 2018

- 10-Year Minus 3-Month: 0.73

- 10-Year Minus 2-Year: 0.19

- 10-Year Minus 5-Year: 0.10

- 10-Year Minus 7-year: 0.04

- 5-Year Minus 2-Year: 0.09

- 2-Year Forward Minus 3-Month: 0.75

The latest data for point 6 is June 29, updated July 10.

On the basis of points 1 and 6, a recession may be quite far off. Then again, there is no guarantee the yield curve inverts before a recession hits.

For further discussion of the San Francisco Fed macro letter, please see San Francisco Fed on the Predictive Power of Yield Curve Spreads.

Mike “Mish” Shedlock

Any attempt at pretending economics is some form of a “data driven” undertaking is mindless bunk from the get go. Knowledge that The Fed is altering the environment based on ANY indicator, always and inevitably result in economic actors optimizing for this, until all predictive value of the indicator in question is squeezed out. Were it not so, central planning of the economy would be a net positive undertaking.

We are in a permanenent (as in never ending) “recovery”,recession are a thing of the pass,the unemployment “rate ” will never rise again (ever)ie a permanent low unemployment…..”rate”,GDP “rate will never be negative again (ever),inflation “rate” will never rise again in any meaning ful way.Central banks will take complete and total control of well……….everything,they will eventually print enough money and own all share in the S&P AND Nasdaq,own all bonds,all etf’s all retirement accounts all commodities and last but not least …..they’ll own YOU!