On Friday, I emailed Pat Higgins a couple of questions.

“Hi Pat, can you isolate the impact on GDP today, distinguishing the decline due to employment vs the factory report? And regarding employment, was it the anemic wage growth as opposed to the decline in employment that impacted PCE and residential investment?”

Pat Higgins’ Reply

The revision in the model’s dynamic factor led to most of the declines in the PCE, equipment, nonresidential structures and residential investment contributions. If one simply replaces today’s estimates of the factors from July – December [the November and December values are forecasts] with the values from Wednesday’s published update, then the growth rates of these components are all within a few tenths of their values from yesterday. The October value of the dynamic factor is going to be heavily influenced by the employment report, rather than the Census manufacturing report, because the Census manufacturing data only goes through September. Here is what we wrote on our public blurbs for the last two updates:

Friday’s Update:

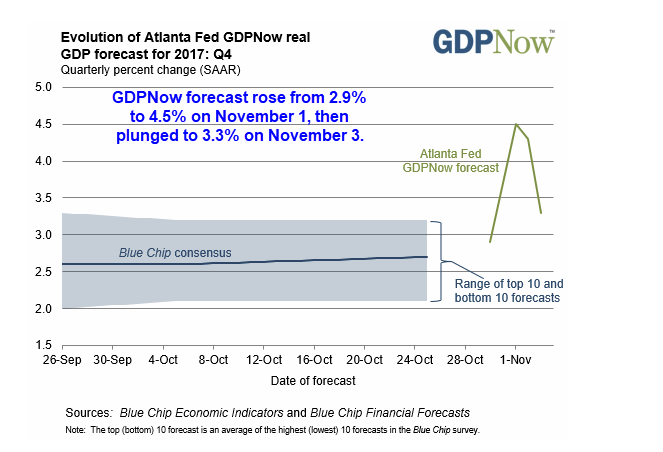

The GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2017 is 3.3 percent on November 3, down from 4.5 percent on November 1. The forecasts of real consumer spending growth and real private fixed investment growth declined from 3.9 percent and 8.7 percent, respectively, to 3.2 percent and 6.0 percent, respectively, after this morning’s employment report from the U.S. Bureau of Labor Statistics. The model’s estimate of the dynamic factor for October—normalized to have mean 0 and standard deviation 1 and used to forecast the yet-to-be released monthly GDP source data—declined from 1.50 to 0.63 after the employment report. The forecast of the contribution of inventory investment to fourth-quarter real GDP growth declined from 0.14 percentage points to -0.03 percentage points after this morning’s manufacturing report from the U.S. Census Bureau.

Wednesday’s update:

The GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2017 is 4.5 percent on November 1, up from 2.9 percent on October 30. The forecasts of real consumer spending growth and real private fixed investment growth increased from 2.8 percent and 4.4 percent, respectively, to 4.1 percent and 8.8 percent, respectively, after this morning’s Manufacturing ISM Report On Business from the Institute for Supply Management. The model’s estimate of the dynamic factor for October—normalized to have mean 0 and standard deviation 1 and used to forecast the yet-to-be released monthly GDP source data—increased from 0.04 to 1.43 after the ISM report.

Along with roughly 100 other series, the model uses something like 22 payroll employment series from different industries at various levels of aggregation and two from the household survey to estimate the dynamic factor. It doesn’t use any wage data from today’s employment release.

Most of the downward revision was in the inventory contribution to growth was, mechanically, due to an upward revision the model’s estimate of change in private inventories for the third quarter after today’s manufacturing report. See cells E26:F27 in the tab TrackingHistory of the online spreadsheet.

Best regards,

Pat

Tracking History

The dynamic model reacted most to the employment data. But in contrast to my expectation, the anemic wage growth was not the precise culprit.

Once again, Pat Higgins was very generous with his time in explaining his model.

Mike “Mish” Shedlock

wow a dustup over an indecipherable scholarly bit on the metaphysics of GDP. so what is a dynamic factor, how many dance on the head of a pin?

Let’s revisit this discussion in mid January after the holiday shopping season which looks to be an absolute blowout. I think 4.5% is too low and we will be seeing GDP in the 5.x%. I’d durable goods, industrial production and auto sales continue at record levels with record high backlogs and new orders then we can see GDP of over 7%, which I believe happened in only one quarter since 2003. Now tell me where do you see deflation or the fed not meeting target of 2%??? The economy is facing serious inflationary pressures bottlenecks in production, a shortage of labor, and record high consumer demand and never before has credit been easier to get or interest rates have been this low for this long

Big man Mish realizes he made a foolish comment, and rather than admitting that he massively overstated the expertise of these tenured academics — he threatens to cut off debate and censor me like he is Rajoy or some other EU politician.

Your blog isn’t what it used to be. This new maven net thing is an annoying format. The really good commenters have become frustrated and moved on to somewhere else. Time for me to do the same.

“No point in anyone commenting here…Only “enlightened academics” have valid opinions, according to Mish. Everyone else should shut up and pay higher taxes and higher tuition so that we may hear the opinions of quacks that don’t live in the real world.”

Medex one more asinine comment like that and you will take a week break or longer. I cannot sand it when people claim I said things I didn’t. I challened you to dispute what they said. You respond with bullshit. Last warning.

@truthseeker — groups that don’t pay property taxes, capital gains taxes on endowments and issue tax-exempt debt are in no position to comment about taxes or regulatory policy. Tell me the opinion of a single mom struggling to hold down two jobs, pay taxes and put food on the table for her kids… her opinion carries more weight than all the tenured academic pricks in the world.

And don’t think that referencing Christian philosopher Who Cares makes you sound intellectual. It makes you sound disconnected from the real world. That single mom struggling to pay taxes to support your library day dreaming doesn’t have time to read academic dribble, because IT DOES NOT MATTER TO THE REAL WORLD. If that makes you suddenly realize how unimportant academia is, good. Time to wake up

No point in anyone commenting here…

Only “enlightened academics” have valid opinions, according to Mish. Everyone else should shut up and pay higher taxes and higher tuition so that we may hear the opinions of quacks that don’t live in the real world.

whats a dynamic factor?