by Mish

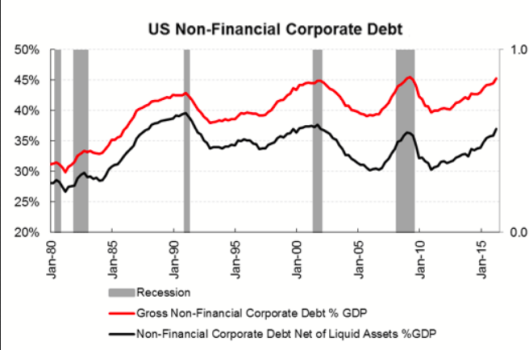

The present calm in high-yield markets is entirely unwarranted and at odds with where we are in the US credit cycle. Corporate debt to GDP in the US is at all-time highs. In the past, whenever corporate debt reached around 42-45% of GDP, the US approached a recession. Today rates are lower, but corporate debt is already above 45% of GDP. Some investors prefer to look at net debt minus liquid assets, but even there, the measure is higher than in 2001 and 2008 (also the top 50 companies hold two thirds of all cash, so aggregate figures are highly misleading).

Every single leading indicator we have points to wider credit spreads. It doesn’t matter if you look at accounting relationships (cash flow to debt, capex to EBIT) or economic relationships (corporate debt-to-GDP, lending growth YoY), or market relationships (yield curves flattening). The message is wider spreads are inevitable.

Credit Spreads Expected to Widen

Mike “Mish” Shedlock