Seven-Year Loan Surge

America’s middle class can’t afford its cars.

A surge in the Seven-Year Auto Loan rate provides all the evidence you need.

Walk into an auto dealership these days and you might walk out with a seven-year car loan.

That means monthly payments that last well past when the brake pads give out and potentially beyond when the car gets traded in for a new one. About a third of auto loans for new vehicles taken in the first half of 2019 had terms of longer than six years, according to credit-reporting firm Experian PLC. A decade ago, that number was less than 10%.

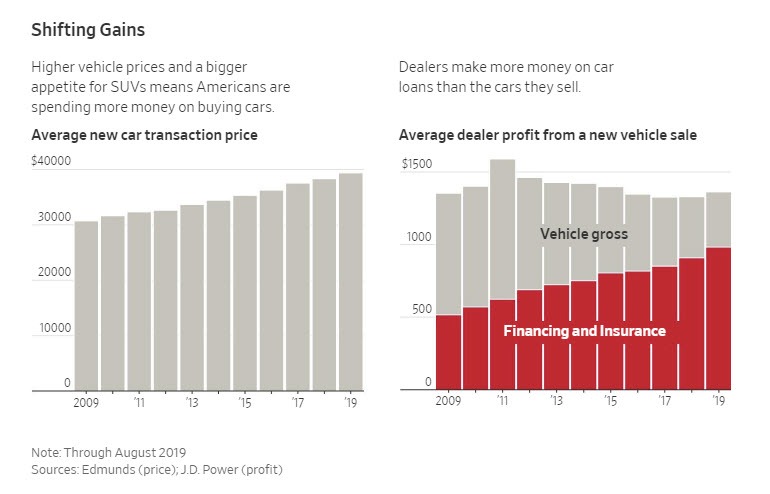

Incomes have risen at a sluggish pace in the past decade, but car prices have grown rapidly. A lending machine has revved up in response, making it possible for more Americans to procure a vehicle by spreading the debt over longer periods. Wall Street investors snap up these loans, which are bundled into bonds. Dealers now make more money on the loans their customers take than on the cars they sell.

Families Go Deep in Debt to Stay Middle Class

On September 9, I noted Families Go Deep in Debt to Stay Middle Class: Revolving Credit Jumps 11.2%

These are signs of a “Late Stage Credit Bubble“

Ability to buy things one cannot really afford does not make or keep someone in the “middle class“.

Wages are not keeping up with needs and desires.

Collectively, these reports show a late stage credit bubble the Fed desperately wants to keep inflating.

Mike “Mish” Shedlock

Agreed link to thesocietypages.org

That means monthly payments that last well past when the brake pads give out and potentially beyond when the car gets traded in for a new one .

Yes, now there are a lot of tendencies to changes in the field of cars, because really very often I am asked about it. It’s also good that I’ve already managed to understand how best to make a car to look cool and solid. Of course, if you take the same tint, then you still need to legally understand the norms of acceptable, because there is a very serious matter and you should definitely study this article link to avtotachki.com , it describes the pros and cons of tint and in general how it takes place or not. It is up to everyone to decide, of course, just to understand whether you need it and what you will be for it. So think about it a few times. I already know friends who are “flying in” for this. But if you act carefully, you will have an indescribable pleasure. So be sure to study this article, I think you’ll learn a lot about tinting in general, how to do it correctly, and of course it is worth it or not. Good luck!

I totally agree with you. You have highlighted the car Dealers blackmailing. Most of them try to sell their cars via loan. Do you know Mazda 3 will be equipped with a turbocharged power plant. Such information was shared by a source who is familiar with price lists for official used car dealers carzaamin.com of the brand for 2021. The Japanese company Mazda is preparing new modifications for the Mazda 3. One of the main innovations may be the emergence of a turbocharged engine and all-wheel drive system. Such information appeared on the web on Thursday, June 4. Recall that the last time a turbo engine was installed on the Mazda 3 back in 2013. Then it was essentially a different car, which for 7 years has changed very much both externally and in terms of technology. Thanks

People here are overthinking things. What insurance are these dealers selling that rakes in the profit? Back up and think about the last time you bought a car. Did they try to sell you insurance against maintenance (i.e. extended warranty)? How about insurance against glass breakage (i.e. glass protection package)? Perhaps insurance against paint failure? These are all very high profit for the dealer.

