The Census Bureau’s report on Manufacturers” Shipments, Inventories, and Orders for April shows a factory sector that cannot gain traction.

Summary

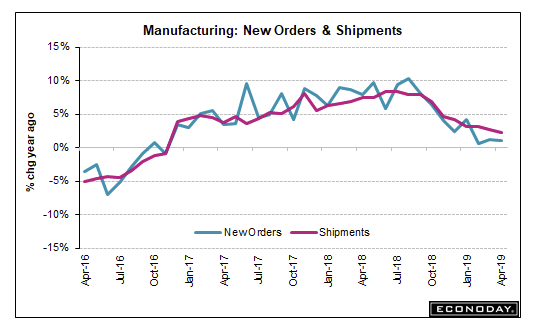

New orders for manufactured goods in April, down two of the last three months, decreased $4.0 billion or 0.8 percent to $499.3 billion, the U.S. Census Bureau reported today. This followed a 1.3 percent March increase. Shipments, down following two consecutive monthly increases, decreased $2.7 billion or 0.5 percent to $504.1 billion. This followed a 0.2 percent March increase. Unfilled orders, down two of the last three months, decreased $0.6 billion or 0.1 percent to $1,179.3 billion. This followed a 0.1 percent March increase. The unfilled orders‐to‐shipments ratio was 6.69, up from 6.61 in March. Inventories, up seven of the last eight months, increased $1.8 billion or 0.3 percent to $692.9 billion. This followed a 0.4 percent March increase. The inventories‐to‐shipments ratio was 1.37, up from 1.36 in March.

New Orders

New orders for manufactured durable goods in April, down two of the last three months, decreased $5.2 billion or 2.1 percent to $248.6 billion, unchanged from the previously published decrease. This followed a 1.7 percent March increase. Transportation equipment, also down two of the last three months, drove the decrease, $5.3 billion or 5.9 percent to $85.5 billion. New orders for manufactured nondurable goods increased $1.2 billion or 0.5 percent to $250.7 billion.

Shipments

Shipments of manufactured durable goods in April, down three of the last four months, decreased $3.9 billion or 1.5 percent to $253.4 billion, up from the previously published 1.6 percent decrease. This followed a 0.5 percent March decrease. Transportation equipment, down four consecutive months, led the decrease, $3.7 billion or 4.1 percent to $85.9 billion. Shipments of manufactured nondurable goods, up three consecutive months, increased $1.2 billion or 0.5 percent to $250.7 billion. This followed a 0.9 percent March increase. Petroleum and coal products, also up three consecutive months, led the increase, $1.1 billion or 2.0 percent to $56.2 billion.

Unfilled Orders

Unfilled orders for manufactured durable goods in April, down two of the last three months, decreased $0.6 billion or 0.1 percent to $1,179.3 billion, unchanged from the previously published decrease. This followed a 0.1 percent March increase. Transportation equipment, also down two of the last three months, led the decrease, $0.4 billion or virtually unchanged to $810.7 billion.

Inventories

Inventories of manufactured durable goods in April, up nine of the last ten months, increased $1.7 billion or 0.4 percent to $422.4 billion, unchanged from the previously published increase. This followed a 0.3 percent March increase. Transportation equipment, also up nine of the last ten months, led the increase, $1.5 billion or 1.1 percent to $136.1 billion. Inventories of manufactured nondurable goods, up four consecutive months, increased $0.2 billion or 0.1 percent to $270.5 billion. This followed a 0.5 percent March increase. Petroleum and coal products, also up four consecutive months, drove the increase, $0.5 billion or 1.3 percent to $42.2 billion. By stage of fabrication, April materials and supplies increased 0.1 percent in durable goods and decreased 0.2 percent in nondurable goods. Work in process increased 0.9 percent in durable goods and was virtually unchanged in nondurable goods. Finished goods were virtually unchanged in durable goods and increased 0.3 percent in nondurable goods.

Boeing Yet to be Felt?

Econoday had some interesting comments.

- At an as-expected minus 0.8 percent, April’s factory orders report closes the book on what was a weak month for US manufacturing. The split between the report’s two main components shows a 0.5 percent rise for nondurable goods — the new data in today’s report where strength is tied to petroleum and coal — and a 2.1 percent dip for durable orders which is unrevised from last week’s advance reading.

- Core capital goods (nondefense ex-aircraft) are very weak in the report, down 1.0 percent for orders and unchanged for shipments. Both readings hint at slowing for second-quarter business investment. General weakness is evident in the market breakdown with orders for primary metals, fabrications, machinery, and new vehicles all weak.

- Data on civilian aircraft are always volatile month-to-month but April’s declines in new orders and unfilled orders were limited, suggesting that possible effects from the 737 grounding have yet to hit. Aside from this, however, the April factory report is consistent with a sector that continues to struggle and, unlike last year, does not look to contribute to 2019 growth.

Inventories, New Orders, Shipments

Year-Over-Year Numbers

- New Orders : +0.34%

- Shipments: +2.39%

- Inventories: +4.97%

Inventories are up for the 9th time in 10 months.

The inventory build added substantially to 4th-quarter GDP.

Mike “Mish” Shedlock

Everyone wants to be like Draghi.

Capitalism without bankruptcy is like Christianity without hell. (wish that was my quote, but it ain’t.) 🙂

What a mess. Thanks to our friendly Fed, American Manufacturing hasn’t been forced to dump zombies and shoot straggler products for ten years now.

And just when C suites were feeling better about continuing to jack their comp plans, and debt loads, with stock buybacks, someone slips a trade war under the door.

In manufacturing, you can run, but you can’t hide from a shrinking backlog. Three consecutive down-ticks, year-on-year, in new orders, along with growing WIP and inventory will soon be throwing negative product cost variances and forcing supply trains to slow.

All big gov’t ,DOD,that means to drive durable weapons….er er er “goods”into the black ,DC will need to borrow moar cash asap.And the fed will not disappoint, tsunami of fresh money printing on the way,along with first ever NIRP,gloves are coming off and the printing presses are gonna run like they’ve never run before!

I’m afraid that you are correct. To infinity — and beyond!

When does it end?