by Mish

Yet, ECB president Mario Draghi has promised to maintain QE asset purchases, and Italy has no other real buyer for its bonds.

What’s Draghi to do?

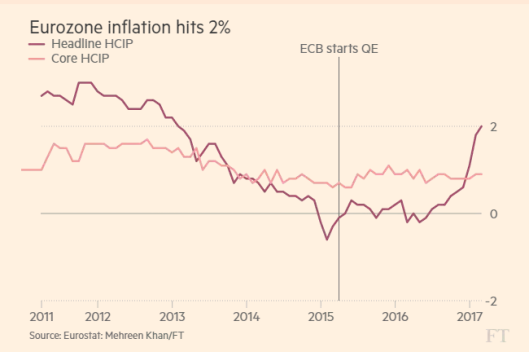

Headline Inflation Hits Two Percent

A milestone.

Annual inflation in the eurozone accelerated to hit 2 per cent for the first time since January 2013 last month, underscoring a sharp rise in prices driven by higher energy costs in the single currency area.

February’s year on year inflation reading, which rose from 1.8 percent and was in line with analyst estimates, comes as inflation hit 2.2 per cent in Germany last month and registered over 3 per cent in Spain.

The eurozone’s core inflation measure, however, which strips out volatile energy and food prices, remained unchanged at 0.9 percent and has remained stubbornly below 1 percent since August 2013.

Inflation Dilemma Headache

With rising inflation, ECB hawks set to crank up pressure for a move towards exiting aggressive monetary easing. This poses a Policy Dilemma for Draghi.

Mario Draghi will get a clear message from European Central Bank hawks next week: drop the doom and gloom.

After four years of weak growth and below-target inflation, price pressures have returned more quickly than the bank expected. Eurostat, the European Commission’s statistics bureau, on Thursday reported that prices rose 2 per cent in the year — rising above a central bank target of “below but close to” 2 percent for the first time since January 2013.

The central bank continues to hold interest rates at historically low levels and has promised to buy €780bn worth of bonds this year as part of its landmark quantitative easing program. Both the rate cuts and the QE program have been a long-running source of irritation, notably among the German political and economic establishment. Influential voices in Berlin have seized on higher German inflation — the country’s annual price rises reached 2.2 per cent in February — to call for rate rises.

Mr. Draghi has so far pledged that he would be ready to cut rates even lower and buy more bonds. His promise is that interest rates would “remain at present or lower levels for an extended period of time”.

ECB Dissent

Last month, Yves Mersch, a member of the ECB’s executive board, asked: “How much longer can we continue to talk about ‘even lower rates’ as being a monetary policy option? Considering the importance of credibility for a central bank, as mentioned, there should be no delay in making the necessary gradual adjustments to our communication.”

Jens Weidmann, Bundesbank president, said this week that the central bank would need to raise its forecasts for inflation this year by as much as half a percentage point from a projection of 1.3 per cent, made in December.

What’s Draghi to Do?

The short answer is nothing.

The long answer is Draghi will likely say something like wage growth is weak, energy prices are transitory, and the ECB will instead focus on core HCIP (Harmonized Index of Consumer Prices, roughly equivalent to the CPI in the US).

Thus Draghi won’t hike, and he is not even likely to taper bond purchases yet.

Italy on Life Support

Italy is on life support and needs a buyer for its bonds. Italy’s 10-year bonds yield 2.138%. Germany’s 10-year bond yield is 0.324%.

The spread between 10-year Italian bonds and 10-year German bonds is 181 basis points (1.81 percentage points).

If there was no risk of default, the yields would be the same. Italian bonds are at a premium for a reason. And if the ECB stopped buying Italian bonds, the spread would grow dramatically.

Mike “Mish” Shedlock