Denial time is over. The eurozone is in recession.

Eurostat reports Eurozone Industrial production Down 0.9 Percent.

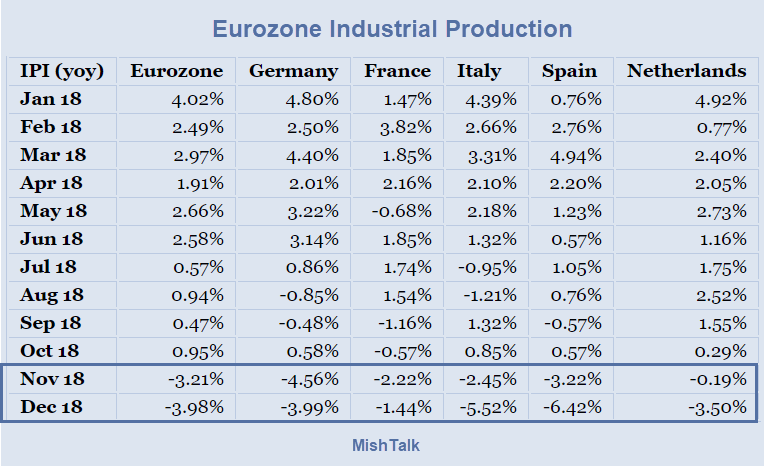

The lead chart is from Eurointelligence which comments:

Eurostat’s industrial production data for December, released yesterday, confirm what we suspected from last week’s poor data from Germany and Spain, which is that the slowdown in eurozone industrial production intensified towards the end of last year. But the Eurostat data tell us more. The slowdown now extends to most countries, including the Netherlands among the largest eurozone member states. Only for the Baltic states and their neighbour Finland, and for Slovakia and Greece, doesn’t the index of industrial production for December 2018 register a drop from a year earlier. The drop in industrial production is most dramatic for Italy and Spain among the larger eurozone member states. Ireland has dismal figures but its series is particularly noisy.

Nobody is yet ready to call it a recession.

While we understand why the ECB is reluctant to call a recession, we’re about ready to come off the fence ourselves. We don’t think we’re over-reacting to a single piece of data if we point out that the slowdown in industrial production is broad-based, sectorally and geographically, and has been going on for a number of months, and that it goes along with a number of other negative data we have been tracking also for months now. It may be early days in 2019, but the eurozone economy essentially peaked in the first quarter of last year. That said, domestic consumption and investment do seem to be holding up – but that will be true until it isn’t.

The slowdown is mostly due to exports, not domestic consumption, and it hasn’t yet filtered down to investment though that cannot be too far off when industrial production is taking a dive. When it does it may be too late, as investment data is somewhat delayed and monetary policy takes some time to take effect. And that is even when the central bank is able to kick-start investment and consumption with a credit supply shock. But currently the ECB’s refinancing rate is at zero and the risk-free rates and bond benchmarks are below zero, anchored to the ECB’s deposit rate of -0.4%. There is ample liquidity in the financial system as a result of the ECB’s asset holdings of over €2tn. And the bank lending survey shows that the supply of credit is unimpeded. There is not a lot monetary policy can do to respond to sagging demand under these conditions.

Key Point

There is not a lot monetary policy can do to respond to sagging demand under these conditions.

Mike “Mish” Shedlock

Europe was too reliant on trade. Dont be shocked if Russia invades a few countries next to regain their Soviet era geography. A failing Europe is what they wanted.

Exports to the UK is the good news as stocking has been ongoing.

When that stops demand will sag further whilst inventories are run down.

I can’t see demand going anywhere but down.

Stimulus can only pull demand forward for a while.

To anyone less aspie in his overemphasized macro focus than Krugman, “stimulus” does a lot more than simply “pull demand forward.” Due to the structure of our financialized “economy,” “stimulus” also alters who makes up that demand.

No longer does demand come from those who run profitable businesses or earn honest wages, and have demonstrably sold enough goods, services and labor; profitably; to posses the means to demand stuff with. Instead, “demand” now comes from reams of incompetent banksters, deadweight “asset owners,” deficit funded governments and others with exactly zero competence at all, in any field extending beyond Applied Capital Destruction.

I just read a piece in the local leftist screecher that four million people in Belgium are on strike for 24 hours, three major unions and government workers in sympathy. Out of a nation of 11 million souls, that’d be the equivalent of over 100 million people here, or two thirds of the workforce. Somebody’s upset.

Wow. That is a hell of a turn from a total Eurozone Industrial Production of +4.02% to -3.08% in less than a year.

An 8% drop in Industrial Production.

“The slowdown is mostly due to exports”….less exports to whom?

Russia (sanctions)? America (trade war)? UK (Brexit)? Etc.

Pretty much back to where it was before the peak silliness of last year.

The ECB is driving a stake through the heart of European industry, with its printing. There’s simply no way to maintain competitive industry, against a backdrop of Weimar levels of debasement theft; from productive industry, to incompetent dilettantes. Even the Germans couldn’t do that, and they’re better at industry than most.

Germany just needs to walk out of the whole disaster right now, and bring its Deutschmark back. Those still aren’t Gold, but at least they historically differed from Mugabe dollars in some respects.

Well said