I took out a six year loan on my car since the rate was about 1% and I (correctly) figured I could do alot better that 1% in the stock market. Low interest rates might be a factor although I wouldn’t doubt it’s mainly because of flat wages.

Most Americans don’t know how to budget or plan for the future. Why would anyone with minimal financial acumen want to get into a 6 or 7 year loan. It doesn’t make financial sense to own a rapidly depreciating asset for that long of a period. It won’t be worth very much when trading it in 7 years later, not to mention the cost of repairs on an aging vehicle.

Perverse incentives will do that. The middle class is rewarded with toys for being irresponsible, and does not notice the debt noose that is tightening around their own collective neck — as taxpaying participants in a system that will eventually implode to far lower living standards.

I’d like to propose that “families se for go deep in debt” to stay at the middle to upper of the lower class vs middle class. They just want the “illusion” of middle class. 500k home, new cars, stainless fridge, 50 credit cards and no money in the bank. My neighbor just sold his house for $600k to a couple with 3kids that put 200k down. In the 3 months they’ve been here ive seen them in the yard twice. They are at work all the time.

I recently traded my 10 year-old pickup for a new one. They are ridiculously expensive, but it will be my last truck purchase (age). After the negotiation on price (a $12,000 discount), the dealer offered another $5,500 off if I would finance it over 6 years with GM at $600 per month. I had intended to pay cash, but $5,500 is good money. The dealer told me that I only had to make 4 payments and then I could pay it off if I wanted to. Looks like the dealer screwed GM on this one.

The real question is can you return more with your cash over 6 years than the interest. The answer is in the most cases yes. A lot of it depends on your timelines, capital at risk and rates of return over the next 6 years along. To me it is better to pay things off as markets peak and then use cheap loans as markets become undervalued. My car loan is 0% and has been since we bought it in 2015. There is no incentive to use cash to payoff the loan.

Generally, I agree with you. In this case, the GM interest rate is 5.1%, so I’m either paying it off or refinancing it at a lower rate at the credit union.

Not mentioned is leasing. Another tool to get people into new vehicles they can’t afford. Edmunds recently reported that a RECORD number of new vehicle sales are leased … 32% of sales.

I think this has more to do with people becoming small business owners and writing off every expense possible. Real estate agents and other small business “professionals” do this.

This explains a lot. A few months ago I bought my son a new Kia Optima. We went to a few dealerships and eventually was given the best price. They then went into how I could finance it. I told them I was just going to write a check for the whole thing. They were shocked and desperately wanted me to finance. They told me it would be less expensive. Which of course I knew was BS. I assume they gave me the lower financing cost instead of the cash price. The car had a msrp of $28k and I paid $23k. After taxes, destination charges, processing fees, etc… I think they took off close to $8k.

Last time I bought a new car, I asked for a loan, and acted to the loan guy like I was a dummy who is fixated on getting a lower sales price while being oblivious to credit costs. He did his car-loan-guy thing and moved their profits from the sales price and into the interest payments. I smiled and thanked him. … Then I paid off the loan in 1 month. Sounds like you played it better and more direct.

Here’s how you buy a new car. Find the one you want and offer $5000 less than asking, up to $10,000 on a higher end car. That’s too much, but it provides some room for negotiation. Let them know you want the longest terms possible on a loan. That way they’ll be happy to negotiate a lower sticker hoping to get their money on fees. Once they draw everything up, tell them you’ve decided to pay cash instead and write a check.

If you can’t write a check, don’t ever buy the car.

