Valuation Inflation is one of Mauldin’s best “Thoughts From The Frontline” columns ever.

Mauldin posts charts from Jim Bianco, Peter Boockvar, Doug Kass, Tony Sagami, Jesse Felder, Ed Easterling, Ned Davis, Doug Short, and Jill Mislinski.

Here are a few of my favorites.

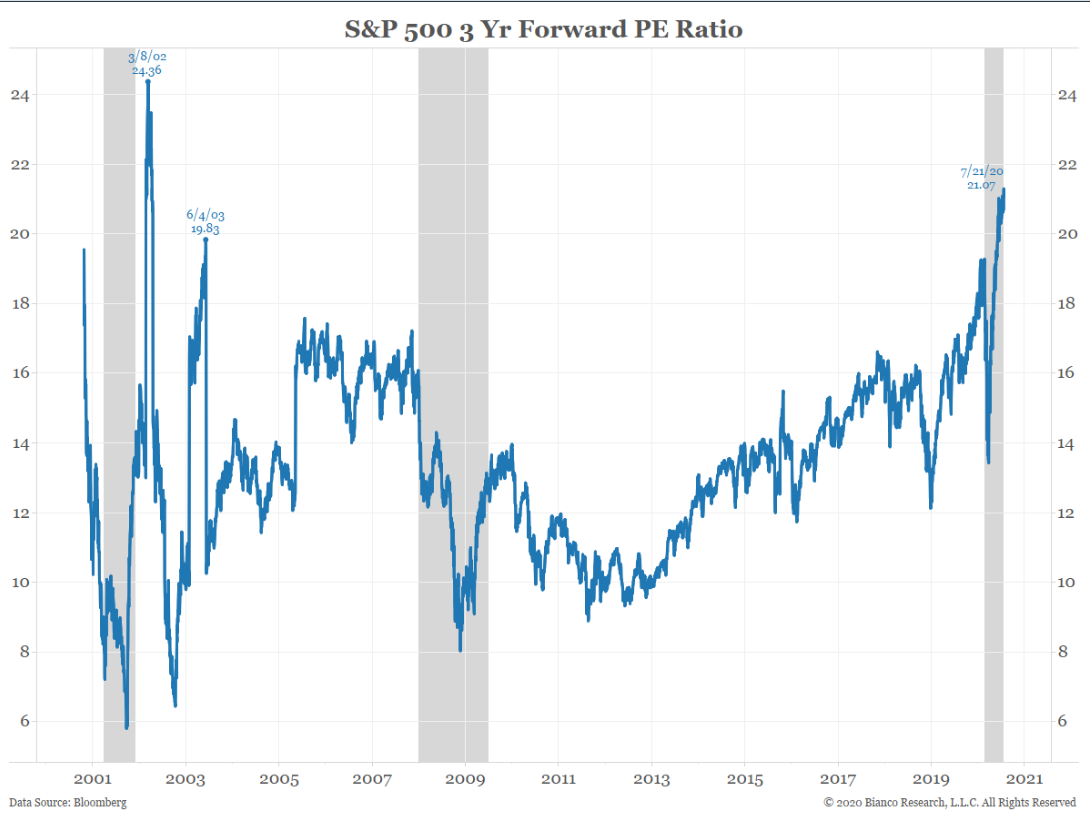

Jim Bianco – 3 Year Forward PE

Mauldin picked that up from a series of Tweets by Jim Bianco.

This shows error rate of 3-yr forward earnings. The green bars (bottom) = estimates are too high, often by as much as 100% when coming out of a recession (now).

Not only are you paying 21 for 3-yr forward earnings, history says they can be way too optimistic as well.

(3/3) pic.twitter.com/t9fdIvOd3v

— Jim Bianco (@biancoresearch) July 23, 2020

Inventing a New Metric

The Price-Earnings ratio look so terrible the bulls invented a new metric, the 3-year forward PE that supposedly shows what earnings would be were it not for Covid.

