WirePoints reports Chicago Mayor Rahm Emmanuel wants a Constitutional Amendment to address Illinois Pension Woes.

The mayor’s plan cannot possibly work because Chicago is far too deep in pension debt to do anything but default.

Nonetheless there is some benefit in the idea for the simple reason it may force the legislature to think about things as they are, not as they want them to be.

Kudos to Rahm Emanuel for broaching the subject of a constitutional amendment for pensions and for using cost-of-living adjustments as an example of why the amendment is so necessary.

The possibility of an amendment in Illinois has experienced a revival of sorts since Arizona recently amended its constitution for a second time. Already, the Chicago Tribune, Crain’s and Mayoral candidate Bill Daley have supported an amendment in some form. And COLAs are finally being recognized as a key driver of Illinois’ pension crisis.

However, it would be a mistake – as some may be tempted to do – to think that an Illinois fix is as simple as COLA reforms via a narrow, Arizona-style constitutional amendment. Instead, Illinois needs an amendment that’s as broad as possible if it hopes to fix the pension crises playing out all over the state.

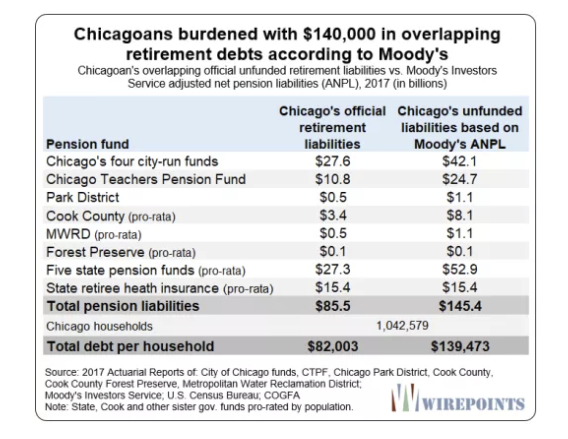

Collectively, Illinois governments owe more than $400 billion in pension debts alone, based on Moody’s most recent methodology.

Its a particular problem for Rahm Emanuel, as Chicagoans are the most swamped of all. Each city household is on the hook for $140,000 in overlapping state and local retirement debts.

Piecemeal Approach Cannot Work

WirePoints discusses changes in Arizona and accurately concludes piecemeal changes won’t work for Illinois.

Here’s a hint, they won’t work for Arizona or any other state or municipality either. Ridiculous COLA adjustments are only a tiny piece of the problem.

More Substantial Fixes Needed

WirePoints concludes and I agree, “Any Illinois amendment should repeal the protection clause and say expressly that the state may modify past and future pension benefits notwithstanding the state constitutional contract clause or anything else in the Illinois constitution that might conflict.”

Of course, Labour unions could and would appeal that, all the way to the US Supreme Court. The process could take years.

In Wirepoints’ view such appeals would fail.

Mish’s Better Approach

I have a far simpler approach that is 100% certain to work, and work faster.

- Illinois can allow municipal bankruptcies

- The Federal government can pass national legislation allowing municipal and even state bankruptcies

Q. How does that fix the problem?

A. As we have seen in Detroit, Michigan; Central Falls, Rhode Island; and numerous cities in California, pension promises are not sacrosanct in bankruptcy.

As it stands, states can allow or prohibit municipal bankruptcies, but if allowed, Federal laws take precedence over state rules. In bankruptcy, pension obligations can be reduced. They were hammered in Central Falls.

In Illinois, I would expect the City of Rockford to file bankruptcy the moment it could. Rockford is Illinois’ third largest city.

Such a bankruptcy would send shock waves through the bond markets, but also where reform is needed most: Illinois pension plans.

Bankruptcy reform would put huge pressure on unions to reduce demands in a fair manner (highest pensioners get the biggest cuts), rather than leaving matters to the courts to decide where the cuts happen.

Bankruptcy reform would in and of itself likely ensure that the state would get around to fixing, via constitutional amendments, its other pension problems.

The advantage of my approach is we would not have to wait for a constitutional amendment. It would come later.

Mike “Mish” Shedlock

The average household retirement savings is $95,776. The median is $5,000! You want the average family that has not save adequately for its own retirement to shell out $140K so a city worker can retire way better off at 50!! Hell no!

The funny thing is the unions have stoked the flames of anger against the 1%, only to find out they ARE the 1%! So, don’t expect any sympathy when the taxpayers tell them to piss off.

MMT points out that the federal government can never go bankrupt nor does it need to save or borrow its own dollars [it’s in the Constitution] so pension schemes which by nature expand over time need an inextinguishable source of funds to operate as they promise. ONLY the Fed can do it. All private and state pension schemes need taking over by the fed to keep faith with their pensioners. It can deficit spend whatever it costs with no threat of inflation and no residual debt. [That’s what deficit spending does]

It’s per household, not each Chicagoan. Regardless, it’s a statistic that every news site should be showing on the front page. This is plunder, plain and simple.