LOL, or negotiate hard and then get a zero percent loan. I dont get my last car purchase. I was ready to pay cash, but got confused when they gave me a 29k sticker car for 21k and a zero percent loan? I just took the loan, first loan Ive had since my first car. I doesnt feel like a loan though. I’m not paying interest, I have the cash to pay it off completely 10xs over, but why?

“Wall Street investors snap up these loans, which are bundled into bonds…”

“…and subsequently sold to banks who collude with each other to bid up prices and inflate their respective balance sheets until they start calling BULL on each other in the repo market…”

Don’t worry though, because in the end, the Fed will bail all the players out by buying their garbage at face value in the name of “helping the economy.”

Bam. Hit the nail smack dab on its head. The economy is so screwed up by it all.

Anything possible.

But Article 14 of Federal Reserve Act specifies what is eligible for purchase by Federal Reserve. Consumer loans (and a lot of other stuff) are not eligible.

Federal Reserve would need for Congress to amend what FR can purchase.

The Fed would never buy consumer loans directly. It is much more effective to overpay enough for plantation MBS’, such that privileged and connected plantation owners can then afford to whip more slaves around, in exchange for enough bread crumbs to minimally service the slaves’ consumer loans.

Seven year auto loans. Thirty year mortgages. Unpayable student loans. Paycheck to paycheck credit card debt. And now the young are buying into “The Everything Bubble”. The FED has helped create Debt Slaves. Call it what it is.

The big 3 will all need fresh bailouts,banks will also need massive fresh bailouts,Fannie /Freddie will need fresh bailouts,state pensions will need a massive bailouts,2020 will be the year of the (collapse) bailout!

Lurking underneath the whole pricing scheme of US auto industry is the 25% tariffs on foreign trucks that was imposed in the 1980s. It served to jack the prices across all cars and trucks.

If only our society had an institution that would educate the population on basic math… one of those school thing-ys that we sometimes hear about in history documentaries. Then Joe and Jane Q Public could understand mortgage and car loans enough to make intelligent choices…

Lots of people like to talk about how US healthcare costs are out of control, but our health outcomes aren’t as good as countries that spend half as much.

Check out health inflation in the chart… then check out education and textbooks

Interestingly enough, the clowns at the BLS claim that new car inflation is pretty close to zero.

When the road you travel is covered in tire popping neglected pot holes, when you spend hours in a traffic jam because one DPW worker is running a weed wacker on the median of the road… you need an SUV

But the bureaucrats who were supposed to fix the pot holes and clear the traffic jams … they were inventing a hedonic adjustment to keep new car inflation low.

Its hedonistic for you to expect to be safe traveling to and from work

You also have to account for each “class” of product not existing in a vacuum: People first need “Food and Beverage”, “Health Care” and “Housing.” When the cost of those go up, the actual, realistic, affordability of cars, toys etc., decrease, even if the price of the latter would have stayed constant.

So, the above graph is largely tautological: If the most basic categories increase, categories further down the necessity rank, will simply have to decrease. There’s simply less money left to create demand for them, after increasingly expensive necessities are paid for.

Then, all that is left to keep up the “low inflation” illusion, is to include the less necessary categories fully when computing it, while either including less fully, or flat out omitting, the categories which are closer to necessities.

TVs are almost -100% my $1000 flatscreen begs to differ. Are we saying it is worth $10,000 relative to the 32 inch at $500 from 1996?

Because if thats the case the stint removal my father just had is worth like $2B to me given the improvement of his health. Is this a chart of technology improvement relative to what people can pay for technology improvement?

If you just spent $1000 on a 32 inch flatscreen, then you are a fool.

Assume you meant to say your father had a stent removed? With an “e”, not an “i”? Moving beyond your spelling issues, the chart isn’t about one specific health procedure (or one overpriced TV), its about the typical cost of a consumer’s total health care — at least according to the BLS.

re: “…our health outcomes aren’t as good as countries that spend half as much.”