Tony Sagami

Much of the S&P 500 returns come from just 10 companies: Microsoft, Apple, Amazon, Google, Facebook, Visa, Mastercard, Nvidia, Netflix, and Adobe. As a group they are up 35% since the beginning of the year. As a group, the other 490 are down more than 10%.

The chart is Mauldin’s post also comes from Twitter.

Is there an ETF that mirrors the performance of the S&P 490? If you strip out of the 10 strongest stocks out of the S&P 500…the stock market looks pretty sickly. pic.twitter.com/fgGWLmc4A6

— The Sagami Letter | Tony Sagami (@Tony_Sagami) July 22, 2020

Here is another one from Tony that was not in Mauldin’s list.

32% of the S&P 500 has delivered Q2 results. Chart from @charliebilello pic.twitter.com/XWLv6B22yS

— The Sagami Letter | Tony Sagami (@Tony_Sagami) July 25, 2020

Ed Easterling – Crestmont

The idea behind the 10-year smoothed PE is that earnings revert to the mean over time. They always look terrible at the bottom of the cycle and great (relatively) at the top.

This is a very expensive market. Advisor Perspectives comes to the same conclusion.

Maludin presented a chart from Advisor Perspectives, Jill Mislinski, Is the Stock Market Cheap?

Here is another chart and commentary from Advisor Perspectives.

PE 10 From Geometric Mean

Relative to the mean, the market remains quite expensive, with the ratio approximately 70% above its arithmetic mean and 84% above its geometric mean.

Wouldn’t Valuations Be Much Lower If We Exclude the Financial Crisis Earnings Crash?

This is an often asked question, the assumption being that the unprecedented negative earnings of the Financial Crisis skewed the P/E10 substantially higher than would otherwise have been the case. While that may seem a reasonable assumption, a simple experiment shows that the earnings plunge did not dramatically impact the ratio. Let’s assume that the December 2007 TTM earnings of 66.18 remained constant for the next 29 months, totally eliminate the collapse in earnings of the Great Recession. What impact does this have on the P/E 10? The mean (average) only drops from 16.6 to 16.5. The lower bound of the top quintile drops from 21.2 to 20.8.

The above excellent comments from Jill Mislinski.

Triggered Market

Mauldin comments “Overvalued markets don’t turn down on their own. Something usually triggers them. What could it be this time?”

While there is always a chance of an oil shock, Covid shock in this case, or some other shock triggering a decline, more often than not, sentiment suddenly changes and that is the trigger.

If you think back to 2006 people were standing in line for hours waiting to enter a lottery for the right to buy a condo. The next month, there were no lines at all. Builders offered massive discounts.

But the market advanced for more than another full year.

Mauldin commented “Back in 1999, I and many others thought there was no way the bull market could go on. Yet it did, with the Nasdaq actually doubling in 1999.”

When Covid hit, many thought it would be like an oil shock only much bigger. Instead it triggered massive speculation in tech stocks.

As with the housing bubble that actually burst in 2006 (but stock kept running anyway) we did it again, only bigger.

This blowoff top pattern is not so unusual after all.

Sentiment is the Trigger

Think back to November of 2007 when the S&P 500 hit a then all-time high. Recession hit the next month.

What was the trigger?

There was none that anyone can point to. Here’s the “trigger” if you think carefully: The pool of greater fools ran out.

People stopped buying houses a year earlier but commercial real estate and the stock market kept things humming for another year.

Then sentiment changed. There was no other reason then or on 2000, or now.

What about jobs?

Over 30 Million People About to Lose $600 in Unemployment Benefits

Congress is debating on whether or how to extend Covid benefits. Note that Over 30 Million People About to Lose $600 in Unemployment Benefits.

That’s about $18 billion a week in benefits.

Also note that Unemployment Claims Rise for the First Time in 4 Months

Unprecedented Recession Synchronization and What it Means

Please consider Unprecedented Recession Synchronization and What it Means.

In the article, I discuss comments by Lacy Hunt at Hoisington Management.

He explains the deflationary consequences of the current global situation.

I too expect a deflationary outcome based on demand destruction. Meanwhile, my other comments apply.

