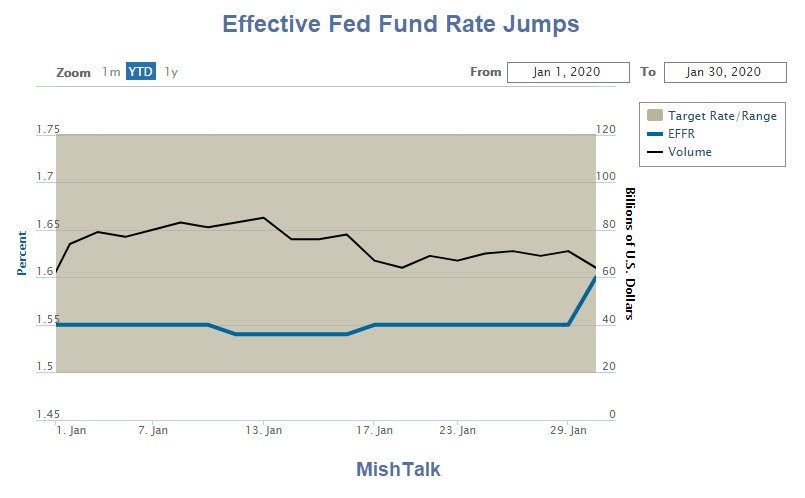

Highest All Year

I do not know the cause but the Effective Rate jump seems unusual.

My Conversation With the 30-Year Long Bond

In My Conversation With the 30-Year Long Bond I noted a “solid wall of inversions” from the three-year note through the Fed Funds Rate.

The Fed Funds rate would not be inverted with the 3-month and 6-month T-Bills without the Fed Funds Rate jump today.

Recall that it was a Fed Ends Rate jump that kicked off the Repo Crisis.

Mike “Mish” Shedlock

The big message I believe everyone is missing about the bond market is, “It’s the duration mismatch, stupid.”

As Mish has explained in past posts, lenders borrow at low rates for short terms and lend at higher rates for longer terms. Lenders have to roll over their short term loans until their customers repay longer term loans. Lenders pocket the difference between the yields. By realizing the existence of a disinflationary environment and that yield curves rarely invert; lenders overcommitted to a perceived low risk / high reward trade. It’s not the “free money” of an arbitrage, but pretty close.

As declining inflation takes hold, yields come down. Spreads between loan durations shrink. To hit profit targets, lenders have to take greater duration risks. Instead of lending for 10 years financed with 5 year loans rolled over once, lenders might lend for 10 years by financing with a 2 year loan rolled over 4 times. This places more demand on short term lending; resulting in short term rates rising relative to long term rates. Eventually lenders reach the point of financing long term using overnight lending.

Once the yield curve inverts at the short end, one could ask, “Why not borrow long term at lower rates and lend short term at higher rates?” Initially that does start to happen. Some lenders are willing to finance several sequential overnight loans with a single one month loan. Since there is a statistical risk of an inverted yield curves lasting a short period of time, lenders are willing to take a small duration mismatch in the other direction. Some of those rolling over loans begin to close their duration mismatch a little more aggressively by financing with longer short term loans. Now demand increases at the 2 month duration, which morphs into longer and longer durations. Bond markets are pretty much completely inverted for all duations. Duration mismatch can no longer be used to maximize profits. Too many lenders still have loans to roll over, but no one to finance them. Bank reserves are insufficient to repay the short term loans and still meet reserve requirements. Liquidity has dried up to the point US bills and Treasuries can’t be sold on the open market to avoid defaults.

In late summer 2019 the Federal Reserve stepped into the repo market “to provide liquidity” by purchasing US bills and Treasuries. If the Federal Reserve had not stepped in, many short term loans lenders took out would have defaulted, creating an insolvency chain reaction. The fact that the Federal Reserve has publicly stated its operations will last for months is a testament to severe structural imbalances duration mismatch has created.

This has lead to a scholarly debate of “Not Quantitative Easing” vs “QE”. I’ll take the “Not QE” side of the argument. Based on the above analysis, “Not QE” is a euphamism for “insolvency crisis”. Given the inverted yield curve, companies and home buyers already have every incentive to borrow large amounts of money at historically low costs; so there are no capital constraints holding back the economy.

None of the Federal Reserve’s “Not QE” efforts can fix the duration mismatch alone. A change in banking regulations is required to prohibit duration mismatch. It won’t matter if such a regulation is phased in slowly or instantly because investors decide on how fast changes in regulation will affect their investments. The amount of short term loans needing to be rolled over also effects how quickly policy change will impact portfolios. Yields would necessarily have to rise once duration matching starts. This would crash both the stock and bond markets.

The Federal Reserve has several short term options to kick the can down the road. It is already stepping into the repo market. Overnight repo can become the remainder of the bill’s or Treasury note’s duration. This is a limited solution because lenders have a limited supply of US bills and Treasuries in their portfolio. The Federal Reserve could reduce banks’ reserve requirements. This is also limited.

The Federal Reserve really doesn’t have any long term tools with positive outcomes. The Federal Reserve can lower it’s overnight rate in an attempt to normalize the yield curve from the short end. The drawback is retail depositors would have to pay storage fees instead of receive dividends. Selling long term US bonds to normalize the yield curve would harm long term economic growth. Adding corporate debt to acceptable repo assets would require a rule change. Such a move should create a fear that markets would no longer be truly free, but at least the perception of hyperinflation can be avoided. None of the above solutions discourages duration mismatch, the risk that has finally destabilized the

financial system.

