A battle looms over ‘business interruption’ coverage, which insurers say doesn’t apply unless there is physical damage, like from a fire, unless there is specific coverage for pandemics.

One of the biggest legal fights in the history of insurance has begun.

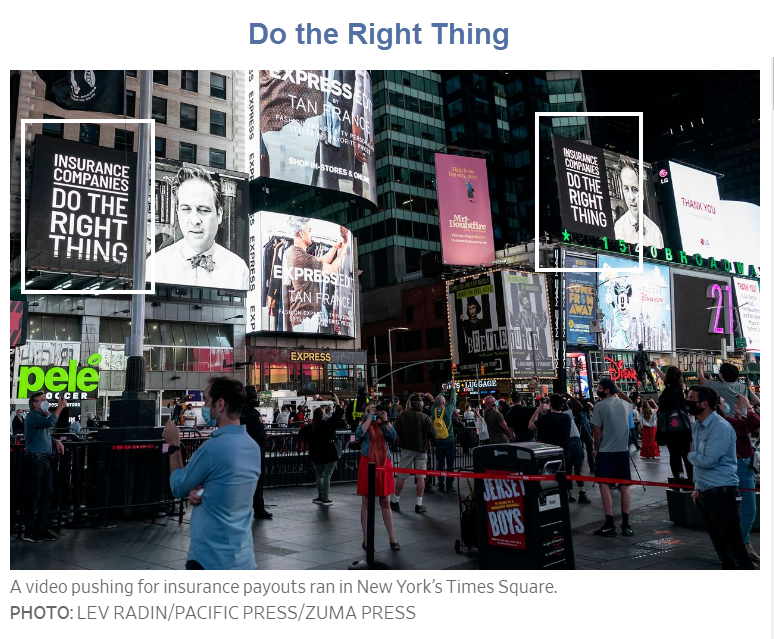

A cavalcade of restaurateurs, retailers and others hurt by pandemic shutdowns have sued to force their insurers to cover billions in business losses. A video berating the industry ran for most of June on a giant screen in New York’s Times Square, four times each hour around the clock.

“Insurance companies: Do the right thing,” was the chorus at the end of the video. Repeating the words were a musician, a dancer, a chef, a rabbi, comedian Whoopi Goldberg—and a New Orleans plaintiffs’ lawyer, John Houghtaling II, who paid for the video.

More than half of property policies in force today specifically exclude viruses. The firms filing the lawsuits mostly hold policies without that exclusion. Their argument for getting around the physical-damage requirement is that the coronavirus sticks to surfaces and renders workplaces unsafe.

What’s the Right Thing?

Logically speaking, the claimants do not have a leg to stand on. If policies specifically exclude pandemics or viruses, that should settle the matter.

But the amounts are huge. People and corporations will sue over anything.

How Will Sympathetic Courts Rule?

That is the key question.

And no one knows how a sympathetic court will rule.

Unfortunately, we will likely see different answers in different states. Some of it may depend on the answer to the question: How deep are the plaintiff’s pockets?

What About Riot Insurance?

Will “riot insurance” exclusions come into play in the wake of George Floyd riots.

Of course. That will be a battle too, but a much smaller one.

Something for Nothing

The right thing is to quickly honor claims of anyone for businesses with insurance and quickly refuse claims if there is a virus or pandemic exclusion.

There may be some policies that do not fit either criteria.

But expecting insurance companies to voluntarily pay up where there is an exclusion rider is ridiculous in these eyes.

If you want insurance to cover something, generally you have to pay for it.

Nonetheless, a monstrous legal battle has begun. And it is poised to get much worse.

- Drinking Banned at Florida Bars and What About the NBA?

- Texas Shuts Bars at Noon as Covid Cases Surge

- Please Don’t Breathe in the Elevator

Mish

“How Will Sympathetic Courts Rule?”

Arbitrarily. How else?

“Courts” just about may work as a means to resolve fairly clear cut and limited disputes. But the purely ambulance chaser boosting delusion, that they’re some sort of universally valid mechanism for refereeing all and any happening in the universe, is exactly not in any way whatsoever any different from the delusion that five year planners and Dear Leaders are.

Ditto “insurance.” A “Pandemic,” in the abstract, is in no way an insurable event. Extremely narrow, specific effects of something somewhat related to what many would call a pandemic, may be. And such a contract could hence be adjudicated in a court. But in those cases, the contracts would be too technical to garner headlines.