We don’t need any ‘solution’ because there is none practically speaking. What we need is a recession bad enough that these pension funds fail naturally. Hopefully it happens during a Republican administration because pension bailouts are less likely.

As one of those pigs at the trough (I know you hate unions but you never explained why or even tried to see it from the other side) who is not a union person generally, Im not a fan of pensions of any kind, in that to expect any business or govt body to maintain its form for 30-60 years to pay out the pensions was silly from the get go. What we need of course are very generous “401ks” and mandatory contributions to both stocks and guaranteed income components. For those of us with 5 years left, we have made plans around a 33-50% of pay pensions for 20+ years, and yanking it at the last minute is just mean. There are plenty of pigs at the Illinois trough that arent pension situations. And have we forgotten that “rich getting richer and everyone else going nowhere” inconvenient fact?

“For those of us with 5 years left, we have made plans around a 33-50% of pay pensions for 20+ years, and yanking it at the last minute is just mean.”

It has nothing to do with meanness, it has to do with math. The Year of Jubilee came every 50 years. There is $250 trillion in global debt. What Chicagoan has $140,000 to pay for government pensions, as well as their own retirement? With public unrest,Yellow Vest movements are spreading and war drums are beating.

Ron,

The resentment is that in negotiating the pensions, no one represented the tax payer. The “negotiations” were between a union representative, and a state employee, who no doubt also gets a pension. It all went on, hidden from public view, and the growing deficits were hidden by overly generous assumptions about furture returns. Only now, many years later, when it is far to late to fix, and when the people that agreed to it are along forgotten, does it come into public view.

Wait til you see a couple years of down markets!

Why would anyone live in Illinois?

A better question is how such a corrupt and enslaving system could be established in the first place…

Same mechanism as Venezuela a bit earlier. And the rest if the West a few years later: The pagan god of demoooocraciiii.

In progressive dystopias, all people are told she is some form of unchallengeable, universal, end of history, deity. And the dumb amongst them, even believe it. All the way to the streets of Caracas.

Indeed, Stuki. The fact that democracies are short lived, and end badly has long been well understood. They always deteriorate along the same path, career politicians getting elected based on promises to give things to people or do things for them, until the government collapses in bankruptcy, unable to fulfill the promises. But, one of the strengths of the US is that not all states deteriorate at the same rate, and you have freedom to move to a state which is not so far along as Illinois.

As long as “saving the system”, means the Federal government and its central bank can, hence will, overly or covertly, transfer resources from the still productive, to the true basket cases, there is a very hard limit on how far behind Illinois anywhere will ever get. It’s kind of nice being able to pick favorites amongst turds in a sewer, I suppose; but from a practical POV, I’m not sure how meaningful it really is.

2banana’s Rule:

Long term democrat rule + public unions + free sh*t army = misery, ruin and bankruptcy

Public unions are, by far, the largest all time political campaign donors. And they give nearly every penny to democrats.

No democrat candidate could win a primary or general election without the public union’s money and support.

Democrats pay back public unions with insane benefits and pensions in government/public union contracts.

In turn, public unions are usually “closed shop” forcing, as a condition of employment, membership. Public unions also take their union dues before a public union employee ever sees their paycheck. It is one corrupt feedback loop.

The democrats will never turn on public unions. Even when their city turns into a Detroit and is in ruins.

That’s the most likely outcome: As long as there is a single, even remotely productive, non leech left within reach of the thieves which comprises all of every US level of government, they will not leave him unrobbed, in their effort to save their system of unconstrained theft.

Hence, there is no even remotely viable solution but a raised middle finger default at the Federal level, along with a return to sound money. Anything less is just naive and childish buying and selling of Brooklyn bridges on the cheap over and over, while uncritically and mindlessly cheering for one half retarded caudillo, “promising” something he doesn’t even understand the meaning of, after another.

Absent sound money and a principled repudiation of the validity of all debt taken out by long gone governments, there will exist a backdoor allowing unconstrained bailouts. Which means there will be more and more unconstrained bailouts. And less and less of anything else, as bailouts keep consuming ever more of a declining society’s ever dwindling resources. Leaving Americans stuck in this Dystopia, infinitely worse than Mogadishu in the 90s, forever.

“Anything less will be deflation an order magnitude not seen since…..I don’t know when.”

There is deflation and there is deflation. Inflation is the deflation of the value of the money. In Zimbabwe everyone became a billionaire in the local currency, but it wouldn’t buy much of anything, as its value was extremely deflated. If you have no money or the money is worthless, the outcome is the same.

I know this sounds crazy, but I think the most likely outcome is the governments sell themselves off. Not just real estate. Entire government functions. Much of government work is contracted out and the contractors do all the work. At least that’s been my experience. Why not just contract out the entire government? Companies bid and they charge a certain amount of taxes in return for services. Maybe have an election. Instead of electing individuals, you elect a company to be the government. Part of the campaign is how they handle pensions.