Our health outcomes are surprisingly good, considering the diet of Omega-6 vegetable oils, low fiber, high simple carb, overly processed foods that most people eat, and the low amount of exercise that most people get. Those things have far, far more to do with the health outcomes than all the medical care you could get.

All the McMommies in North County need at least a Lexus to be seen in, and it’s all good, because the McMansion is appreciating and there’s HELOCs as far as the eye can see. 6 year car loan? 7? 10? Why not 30? The house will pay for it all! What could possibly go wrong?

They are driving in their McMaxMobile thinking of all the suckers who drive cheap cars. With FED on the loose, you lose.

In the 11th year of our Fed-purchased expansion, 40% of people report they can’t handle a $400 emergency expense. Does this mean I can get a really good deal on a used Glitzmobile soon?

If there’s a significant market drop and recession, used Tesla’s may actually become affordable.

Did someone on here at various times say socialism?

How taxpayers may wind up subsidizing Uber and WeWork’s losses

link to qz.com

On AVERAGE, tax payers; or more technically accurately, dollar economy participants; have subsidized at least 95% of all salaries and wealth accumulation in the FIRE sectors, since the early 70s. That’s what The Fed does: It debases people who produce value, and hand the money to idle halfwits in New York (and elsewhere.)

And that’s on average, For complete wasteshows like WeWork, money center banks, hundred-thousand-to-erect-but-million-dollars-to-buy houses etc., the subsidy is waaaaaay in excess of 100%: The wast-of-spaces involved in the rackets make bank, despite not just being idle, but in fact flat out destroying value as they stumble along on their cloud of undifferentiated idiocy.

Taxes and over bailouts add to that. But far and away the biggest chunk of subsidies for, and reditribution for the benefit of, (predominantly bicoastal) connected worthless sycophantic clowns, are being engineered by The Fed. Direct taxation is largely a side show. Hence such classics of Guardian-drone economic illiteracy as “The Blue States are ‘Net Contributors’….”

U.S. Auto Sales, Third Quarter 2019: Winners and Losers

link to thetruthaboutcars.com

“Thanks to stretched out payments, dealers make more on loans than cars.”

Thanks to financially illiterate poor suckers, dealers make more on loans than cars. I guess, they can still manage a standard sub-compact instead of a usual fully loaded gas guzzling SUV.

Not so long ago, the average car lasted 5-7 years, so financing it beyond 36 months was a stretch. Today the average car lasts about 12 years. Financing a car with a life of 60 months for 36 months is 60% of the useful life. Financing a car with a 12 years life for 86 months is 60% of the useful life.

It’s also nuts.

Where did you find that stat? Average being 12 years. My car will soon be 16 y/o yet I don’t know anyone who has a vehicle anywhere near that except for 1.

I gave that stat from memory, but did a web search, and it says that the correct number is 11.4 years, so I was pretty close:

link to blog.nationwide.com

… and not long ago most car problems could be fixed by the local gas station. Today, you are trapped into the ridiculously expensive dealership repair garage.

How long a car “lasts,” is no longer primarily determined by mechanical degradation. But rather by when an owner can afford to upgrade (hence why such paragons of mechanical reliability as one-off, high tuned Ferraris seem to all have lasted since the 50s…).

Mechanically, Toyota and others, had pretty much “perfected” cars by the 90s. Wrt Corollas, Camries, Land Cruisers, Tacomas etc., I’d almost be surprised if the more recent ones aren’t more prone to early breakage (of their increasingly engineered for weight savings, mileage etc. components) than their “Golden Era” ancestors.

So, as cars get less affordable to replace, they’ll “last” longer. Pretty much by definition.

Dealers also make money on vehicle repairs.

One owner of a large Ford dealership I know told me that they made most of their money on the service department. The front office is a price they have to pay to Ford to get the dealership rights – it is seen as more of a cost center than a profit center. As the article highlights, the finance office is also a major profit center.

