Economists misguessed consumer behavior yet again. Flush with stimulus money, Consumers Shun Credit-Card Debt.

When unemployment soared this spring at the start of coronavirus lockdowns, credit-card debt and delinquencies were widely expected to surge as struggling households borrowed more to make ends meet.

Instead, amid the deepest economic crisis since the Great Depression, the opposite happened. Credit-card debt in the U.S. and other advanced economies has fallen. Fewer people are late on their credit-card payments. Consumer demand for new borrowing—through credit cards, personal loans and even pawnshops—is down sharply.

The main reason, according to economists and financial executives, is government stimulus programs launched in the U.S. and other advanced economies that have worked unexpectedly well. The flood of money, along with debt-relief measures such as deferred-mortgage and student-loan payments, has stabilized the finances of many households and even left some in better shape than before the pandemic—at least for now.

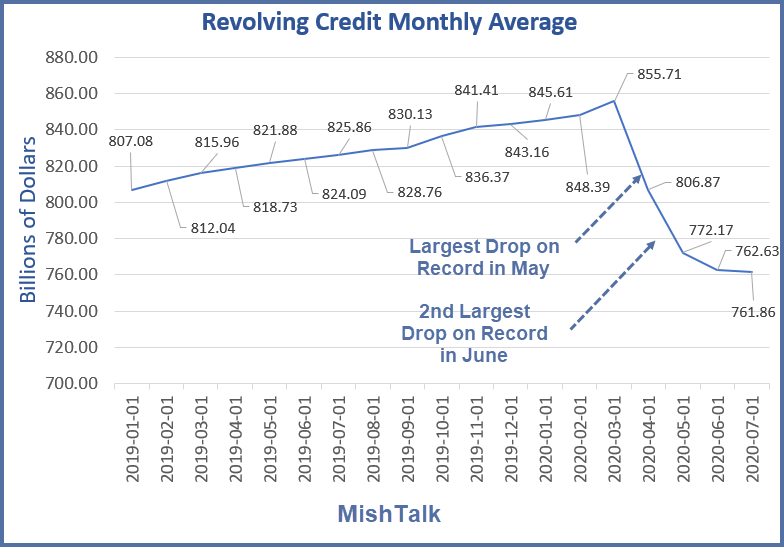

April was the largest monthly drop in revolving credit on record, while May was the second-largest, according to Federal Reserve data. Personal-loan originations were down by a third in mid-May compared with the beginning of March, according to Equifax.

Since February, credit-card debt is down 11% in Canada, 14% in the U.K. and 17% in Australia. In the eurozone, credit-card debt and other forms of revolving credit for households fell 5% between February and June.

Revolving Credit Monthly Average 2001-2020

Comparison to Great Recession

- Between February of 2009 and February of 2002 consumer credit declined 12 consecutive months for a total drop of $77.09 billion.

- This is month number 4 with a total drop of $93.85 billion.

What’s Going On?

- Stimulus money is in play but psychology may be a bigger factor. People are rightly worried about what happens when the checks run dry.

- Millions of consumers make more being unemployed than they made being employed. They have an easy means to pay down debt.

- Those in mortgage forbearance plans have an easy means to pay down debt.

Point number 2 is a pet peeve of Trump.

Republicans want to address that point by limiting unemployment checks to no more than 70% of what people were making before Covid hit.

Fed Wants More Free Money

As noted earlier, Fed’s Kashkari Urges Congress to Hand Out More Free Money

In addition to calling on Congress to hand out more free money, Neel Kashkari discusses a hard lock down.

“If we were to lock down hard for a month or six weeks, we could get the case count down so that our testing and our contact tracing was actually enough to control it,” Kashkari said.

Fed Independence?

The Fed hollers every time Trump or Congress meddles in monetary policy, but the Fed repeatedly meddles in fiscal policy.

And here’s a new one: The Fed is willing to interject its beliefs about medical policy as well.

Spigot Temporarily Off

As noted on July 26 the Clock Just Ran Out on $600 in Weekly Unemployment Benefits.

On July 29, Trump announced “So Far Apart on Covid Deal That We Don’t Really Care”

Those with no money coming in certainly do care and they will not take too kindly to expiring benefits, even if it is temporary.

Meeting of Minds

Republicans and Democrats met this weekend but the parties are “not yet close to a deal” according to Senate Majority leader Chuck Schumer.

But, there will be a deal and I expect Pelosi will get most of what she wants. My guess is $400 instead of $600 weekly checks.

Click on the preceding link for the major points of contention, but they do agree on one thing.

Both parties want to send out blanket $1,000 checks even to those who have not lost a cent in wages, with a cutoff of those who made $95,000 last year.

Hooray! More Free Money

Let’s see how long a deal takes, but my guess is this week.

Mish

Apologies offered on inability to comment