Even treating “pandemic” insurance, in the general sense, as anything fit for court adjudication at all; which is a prerequisite for mindlessly babbling over what it maybe just perhaps could “mean”; only serves to grant even more arbitrary redistribution power to kangaroo courts, than they already have.

The dudes who bought it, got scammed. Sucks to be that gullible, I suppose. If whoever sold it to them, violated any laws, hang them. If not, don’t be such an easy mark next time. Now quit wasting the time and money of the taxpayers whose taxes fund these courts, and go do something useful instead. Which aggrandizing ambulance chasers, and self proclaimed experts at interpreting Newspeak, is exactly not at all.

Dow 5 million?

Here is an interesting article link to wired.com . Pandemic Insurance to be underwritten by pension funds (for obvious macabre reasons), that basically no one bought.

A lot of the policies I’ve seen without specific pandemic exclusions are actually business property insurance policies with business interruption riders. The rider specifically covers business interruption caused by damage to the property.

For example, if your building burns down, not only will insurance cover the cost to replace the building, but lost earnings while it is being rebuilt. Without a property damage claim a business interruption claim cannot be made.

Legally, I do not think the small businesses have a leg to stand on. Courts care less and less about what is legal though, so who knows.

QUOTE: “Aloha,

From Hawaii, where all the measures ARE working. Contradicting information, this place is safe, this place isn’t, blah blah. The measures aren’t working, we need a new plan. We, in Hawaii, seem to have herd immunity from that line of thinking. We stuck with common sense. We didn’t push for haircuts as a necessity(buy a pair of clippers). I have never seen a person without a mask in public in an enclosed public space. Visitors are allowed but with a 14 day quarantine so next to none have come with the exception of a few from “the mainland” who you guessed it, immediately broke quarantine. But, ALL were arrested and given a one way ticket, paid for by the Hawaii tourism authority, off island. No one is protesting mask rules. No Karens. Unfortunately we are recognized as a state in the US, even though we are under an illegal military occupation.(study it, you’ll see).

I am with you! Sovereign Hawaiian nation!!

everything feels so new nowadays — new dilemmas, new battles, etc.

I think property damage is correct. However, once a property is disinfected, it is to the owner to be sure it does not become damaged again. If that means not accepting customers due a lot of them damaging property, that is the way it is, and that means the business closes. You might take that one step further, and say customers have become a danger to the property and therefore the business is under siege, as per a riot circumstance, and must close, with or without redemption.

This is just arguing out the logic, free to take that further or oppose, there is no judgement meant.

…Many organizations have “Business Interruption Insurance,” which covers loss of revenue when a business is forced to suspend operations. “Civil Authority” clauses may also be present in policies, which cover losses specifically in cases where government agencies temporarily close businesses.

However, following the SARS outbreak in 2003, many insurance companies adopted a standard exclusion in their policies for viral pandemics. Furthermore, business interruption claims typically require evidence of property damage if they are to be granted. It is an open legal question whether property can be considered damaged as a result of exposure to the virus….

NY legislature trying to turn back time…

The crucial question is going to be whether the government mandates are included in the business interruption policy. Pandemic doesn’t have to factor in. Next question is to what extent governments can be sued for damages their policies have incurred.

Sovereign immunity protects the government from lawsuits unless the government has specifically authorized a lawsuit against itself, for example civil rights actions under USC 1983. I doubt authorization for lawsuits related to damages for government policies during a pandemic has been authorized.

“Nonetheless, a monstrous legal battle has begun. And it is poised to get much worse.”

…

Re commercial leases. If governor closes businesses, does tenant pay, or not?

No one wants to take the loss. Impending suits will be epic … in many cases a business’s survival at stake (including the insurances’).

A golden age is dawning for lawyers

Yes. And a drawn out affair. I foresee many businesses going under in the interim. They need cash flow NOW.

You’d think the insurance companies would have priced pandemic risk into that policy. It’s been known for years that this was going to happen, and there were probably even decent risk models.

Maybe they decided all that analysis would just make their policies more expensive, and harder to sell. Why bother with that?

They did indeed factor it in. They wrote riders excluding it unless someone paid for it.

So I guess the rioters were doing the business a favor when they burned them