by Mish

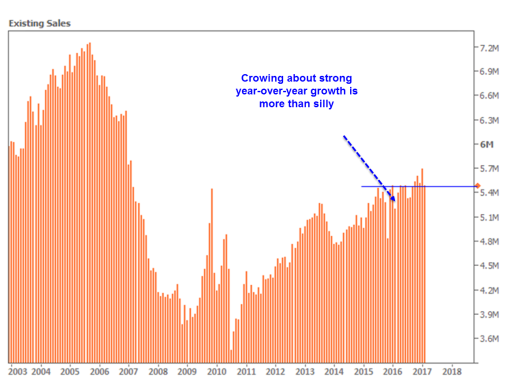

Existing home sales are on the soft side of expectations, down 3.7 percent in February to a 5.480 million annualized rate and below the Econoday consensus for 5.555 million. Details are mostly weak including a 3.0 percent decline in single-family sales to a 4.890 million rate and a sharp 9.2 percent drop for condos to a 590,000 rate. Year-on-year, single-family sales are up 5.8 percent with condos fading and barely over zero at 1.7 percent.

But total year-on-year sales are up a solid 5.4 percent and still below pricing where the median, at $228,400, is up a healthy 7.7 percent. Supply has been very thin but is improving, with 1.750 million resales on the market for a 4.2 percent gain from January. And relative to sales, supply is at 3.8 months vs January’s 3.5 months. Days on the market are very short, at 45 vs 59 days a year ago.

Existing Sales Stifled By Inventory Constraints

Mortgage News Daily reports Existing Sales Stifled By Inventory Constraints.

Existing home sales burst out of the box in January to start the year out with a 3.2 percent increase over the previous month. Those gains, however, were wiped out in February. The National Association of Realtors® (NAR) said on Wednesday that sales of previously owned homes, including single-family structures, townhomes, condos, and co-ops, retreated by 3.7 percent, to a seasonally adjusted annual rate of 5.48 million units. NAR did not revise their original estimate of a 5.69-million-unit pace in January. Even with the decline, sales still maintained their edge over February 2016 by 5.4 percent.

Sales of single-family homes were down by 3.0 percent to an annual rate of 4.89 million from 5.04 million in January, remaining 5.8 percent above the 4.62 million sales pace in February 2016. Condo and co-op apartment sales plunged month-over-month by 9.2 percent to 590,000 units from 650,000 but remained 1.7 percent higher than sales in February 2016.

Lawrence Yun, NAR chief economist, said buyers in most of the country were “stifled” by the lack of properties for sale and weakening affordability. He said, “Realtors are reporting stronger foot traffic from a year ago, but low supply in the affordable price range continues to be the pest that’s pushing up price growth and pressuring the budgets of prospective buyers. Newly listed properties are being snatched up quickly so far this year and leaving behind minimal choices for buyers trying to reach the market.”

Inventory

Total housing inventory increased slightly in February, up 4.2 percent to 1.75 million homes compared to 1.69 million at the end of January, but it is still 6.4 percent lower than in February 2016 and has fallen year-over-year for 21 straight months. Unsold inventory is estimated at a 3.8-month supply at the current sales pace compared to a 3.5-month supply in January.

First-time buyers continue to represent a lower share of sales than their historic levels. Those buyers accounted for 32 percent of sales in February compared to 33 percent in January. First-timers averaged a 35 percent share through most of 2016 and have had a near-40 percent share historically.

Individual investors purchased 17 percent of homes in February, two percentage points more than in January but down from 18 percent a year earlier. Seventy-one percent of investors paid cash for their purchases, tying the most recent high in April 2015. Overall, all cash was employed in 27 percent of all transactions during the month.

Six percent of February sales were foreclosures and 1 percent were short sales. The percentage of distressed sales has remained at 7 percent for three straight months and is down from 10 percent a year earlier. Foreclosures sold for an average discount of 18 percent below market value in February (14 percent in January), while short sales were discounted 17 percent (10 percent in January).

Inventory Not the Problem

Inventory is not the problem. Rather, inventory is one of many symptoms of the problem.

- To a great extent, the Fed re-blew the housing bubble. Banks were bailed out, but not homeowners.

- Prices are up far more than wages. Homes are not affordable, especially for first-time buyers.

- Some of those who may want to move elsewhere are priced out because they cannot get what they need from their existing house, so they pull their listing.

- Those who bought at the market peak in 2005-2006 are still underwater in many places. Such homeowners remain trapped. They cannot sell without bringing money to the table.

The Fed is now hiking, making homes even less affordable.

Lack of inventory represents a price mismatch. New buyers cannot afford to buy, and sellers cannot get the price they want or need. As a result, listings dry up.

Mike “Mish” Shedlock