Unwanted Inflation Easy to Find

Actually, inflation is easy to find. Look no further than the stock and bond markets.

The Fed’s balance sheet expansion coupled with trillions of dollars of fiscal stimulus (both unprecedented) has resulted in stock market speculation also at unprecedented levels exceeding the housing bubble boom in 2008.

Inflation is not where the Fed wants it.

The Fed can print money and Congress can hand it out, but neither can dictate where the money goes.

In 2020, money has found a home in rampant speculation in stocks and bonds. In 2008 money primarily went into a housing bubble.

But bubbles burst. Thus, speculation too is inherently deflationary.

Why expect anything differently this time?

People will blame jobs as the trigger, but if that was the trigger it would have happened already.

The Fed blew its third major bubble in 20 years. Bubbles always burst with deflationary consequences.

They burst when sentiment changes. The pool of greater fools always runs out.

Mish

Personally came to the conclusion that the news get matched to price action most of the time not the the other way around.

Excellent post, MISH. Thanks. Been wondering what could possibly be the trigger for the next leg down, but didn’t consider that that there doesn’t actually need to be a trigger.

Mish, what makes you think the stock an bond market inflation is unwanted by the Fed? It seems to be the inflation the Fed craves the most. Kinda find all the comments bullish, not that I disagree with the article, I don’t. Many looking for massive pullbacks, technicals are a bit wobbly, but not broke…yet. I own a lot of gold and silver physical and stocks, and the greater fools game has begun with metals I think. More to run for sure, but current demand seems unsustainable, beware of backwardation in gold / silver.

1.) M2 velocity is falling. Bernanke’s helicopter can’t help Greenspan “push on a string”. Deflation is well under way.

2.) Delaying eviction is more of a benefit to renters in urban areas than an extra $600/ week because back rent will never be repaid.

3.) Some sort of handout will have to be approved right before elections to buy votes.

Mish states this thesis better than anyone, and I think it will be proven true again: bubbles end when sentiment flips, and sentiment of the masses can flip for surprisingly little “reason.” Another way of looking at it: the house of cards of “reasons” for high bids on assets falls down very suddenly, exactly because the reasons were baloney all along. I expect it will continue to be obvious that the Fed has a floor under stocks and bonds right up until it’s obvious that there’s no floor at all. The Fed cannot buy the whole market.

Usually the peak of a bubble follows shortly after the appearance of the “this is the new normal” crowd. When the talking heads start crowing about a new paradigm in. I’m curious as to whether that will come still or if the market is just so broken that no one is even going to bother

Has not Japan essentially bought it’s whole market?

As has, effectively, The Fed. And as did the Soviet Union.

The exact dialect of Newspeak employed to justify doing so, being far and away the biggest difference between the three.

When stocks fall 50%, the stock market will be closed till moral improves. That’s the floor.

The late, great Martin Zweig “Don’t fight the fed, don’t fight the tape.”

And of course “Bull markets climb a wall of worry.”

LONG with regular purchases of gold/silver since 2008. 🙂

Mish – would the Fed have a better chance of achieving “wanted” inflation if they were to deliver a massive amount of helicopter money straight to Main Street. If I remember correctly the $3.5T stimulus package would have translated into something like $15,000 per person in the US.

“helicopter” drops are FISCAL … ie: originating out of Legislative body.

In simplistic terms the Federal Reserve is just a couple of thousand of economists. That’s it. No bureaucracy, let alone authority to send out checks.

In the US there are 120 million households. Federal Reserve has no access to their names / addresses / social security numbers.

No Way will Congress EVER give up The Power of the Purse.

If congress were to decide on UBI for example, how would the fed manage that request ? They could decide not to accommodate it and let yields rise but that would likely be a challenge for banks as a whole, or they could accomodate it but knowing that it would likely at least bring disruption and remove authority from banks. In short I just wonder what happens if there is a standoff of this kind, not that I expect anyone to know the answer.

Correct – But they cannot. Tony Bennett replied correctly.

