The NAR reports 5.21 million sales in march at a seasonally-adjusted annualized rate (SAAR).

This follows February’s surge to 5.48 million sales which now appears to be a one-hit wonder. The NAR originally reported 5.51 million in February (up 11.8%) now its 5.48 million (up 11.2%).

More importantly, there was no follow-through.

Nonetheless, NAR Spokesman Lawrence Yun brushed it off as an Expected Slide.

“It is not surprising to see a retreat after a powerful surge in sales in the prior month. Still, current sales activity is underperforming in relation to the strength in the jobs markets. The impact of lower mortgage rates has not yet been fully realized,” said cheerleader Yun.

Please, stop the nonsense.

Economists expected sales of 5.30 million, not 5.21 million.

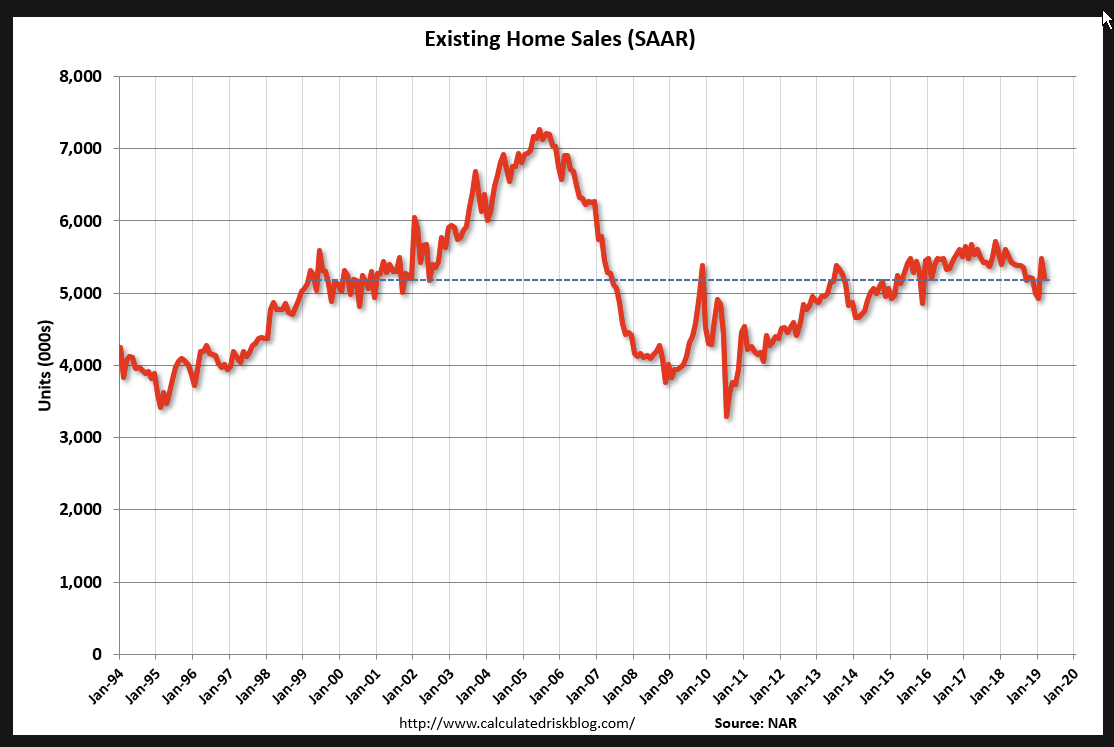

The chart by Calculated Risk (my line in blue added), shows existing home sales are about where they were in January of 2000.

Year-Over-Year Numbers Telling

Year-over-year sales are down 5.4%. In February, sales were down a revised 2.3% year-over-year even with that huge surge.

To brush this off as “expected” is a joke. Neither Yun nor the NAR expected such results.

Rising Inventory

Total housing inventory at the end of March increased to 1.68 million, up from 1.63 million existing homes available for sale in February and a 2.4% increase from 1.64 million a year ago. Unsold inventory is at a 3.9-month supply at the current sales pace, up from 3.6 months in February and up from 3.6 months in March 2018.

“Further increases in inventory are highly desirable to keep home prices in check,” says Yun.

The Econoday cheerleader had this to say: “A key positive in today’s report is strength in selling prices, suggesting that sellers are holding firm to their asking prices. The median rose 3.7 percent in the month to $259,400.”

Supposedly It’s Always a Good Time to Buy

NAR president John Smaby repeated the expected nonsense: “We’re also seeing very favorable mortgage rates, so now would be a great time for those buyers who may have been waiting to make a purchase.”

The median sales price increase more than wipes out any increase in wages or drop in mortgage rate.

Home prices are not affordable. Period. And attitudes towards ownership, debt, and family formation have all changed.

Mike “Mish” Shedlock

Rates have risen since I bought mid-2016, but so have prices. My neighbor’s smaller house just went on the market this weekend for 15% more than I paid. Property taxes are up 10% too. I don’t get why prices haven’t been pressed done more/already given the rise in rates.

Looser lending standards.

Are wages up 15% too?

Only $650k for a 1980s track home in my part of Northern California. Median wage is probably $20 hr or 42k a year. I am sure it’s a great time to buy! House prices go up 10% a year and wages are stagnant! This is so sustainable with such a bright outlook for the future!

Yet, all that the leeches living high off of keeping the rest homeless and desperate needs to do, in order to bring anyone complaining back in line; is to say that “The System”, the system which keeps Californians homeless and starving as a mater of explicit policy, “will collapse,” if anyone dares to do anything at all meaningful about the looting and oppression resulting in $30K houses costing $600K. And then the saps gets all worried about the “system collapsing”, and realize they should be happy that Dear Leader allows them to live in a system where they are the designated homeless.

Those prices actually sound reasonable. My wife just told me yesterday the average home price in Bellevue, WA (where she works) is just shy of $1 million. Not much lower in our city where the lowest price we have seen is just under $900K. But it is a great time to buy!

$30K student debt and $500 car payments leave no room in the budget for a $260K mortgage. $1000 sq ft homes are not being built. I know young professionals who pay $7.50 to Uber to work rather than drive an old used car. These people will never be out of debt and never own a home. Post WWII USA manufacturing monopoly and above world price wages and standard of living cannot return. Compound interest is Jr. Hi math. Unfortunately higher math cannot be taught to a mixed class of sub human cretins with a two week time horizon.

You are blunt but I think you are exactly right. Modern entertainment like the Kardashians, rap music, etc are ruining today’s youth. Good post.

As if the same wasn’t said in the 60’s and 70’s with all “this hippy music and kids smoking the devil’s lettuce”. Those kids back then turned into the Bill Gates, Steve Jobs, etc. Kids today might not live like you think they should, but, in general, they are a helluva lot smarter than I was at their age.

Rates will go lower next year. As we continue to transition to the ownership society more debt slaves will get created. It is all destined to blow up but who knows when. We are likely headed down the path of Japan with small being the in thing.