Hence, they are called stealerships.

I assumed that’s where they make all their money. Selling cars was just the first step in having cars serviced.

I guess you missed the GMAC bailout under obama about nine years ago. They couldn’t “afford” cars at that time.

Only $17 billion of taxpayer money flushed down the toilet.

“A third of auto loans in 2019 had a term period over six years. People cannot afford the cars they are buying.”

Hmmm… GM didn’t pay back the money it got from the govt?

Stop spoiling his fact free rant.

LOL

GM did pay some taxpayer money back. But not even close to what they borrowed.

But the obama UAW/GM bailout, in the end, cost taxpayers $17 billion. And the destruction of 100 years of contract law.

Facts are hard to understand, I know. Especially in your echo chamber.

GM didn’t payback all the money. They got tax breaks, subsidies, and free money that helped payback the loan. Dont forget cash for clunkers too.

Listen you arrogant bozo. I asked a question. I don’t think someone needs to be disrespected because he asks a question. If you have an answer, why not provide it. You don’t need to come off all high and mighty. You will never persuade any one to your position doing that. Or are you merely interested in showing how smart you are and how dumb everyone else is?

Rising Car Prices Are Sending Even Strong-Credit Buyers to the Used Lot (NYT)

link to nytimes.com

“These are signs of a “Late Stage Credit Bubble”

Mish, this is something I’d like to read more about. I’d love to read your insights/predictions regarding this matter. Or your thoughts on ‘the endgame’.

Thank you.

I was initially confused that dealerships make money on insurance. I totally forgot they push gap insurance, unemployment insurance, and life insurance for those car loans.

The big thing they push is extended warranties. Those are high dollar money makers. That is, after all, a kind of insurance.

We get telephone calls for those extended warranties for a car we leased last year.

The ultimate goal of all fully financialized dystopias, is that all money is made from loans. Fully systemic rent seeking, IOW. That way, the rank idiots who champion the illiteracy, don’t have to worry, that their lack of absolutely anything else of value whatsoever aside from Fed provided “asset vaijues” to lend out, will cause them to simply be routed around and left for dead by their betters.

As for the Fed itself: When every single penny owned and/or acquired by anyone, is due solely to their closeness to The Fed, rather than to any productive ability, talent, aptitude nor effort on their own part;…… well, The Fed is sitting pretty sweet….

I’m bitter about the injustice of it all. And the damage it’s done to this and future generations. How the f-word can we wake up the masses and start demanding an end to this insanity?

We can end the Fed and all ability to print money. Tnd price the dollar at $20/oz. Or perhaps $1/gram, to make metric easier…

Default on all the public debt which younger generations are somehow, due to no fault at all of their own, is supposed to “owe” to leeches.

Get rid of all income and other activity taxes. Whatever money the state needs, it should obtain from charging for the direct services it provides: Protecting the border (tariffs), and protecting private property ( property taxes). Nothing else.

Stop interfering in how private property owners use their property. Meaning, treat zoning, land use and similar laws and ordinances, as what they really are: Clear violations of private property.

Affirm, once and for all, that the only people responsible for government debt, are the specific politicians who voted for it in the first place. Not random children who just happen to be stuck between some arbitrary lines drawn on a map.

Do that, and you’ll at least prevent further erosion. As well as go quite some ways towards righting previous wrongs, even if necessarily still imprecisely.

Barring that, if “we” have now reached a level of general incompetence and economic illiteracy sufficient to prevent us from achieving something very close to the above; we’re stuck with plan B: Sit back and wait for the Jihadis to save us from ourselves. They’ll do it, no doubt, and while anything whatsoever is an improvement over progressivism, I’d still personally prefer a different solution than theirs.

“When every single penny owned and/or acquired by anyone, is due solely to their closeness to The Fed…”

Isn’t this already the case? There’s Treasury notes and Fed notes. Everything else boils down to those, and they form a loop — buy a big IOU from the Fed with Treasury IOUs and you will be paid back with … more Treasury IOUs.