It is also unclear they would if they could. The Fed is beholden to the banks.

If the Fed thought free money would hurt the banks, they would not do it if they could. But the point is moot because they can’t.

You have to love this Republican government…..

Over 30,000,000 unemployed, unemployment benefits ending, and the Senate majority leader says it could weeks to pass the next stimulus package. What the hell!!!

We have been living with this virus since February, we know testing is the key to getting it under control (despite what our clueless president believes) and we are still living with testing shortages. What the hell!!!!

This has to be the most incompetent elected US government ever. Much like Nero fiddling while Rome burned. How anyone can defend the Republicans response to this Covid outbreak is beyond me. Must be some mighty powerful Kool Aid!!!!!

You have mastered the obvious!

Would be interesting to see if there is similarity somewhere with patterns like those in countries that find high inflation. There as far as I know the stock market rockets chasing inflation, but there must be a window between spending, government yields, retail prices, economic shock where it all goes awry, maybe in a certain order.

Point is people are chasing yields because the rest of the economy does not provide them, I’m on the deflation side of that except also that the economy can be understood as yield and that yield is the value of money, if there is no economic yield money becomes worth less, not more – you have to spend more to secure and prices go up even as demand goes down. The whole show would have to become unhinged to get there, as has happened historically occasionally.

Over to Spain and it just piles up for the country:

Bank of Spain says EU fund will provide only 10% of that needed over the next five years.

UK decides without warning that anyone returning from Spain from tonight will have obligatory quarantine. There goes most of any tourism left from UK.

France says strongly not to travel to Cataluña.

Cases in Spain are turning up. Numbers are opaque, for example only one in ten hospitalisations in Cataluña is being announced according to elmundo, or there is no official daily figure of new cases only moving targets that give lower headline.

Suggest anyone interested follow

twitter.com/matthewbennett

A friend with some closeness to the Baleares government, tells me they are just trying to get through the Northern European synchronized mass summer holiday with as little hiccup as possible, since such an outsized share of almost all businesses’ revenue and workers salaries are earned during the months mid June to Mid September. The idea being, once the end of September rolls around, they can all close down and clean up, if contagion is high. Case and hospitalization counts are still remarkably low over there it seems, despite how close it is to Barcelona, and for being such a pressure cooker of tourists during season.

At least unless numbers are being under-reported 10 to 1…..

The way “the economy” balances out over there, I suppose, is that the Germans work 9 months out of the year to make all the things the Spanish buys. So at the end of spring, all money is in Germany. Then, for three months, the Germans come to Spain to live it up in the sun, spend all their earnings and cruise around butt naked for three months. Such that at the end of summer, all the money is back in Spain again. And then, come fall, the Germans go back to making stuff the Spanish needs to buy, so the money comes back to Germany again. Etc., etc….. So that if those three months are interfered with, the repercussions are just massive. Not just for the Spanish who don’t make money in the tourist trade, but also for the Germans those Spanish normally keep employed with their tourism earnings for the rest of the year. And then the Germans can’t afford to holiday next year…….

Made me laugh, but that is about it. I know the south from before tourism arrived, partly from having lived there from before it became “modern tourism” and not a few hotels where tourists arrived with a towel and happy just to wander quietly around town for a local meal all very civilised and contained with a sense of privilege thrown in , but also because I learned how things were just before that. Places even slightly removed from tourism were still in the older way of doing things, my local town of several thousand people (now many more) had a documentary made of it in the late sixties, they had one car in the whole town, owned by the postman and that also served as bus and delivery vehicle.

I liked talking to older people when possible, there was a lady at a fountain we used to fetch water from in a hamlet, one of the most lucid and gentle people I have met. She told me of how it was when she was young. School was only for boys then, she would help out with whatever needed doing at home, life was very simple but she remembered that there was always something to look forward to, always something to keep people happy.

Essentially that is Spain, it had farming fishing and some small industry depending on whatever was needed, conservative but generally at peace with itself, a peace that had had a heavy price to pay to achieve and whose borders were still strictly guarded.

