The following snips are courtesy of Albert Edwards at Society General

Unit Business Costs and a Profit Squeeze

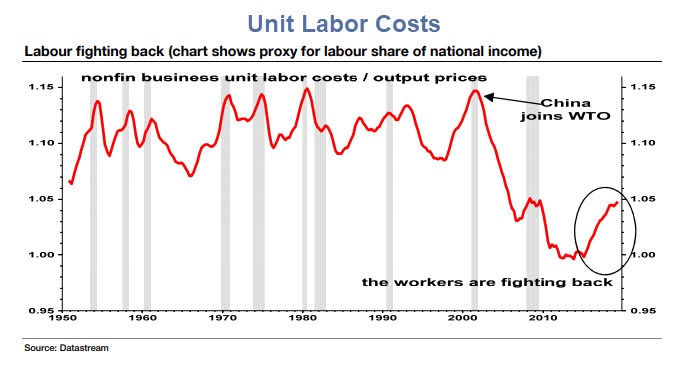

Aside from payrolls, the economic data has certainly been lukewarm. So that rapid payroll growth spells dire productivity growth. In short, the sharp 3% jump in unit labour costs in Q3 is crushing corporate margins (chart shows inverse).

Our US economist Steve Gallagher shows below that, if history is any guide, a recession is due just about now. Yet investors fear of recession has all but evaporated.

Extent of the Margin Squeeze

Recession Overdue

Regular readers will know that we have long believed that it is the business investment cycle that ‘causes’ recessions, in an accounting sense. The chart below shows the contribution of business investment to GDP growth. Although in an economic recovery business investment contributes a fraction of GDP growth, in a recession the dotted line totally overlays the red line – business investment ‘causes’ recessions.

Recent weak core durable goods orders confirmed what the latest Q3 GDP data also suggest: business investment has begun falling. Together with the margin cycle, this is a loud warning signal of recession (the false signal in 2015 was due to the collapse in shale oil and confined to only one sector).

Mish Comments

Thanks to Albert Edwards for an interesting set of charts.

Declining Profit Margins

Despite Q2 rebound, the broader story remains one of declining #profit margins since 2014 — the longest late-cycle contraction in post war history… pic.twitter.com/WZQa5hCuSj

— Gregory Daco (@GregDaco) August 29, 2019

Another fun fact.

Recent years have seen a decline in corp profit as % of GDP (I don’t have the post-revision numbers yet) as well as a decline in average corp tax rate.

Weren’t the lower corp tax rates supposed to boost corp profits??? pic.twitter.com/WLxSHkut8O— Asif Abdullah (@Asif_H_Abdullah) August 29, 2019

Rise in Employment Costs

I discussed the rise in employment costs yesterday in Labor Productivity Dives as Unit Labor Costs Soar

10 Reasons for Declining Productivity

Earlier today I gave 10 Reasons for Declining Productivity

Fed-sponsored Zombie corporations, debt, government spending and demographics are among my reasons.

Mike “Mish” Shedlock

So all the big Trump corporate tax cuts did nothing for the economy/society (evidenced by declining % of GDP), only benefiting the wealthy through (unproductive) corporate share buybacks.

No, just amused about the markets swings on the good/bad-on/off trade deals….

You just figuring that out now?

Doncha’ know, you should be fully in the market, because it’s up !

And that is what the reasoning has been reduced to….wait for it….”because it’s up”

And that is the reasoning to ignore reason.

Every few months, we get a new recession indicator that show a recession is coming soon. I’m sure that a recession will come. Those that predict it every quarter will eventually be correct. In the interim, we can all enjoy a growing economy and a rising market.

Société Générale and not Society General

Insolvent without state backing, no matter how you spell it

Here is the most recent GDP by state. The exodus from California is helping the desert southwest and Texas. The rest of the country is effectively sitting at < 2% GDP. Washington state is the Amazon effect that is helping the country too.

Nice try California boy… California still has lots of Libtards, pooping homeless, needles, rats (the vermin, not CA’s Congressional reps) and both state and local governments dominated (for decades) by democrats. All the things that make California the 3rd world sh!t hole that it is.

