The Wall Street Journal has an interesting infographic series of 25 charts entitled 10 Years After the Crisis.

Here’s eight of the 25.

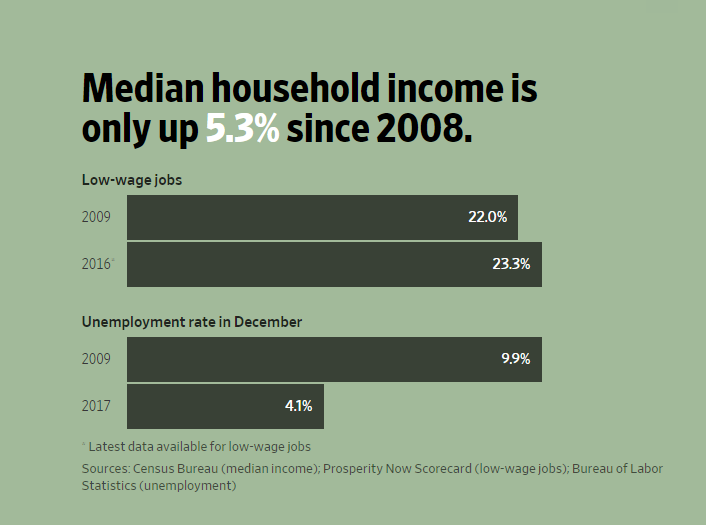

Median Income Barely Up

Forget averages. The median is what counts most.

Real median wages fell in 7 out of the last 11 years! For details, please see Imaginary Wage-Inflation Conundrum.

My discussion pertains to “wages”. The WSJ referred to “household income”.

Public Debt Triples

The MMT crowd says “We owe it to ourselves”.

Credit Rating Agencies

The guys that rated everything AAA in 2007 are still in charge of things.

Fannie Mae

They promised to unwind Fannie Mae. What happened?

More Ways To Invest

More ways to invest in fewer companies. Who can possibly find fault with that? The casino is open!

Revolving Doors Still Functioning

The revolving door concept still works.

Gotcha!

Batting one out of a thousand is arguably better than expected.

Wealth Distribution Trends

Who couldda possibly thunk that might happen when you bail out the banks, lower interest rates to zero, foreclose on millions of homes, send no one to jail, and promote inflation?

No one could possibly have predicted this result.

Mike “Mish” Shedlock

“Who couldda possibly thunk that might happen when you bail out the banks, lower interest rates to zero, foreclose on millions of homes, send no one to jail, and promote inflation?” Definitely not “wealth effect & courage to act” Bernanke

Thruthseeker Only 10 comments load at a time.

In terms of Gundlachs prediction of higher rates. I don’t see how the long end of the curve goes up much without crashing stocks, RE, and bonds of course. And those crashes in turn would cause rates to come right back down again as assets deflate. Can the inflated US asset markets handle a 10 yr T over 3%? Will there be a day where stocks crash, recession happens, but the 10 yr T goes up?

“Crisis Struck 10 Years Ago: What’s Changed?” The hole has gotten deeper. Now 233+ Trillion in global debt.

Truly the Road to Hell. As Chris Rea wrote:

And all the roads jam up with credit

And there’s nothing you can do

It’s all just bits of paper

Flying away from you

Two issues worth thinking about:

(1) How permanent is membership in the “1%”? Is it the same people in 2007 and 2016?

(2) The Power of Bad Ideas – like “National Debt”.

It’s important to look on the bright side of these running debacles: Assuming you are a one percenter, your rake will grow from 38.7% of the pie to 57% in only 25 more years, and if you’re a CEO today, jacking up your debt load to buy back stock to goose your comp plan, by that time, you’ll be well beyond having to worry about claw-backs.

I will tell you exactly what changed. After the bubble was popped and the wealth transferred multiple new bubbles were created with the originators already in place. Rinse repeat as many times as necessary to get the shiny clean results.

It should be obvious that proactive change is as rare as common sense. Is it any mystery why the establishment wants to confiscate guns? Ignorant Liberals may gladly follow their fearfull leaders off the cliff in their pursuit of Utopia, but patriotic conservatives will once again demonstrate that liberty is the line in the sand. So sad. I guess the only thing to do is to pray for Democrats and the rest of the establishment, for they know not what they do.

What’s happening is 96% of the mortgages are Gov’t backed in some way (fannie, freddie, fha, va). Private mortgage banks are originating these loans on the front end, but they are Gov’t backed loans in secondary market. Dodd Frank regulations are so draconian that no private non-Gov’t backed mortgage investors really want to step up. There is too much risk of liability and getting sued or fined by the Gov’t for not dotting an i or crossing a t. Compliance is too costly. Also, only the Gov’t will make a 3% down FHA loan at a 3.5%-4.5% yield. Who else would take that risk for that low yield?

Mish, you keep predicting deflation. Do you know of a historical example where a country ran huge budget and trade deficits and increased its money supply (M2) by 80% in the last 10 years and then seen its currency increase in purchasing power?

Once upon a time, mortgages were issued by banks and savings and loans, who then carried them on their books. As a result, they cared whether the borrower could actually repay it, so they cared about things like accurate appraisals, accuracy of reported income, and the character of the borrower.

Today, it remains true that, like 2008, mortgage originators resell the mortgages as quickly as possible, and thus have no particular concern over whether the borrower will actually be able to make payments, only whether or not the mortgage can be sold. That’s a recipe for fraud – overstated income, over appraised houses, aggressive sales of mortgages to marginally qualified people. That caused the crisis in 2008, and it will cause another one.

Eight years of obama economics in a nutshell.

They didn’t mention if the 5.3% figure used constant dollars or not. It may have.

Median income up only 5.3% while inflation “officially calculated” in the same period up more than than 15% …

‘The government has its hands on 96% of the mortgage market, if it can even be called a “market”.’

It can’t. It’s a racket. Pure and simple. No different from stocks, bonds, houses nor any other FIRE, legal and regulatory racket in that regard. Just another light obfuscation for excusing why it’s somehow OK for government to rob the productive, solely for the benefit of the idle connected. All while the latter prances around on generous, stolen welfare wearing Adam Smith pins. Too economically illiterate to even recognize the irony.

10 year treasury was also above 5% in 2nd half 2007, late into that cycle. Despite being 9 yrs into this current cycle, we are only at 1.75 on the FF rate and 2.74% on the 10 yr T.