The rest is modernisation, mostly tourism and construction…a nation of albaniles as one local described it.

That doubled with entry of euro, high finance, european politics, modern themes being pushed. In Spain they focus on “machismo” and gender violence because gender identity politics is too far beyond what most would tolerate, but they have started that lately as well. The country has become formatted and subsidised, corrupted at so many levels. Even younger generation I talk to miss the freedom and social world before this, now the youth are often reduced to botellon.

Without tourism and real estate the country is as poor (said without prejudice simply in terms of productivity) as it ever was, except society is no longer locally coherent and structured enough to handle that reality. Expectations and hence disillusions are higher, the amount of national and private debt is way higher than what it was pre-euro, there are all kinds of resentments that have built up.

Now I suppose we will watch the government try to turn the country full socialist northern/french model, because people and the country are so cornered.

It’s really sad to watch this going on, but at the same time the Spanish have a side that is irrepressible, I hope that lives on. They aren’t as stupid as sometimes made out either, just the oganisation is lacking, or too much maybe because they really do best when involved and figuring things out for themselves.

Just reading Baleares might be excluded from quarantine, and Canarios. Tens of thousands are cancelling ther holidays now apparently.

This is a map of countries that have travel restrictions on anyone trying to travel from Spain

“The rest is modernisation, mostly tourism and construction”

At the very least, Spain has the advantage that so-called “finance” is not the main one. That is what was the bane of the Anglo countries. Italy, and even Greece, is much more burdened by that as well.

That is a curse both Spain and Germany has, relatively speaking, avoided to a greater degree. Such that industry/manufacturing in Germany, and construction, as well as tourist services, in Spain, has been less burdened with having to pay massive unearned rent to the ever more rapacious, government facilitated thieves and leeches which is all money center “finance” ever has been, and ever will be. I bet most Spaniards have no idea how lucky they are, that Latin America’s “financial center” ended up being Miami, rather than Madrid….

As a result of fewer and less wealthy/demanding FIRE leeches to feed by their construction industry, I bet a given distance, and quality, of road can be built for 1/10th in Spain, versus in similar climate California. And a new highrise in a high demand location, ditto. All despite combined real wages and benefits (In Spain partially government provided) being no lower than what those who actually build roads in California earns.

With the difference going solely to FIRE, “legal” and lobbying deadweights facilitated by the sort of pointless NIMBY driven meddling, which is required to ensure the “collateral” upon which the FIRE leeches’ stolen fortunes are perched, don’t risk “going down,” due to more modern, better and cheaper alternatives rendering it less attractive.

Both construction and tourist services (like manufacturing in Germany) do employ lots of people. Construction, and even tourist services when done competitively at the sheer scale it is in Spain, in “good” jobs as well. And because those sectors are so critical, they are influential enough to beat back the FIRE leeches’ NIMBY nonsense much more effectively, than in anglo countries, where living off of central banks’ stealing from others, is virtually all that is left as a means to make a living.

True. Post gfc there was an attempt to encroach on Spanish realty by the US, but the Spanish tend to keep the sector in-house. There is an old rivalry with the US, and a distrust which is warranted. Involvement in the Iraq war, Libya even, reinforced that. With the UK as well the relationship is sometimes difficult for a range of well known reasons.

What did happen though is that national financial structure after euro changed greatly. Previously rates were high and financial dealings were in the hands of traditional regional power holders. They could not compete in the euro-ised framework and come gfc most of those failed and were merged, giving fewer but well connected high power lenders. Santander for example is modern/traditional mix, BBVA is more adventurous but still answerable.

The surplus real-estate was swept under the rug, basically nationalised until it could be offloaded, and the rest of the argument has been about not evicting people, about trying to keep property prices afloat (but not astronomical), about trying to reorganise employment. So the greater of excesses after gfc were avoided being repeated.

The problem is that this has all cost the country a vast amount of debt, and has led to new forms of socialist influence. 15M protest movement which was basically non partisan anti-corruption got co-opted/deleted by the far left podemos. Both traditional parties are seen as corrupt, the royal family also is being shaken by scandal. Local economy has pretty much stagnated for a decade, in other words they rearranged the deck chairs and put a different face on it but the country was not going anywhere in a hurry, with endless political impasse thrown in.