The rest of the country is growing because they are NOT emulating California’s stupidity

Turns out Texas isnt so great when it comes debt either. Here is the breakdown of state and local debt per capita. Texas is actually catching up to California from a debt perspective. By 2024 Texas will turn blue but there will be no one to blame but a state that was run by Republicans for nearly 25 years

link to taxfoundation.org

PS — I am giving you the level of respect that you “earned” by moving into Californa even knowing it is a disaster. I don’t give respect just because you think you are entitled.

Respect is not a participation trophy.

Nice try country bumpkin who failed in NYC. I wouldnt take your respect as it’s well beneath me on any socioeconomic scale. You are a simpleton country bumpkin and this is why you failed in NYC.

Your making yourself look stupid again with the namecalling and pegging me as one thing. Keep failing.

Even a dumbshit like you can see 2 is the average and 1.9 is basically average. It is obvious to see the worst part of the country isn’t the west. It is actually holding up the country. The northeast and midwest are dragging the country down.

Oh yeah. Add the deep south to dragging the country down.

Not a single state is in recession. Very difficult to believe.

Inflation (aka cost of living) is radically understated along the two coasts, and overstated in the geographic middle of the country (inflation is close to zero in the middle of the country, but close to 4-5% along the coasts).

Subtract 2.2% from the numbers along the coasts, and add 1-2% to the states in the middle. That would give a more accurate picture

You are correct. Anyone knows that when it says “real” it is already adjusted for inflation. I looked up the consumer price index by region. In the western states it is actually 2.6% and the rest of the regions are 1.3 or 1.4%. So growth it actually even higher in western states as you would need to add back the 2.6% CPI. Basically the west and Texas are carrying the country when it comes to growth.

In other words no one gets to make up their own country bumpkin math by subtracting from one region and adding to anothere region. Even the village idiot knows inflation is positive for all regions.

A year ago when the yield curve supposedly inverted (due entirely to Fed manipulation), we were told that “proved” recession was unavoidable and GDP would be negative by early 2Q2019… guess these talking heads don’t really have all the answers.

Parts of the economy (California and northern cities with bloated bureaucracies and massive debt) are in recession, the south is growing gang busters (often with transplants fed up with big government up north). On average, the economy is growing 1-2% — but lower numbers in government land, higher numbers in areas with more reasonable levels of government.

“Together with the margin cycle, this is a loud warning signal of recession”

…

The Brotherhood of CFOs desperately need a kitchen sink quarter (or 3).

Low rates have allowed the lump under the rug to turn mountainous.

Looking forward to what a good cleaning will bring out …

“Interesting to see rise in corporate #profits in Q2:

…

He tweeted that August 29th. Q2 profits since revised down to +$75.8 billion

We are back to slow growth levels under Obama which isnt surprising. That means low investment levels and slow growth.

How does it all compare to Europe and the rest of the world that are seeing their mountains of dollar-based debt rise with a rising dollar?

Yield curve says no. It’s go-go!

Corporate profit margins don’t have the meaning they use to have. With government deregulation, corporations now hide their profits for tax purposes. Shareholder are rewarded with stock buybacks, not profits. What used to be profits are now debt payments to PE firms and banks.

“Corporate profit margins don’t have the meaning they use to have.”

…

The worm will turn. In 2013 (or there abouts) Bernanke said corporations had reaped $800 billion in interest savings rolling over debt into lower interest bonds. That has ended. And rates will go up as covenant lite garbage starts to go belly up.

A lot of retailers are going under. And it’s not entirely because of Amazon. They kept adding on debt and hit a point where they could no longer pay the interest. I suspect there are a lot of companies in sectors not quite as bad as retail that will soon follow.

Mish is making a recession call, it must be a day ending in “y”.

A report from Bisnow. “A strong jobs report, the stock market performing at record highs and low interest rates continue to fuel U.S. commercial real estate’s prolonged growth cycle. But overall economic growth has fallen as the year progresses, raising commercial real estate’s favorite question: How much longer can it all last? ‘I still, to this moment, don’t get it, other than there’s still a significant hangover from the financial crisis,’ Walker & Dunlop CEO Willie Walker said. ‘You’d think people would stretch lending standards, but they haven’t.’”