Too long a post for me to read, so I add to the first paragraph. Borrowing short in the gc repo market, and lending long (such as buying long dated bonds) wouldn’t go far for a hedge fund. So they lever up >10 times the same collateral, and voila, you have a decent return on base capital. This work when you can roll over the short borrowing, but you’ve got an LTCM when repo rates blow up.

Similar strategy worked like charm until 2008. With FED’s backing, only the taxpayer can lose.

Yup. Which is why US banking is absolutely whacked for the next few decades. As spreads will be compress and go negative, and rising asset prices can no longer be relied upon to facilitate repayment of loans as interest rates go lower. Higher short-term rates are absolutely and utterly toxic to the US financial sector, insurers, pensions, etc., who have built their business on “borrow short, invest long”. The reckoning will be epic, especially in an environment where the stock market has priced in extremely rich future earnings based on a believe that interest rates would continue to significantly fall. A classic overshoot at the long end of a bubble behaviour.

Maybe finally, instead of bankers (and their lackeys such as lawyers, accountants, etc.) getting all the ‘glory’ in the economy, leadership can move to actual producers and productive people.

I believe we are in agreement, more or less. In an effort to avoid a crisis the Fed has been forced to deal with a liquidity issue in repo rates since a sudden and dramatic surge began in September. While it is difficult to see the difference between QE and an injection aimed at maintaining liquidity, in this case, several reasons exist to believe this is not QE.

A strong dislike and distrust of the Fed should not blind us to the idea this may still play out in many ways. More on this subject in the article below.

This tells me there is short term worry in the system.

The more valuable morsel of information was in the previous post: link to moneymaven.io

In the replies: FED extend the long term repo facility at least until April. This was supposed to be a one off, in September. Also in the news, FED floating the balloon of extending this facility to hedge funds (short cutting the banks).

It says a lot.

Question for Mish. Without government stimulus, are we in a recession and how far back does it go?

Yes. 1971.

Permanently collapsed economy will force the fed’s hand with the nuclear option of a one two punch of deep NIRP/QE 5 cocktail by summer in desperate attempt to stave off collapse of the govt before elections.Govt collapse will be the excuse the Trump junta needs to seize power and cancel elections.

Ask yourself this question – Would any politician be any different?

If your answer is “yes” I think that’s your problems.

None of the Washington rats are like you and me. There is Royalty and the peasants. We are the peasants.

Worse than peasants: Slaves. Sufficiently indoctrinated to volunteer for that role.

Peasants at least have access to pitchforks, rope and tree branches. And they have the brains to realize those who rob them of their output are plain thieves. The current crop of pliant illiterates, OTOH, instead stand around and cheer for Dear Leader when he strips them of even those basics of freedom. Begging for him to do more of it, even.

Then handing that, and other, loot, in the form of ever more intense surveillance, arbitrary “law” enforcement and other, obvious to anyone literate, public displays of totalitarian overreach; to the undifferentiated mass of abject middlebrows which are being designated “royalty” in this dystopian, progressive DumbAge.

“This time is different” ?

It’s not our economy that’s on the precipice of collapse. It’s the rest of the world holding too much dollar-based debts, that cannot tolerate a rise in interest rates, or the US dollar. This is who the Fed is trying to save, at the expense of savers and pensions.

The effective fed funds rate went up because the fed hiked interest on excess reseveres (making it more profitable to lend to fed then to lend to repo market overnight)

I am headed out for the evening. There is a better thread in which to reply here:

My Conversation With the 30-Year Long Bond

Hello Mish

Is not the FFR the “sparest of spare liquidity” as Jeffrey Snider of Alhambra put it? Sniffing out problems in the air?

If Sniders views are anything to go by Bonds and Gold are both signalling fear – somewhere out in the shadow banking system. But collateral Gold will sell off first if the liquidity issues are ever permitted to surface – “effective Repo operations” by the Fed notwithstanding.

Gold may fall sharply if control is lost, as Liquidity trumps Fear.

I do wonder how much Gold is used as collateral but sharp sell offs occur from time to time that seem to suggest the figure is not at all insignificant.

BIS rules changed in 2019 to make Gold a Tier one asset. I wonder if this has stabilised Gold volatility somewhat? More relevant I think is the bid for Central Bank Gold. Gold’s virtue as a non US Dollar asset purchasable in any currency that can be converted to US Dollars in a flash.

This is what worries me most. Gold is so damned liquid, if there is an uncontrolled bid for US dollars again, Gold will suffer a sizeable take down.

When?

You need to think about things in a slightly different fashion: investors would need to value the Dollar much more highly than gold for gold to fall precipitously.

Gold can (and most likely will) fall fairly soon, but not far enough to hurt you. Gold is the trade du jour. As long as you are un-levered you will be fine.

“You need to think about things in a slightly different fashion: investors would need to value the Dollar much more highly than gold for gold to fall precipitously.”

Bingo

Sorry second link….

Blow it link to ftalphaville.ft.com interbank repo effect and goldfect-and-gold/ via@FinancialTimes

Why didn’t I just link this?

Here we go…

Thank you Lege, very well said. Steep sell offs in Gold must be expected from time to time. I expect one again as Liquidity trumps Fear.

I am not leveraged to Gold which means I can thankfully hold my own into a downturn. In this regard, as a precaution, I sold my gold shares quite fortuitously on 31 August 2019 ahead of the last repo tremor. I have watched these shares fall sharply and then recover, but fail to test those late summer highs.

The Gold/Hui divergence on the face of it suggests I am not the only investor wary of yet another collateral call “wash out” that would affect all other assets not nailed to the deck. Except perhaps US Treasuries and the US Dollar.

Not only will rates rise (driven by risk), but don’t expect the 30-yr mortgage to be available in the next decade. No one will trust govt, especially when they renig on pensions, and FDIC does not protect depositors from bail-ins.