Since 1971, all the “money” in the world is fundamentally debt to government entities. Which means: receipts for future taxpayer labor. The US has been sitting pretty through this, because we’ve got the most reliable taxpayers. But it is unsustainable, because the debt slaves have to keep running faster as underlying capital gets spent, leaving higher levels of debt slavery.

The reason people cannot afford the cars they are buying is because the banking system is similar to the insurance system. If cars and homes could only be paid for through credit cards or cash, the prices of them would fall like a rock. We will get < 2% on mortgages soon. A final reflation and then a collapse to <1% on all loans. What this “late-cycle” has showed, is that as time goes to infinity, rates must go to zero.

Touche!!

The printed up “credit,” which the saps are being indoctrinated from birth into believing is somehow “important” for obtaining anything from a house to a car to a business; in reality serve no other effect than driving up prices of houses, cars and inputs to production. For the exclusive benefit of the idle clowns close enough to The Fed to have first access to the newly created money. To the the detriment of everyone else.

Yes! I call it, hyperfinancialization of everything. Especially this last decade of excessive moneyprinting has pushed consumption, mortgagelending and loans on everything into insane over-indebtedness. And now they’re surprised things slow down, growth is minimal and delinquencies are on the rise. Add to that the gimmegimme generation and this is what you get. But hey, life is great, life is awesome, let’s all live in Pods in the Bay-area!

I find it harder and harder to believe that somehow, this isn’t going to end in a massive, giant deflationary de-bubblification.

You know what I do when I can’t afford a car? I don’t BUY it. And I certainly don’t finance it.

About half the cars I have owned were well maintained inexpensive clunkers. To include a door handle that fell off a Honda that was replaced with some rope (I did get out of a few tickets with that!).

“The reason people cannot afford the cars they are buying is because the banking system”

Oh, you are one of those NERDS that knows how to fix things 🙂

/sarc

The reason people cannot afford cars is because they are financially illiterate.

The reason people cannot afford to maintain cars is because they were learning safe spaces and gender neutral bathrooms and whining about Trump…. even the pansy boys skipped shop class.

When I lived up north, not one kid in the neighborhood knew how to change the spark plug on a lawn mower (not a car, no distributor to worry about — a friggin’ lawn mower). No kid knew how to change the oil on a mower either. And what is this carburetor thing you speak of? I’m feeling triggered!

Those kids who can’t wipe their own butts grow up to be adults that can’t read a car loan.

“The reason people cannot afford cars is because they are financially illiterate.”

And corollarily, because something as trivial, and as solved-eons-ago a problem as obtaining a car, requires some level of “financial literacy.” Solely on account of what passes for “finance” these days, being nothing more than a crass theft and redistribution racket. Back in the civilized era, sufficient “financial literacy” to run a California sized ranching operation, amounted to little more than counting the coins at the bottom of a chest, and see if they added up. Freeing potentially productive people up to do something useful with their lives, instead of reading 13 pages of fine print and masturbating over make-work nonsense which serve no other purpose than aggrandizing idle half literates in money centers who own “assets.”

On a more positive note, it appears to me at least some of those much maligned “millennials,” are actually starting to make up for their lacking formal education in anything useful, by embracing Youtube videos on how to fix, and make, stuff. Up until 5-10 years ago, I’d agree with you it looked like the ability to putting on clothes themselves, were about to become a lost art among coming generations.

But now it seems many of the “cool” things they aspire to do, from turning a Prius into a permanent dwelling, to building irrigation, ventilation and electric systems for their grow ops, up to even organic market gardening and buying an old sailboat and kitting it out to sail around the world; requires more “practical” skills than youngsters have had in at least a generation or two.

I live in the bay area and have no significant debt. I dont own a car because it’s not really necessary if I live near public transit and work in a dense downtown where parking is super expensive. Just another headache I dont need