Now what though ? They will be on their knees to EU for a decade , while EU takes over managing the country, which is basically what it says it must do in exchange for help ? Or they will borrow till the lending stops ? Already at 100% debt to gdp before pandemic, when they are supposed to be under 60%, skirted direct intervention during gfc, but now ?

So you don’t have the FIRE racket, but instead you have one political racket or another ready to fight over the say and direction, and society still very much divided and in future likely more than fed up.

It isn’t like they can have a bad tourist season and just go back to their local economy till it improves. The figure for tourism is somewhere over 10% gdp, but in reality that money then flows through the economy accounting for a much larger part. People miss this effect – wages from tourist gets used at supermarket pays employee gets used at restaurant pays supermarket etc. The whole system is supported by this, and government spending cannot replace it.

I always wondered about the inflationary aspects of continually rising stocks & bonds prices.

I go to the store and buy a pound of ground beef. Price has gone from $4/lb to $6/lb. Definitely inflation.

The price of Tesla stock goes from $500 to $1500. Inflation??

At least I can make a couple of burgers with my pound of ground beef.

👍

The $600 federal unemployment benefit has expired THANK GOD!

Tens of millions are hurting, tens of millions were hurting last month, and last year. Disabled vets have a homeless problem, of course, a 100% disabled vet is compensated at $716 per week. That is good enough according to congress for your vets, so it is good enough for people temporarily sidelined by Covid. When they say we will give disabled vets $600 per week more then I will feel bad for the unemployed.

Mish: Please stop pointing out the obvious until I am done buying a multi-generation supply of gold and silver.

Just to be devils advocate the PE on the 30 year Treasury is over 80. 170 for the 10 year.

Bonds have yields, not earnings. That aside, your comment is not DA at all.

Rather it is one of the silly justifications you hear all the time “stocks are cheap compared to bonds”.

Hussman accurately blasted the concept recently.

Well yes the cash flow on bonds is fixed and known so it’s easy to sum the present values to arrive at the price with a given yield. It’s not possible with stocks because future earnings aren’t known and could be quite volatile.

Do you have a link to what Hussman wrote, I could only find something from 2015 although I’ve no doubt it’s very similar. It might be a good topic for one of your articles.

Two things.

Treasuries are backed by the full faith of US taxpayer.

Stocks / corporate bonds backed by ????? Losses WILL occur.

Second, you (and most everyone else) are ignoring capital gain on treasuries when yields drop.

Stocks/corp bonds backed by …

The FED.

haha.

Federal Reserve has a very loud bark. Bite? Not so much. Folks front run the FR, obviously. But when push comes to shove?

Federal Reserve balance sheet just under $7 trillion. Likely go to $10 trillion to $15 trillion before we’re done this recession.

Total US debt + equity valuation ~ $115 trillion.

Federal Reserve will have its hands full treasuries and state / local govt debt.

Everyone else? Good luck.

“Treasuries are backed by the full faith of US taxpayer.”

…For as long as the US taxpayer remains dumb, bent over and indoctrinated enough to accept pliantly playing perpetual patsy for the gaggle of negative-value-add leeches feeding off of him.

If he ever wakes and grows up, well…..

“Second, you (and most everyone else) are ignoring capital gain on treasuries when yields drop.”

No I’m not, I’m an ex bond trader (80’s & 90’s) so I fully understand price movements in relation to yields. You didn’t follow the point I was hinting at, which is that some people think equities look cheaper than bonds by comparing PE’s. Only this week someone mentioned to me that Nestle could quadruple and still look good on an earnings basis v current rates and yields! I’ve no idea whether it’s cheap or not, but fully endorse the gist of Mish’s post that current stock markets are expensive and are pricing in forward earnings that won’t materialise. Mind you I’ve thought that since the end of last year and Covid only made them worse, so I’ve been wrong about them since the lows.