Case for Decelerating Inflation

In its Quarterly Review and Outlook for the First Quarter of 2021 Lacy Hunt makes a case for decelerating inflation.

Contrary to the conventional wisdom, disinflation is more likely than accelerating inflation. Since prices deflated in the second quarter of 2020, the annual inflation rate will move transitorily higher. Once these base effects are exhausted, cyclical, structural, and monetary considerations suggest that the inflation rate will moderate lower by year end and will undershoot the Fed Reserve’s target of 2%. The inflationary psychosis that has gripped the bond market will fade away in the face of such persistent disinflation.

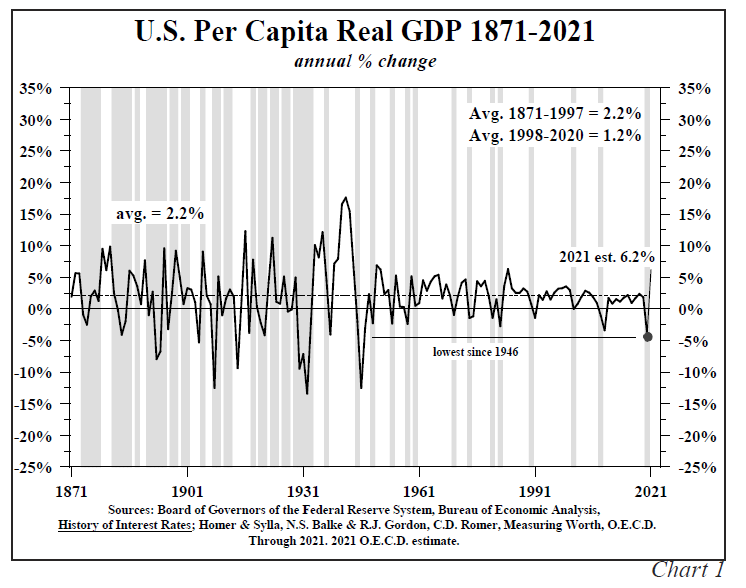

After declining 5.2% in 2020, or the most since World War II, world-wide real per capita GDP is estimated to rise 4.7% in 2021. The United States will perform even better, rising 6.2%, after a contraction of 4.9% in 2020. The U.S. growth rate this year could be the fastest since 1984 and possibly even since 1950 (Chart 1).

Five considerations suggest that such growth is not likely to lead to sustaining inflation.

Lacy said 5. I added a 6th bullet point from his discussion, then added 2 more points of my own.

Six Reasons to Expect Disinflation

- Inflation is a lagging indicator, as classified by the National Bureau of Economic Research. The low in inflation occurred after all of the past four recessions, with an average lag of almost fifteen quarters from the end of the recessions. (Table 1 Inflation Troughs Below)

- Productivity rebounds in recoveries and vigorously so in the aftermath of deep recessions. This pattern in productivity is quite apparent after the deep recessions ending in 1949, 1958 and 1982 (Table 2 Below). Productivity rebounded by an average of 4.8% in the year immediately after the end of these three recessions and unit labor costs were unchanged. The rise in productivity held down unit labor costs.

- Restoration of supply chains will be disinflationary. Supply chains were badly disrupted by the pandemic. Low-cost producers in Asia and elsewhere were unable to deliver as much product into the United States and other relatively higher cost countries. This allowed U.S. producers to gain market share. As immunizations increase, supply chains will be gradually restored. Thus, the pandemic cost the low-cost producers market share which was shifted to domestic producers. The pandemic did far more for domestic firm’s

- Accelerated technological advancement will lower costs. Another restraint on inflation is that the pandemic greatly accelerated the implementation of inventions that were in the pipeline. Necessity is the mother of invention, as has been demonstrated in earlier crisis situations like wars. Thus, the technology du jour is not the same as the technology of a year ago. This will also serve to act as a restraint on inflation. Much of the technology substitutes machines for people, communication without travel, and work without offices.

- Eye popping economic growth numbers, based on GDP in present circumstances, greatly overstate the presumed significance of their result. This is where the fallacy of the broken glass comes into play. Many businesses failed in the recession of 2020, much more so than normal. As survivors and new firms take over their markets, this will be reflected in GDP, but the costs of the failures will not be deducted.

- The two main structural impediments to traditional U.S. and global economic growth are massive debt overhang and deteriorating demographics both having worsened as a consequence of 2020.

Inflation Troughs

Sharp Economic Rebounds

Mish Comments

Lacy is talking about “inflation” as measured by the BLS.

I am in 100% agreement with every point.

Thus I expect bond yields to soon peak if they have not done so already.

Year-Over-Year Inflation Spike Coming

The above viewpoint is not incompatible with my March 12 post Inflation is Poised to Soar, 3% by June is “Almost Certain”

Year-over-year comparisons produce very large numbers, up and down, heading in and out of recessions.

I commented “It’s not that inflation will be rampant. Rather, it’s the impact of year-over-year comparisons, goosed by a huge Covid-related dip in energy prices in April and May of 2020.”

I also commented A Producer Price Index Inflation Spike Is On The Way Too

The rationale is the same. And as noted Gas Prices Are Soaring, I Pay $3.28, How Much Do You Pay?

Hello Fed, Inflation is Rampant and Obvious, Why Can’t You See It?

On March 30, I commented Hello Fed, Inflation is Rampant and Obvious, Why Can’t You See It?

Q: Has my view change?

A: No.

Q: Is it inconsistent?

A: No.

Q: Why?

A: Lacy is talking about “inflation” as measured by the BLS. I addressed home prices in detail substituting home prices in the CPI for Owners’ Equivalent Rent (OER) in the CPI.

I stand by that measure of inflation and it’s out of control.

The Fed blew another set of bubbles and did so on purpose.

Two Bonus Reasons to Expect Lower Inflation

- Bubbles Pop

- Higher Taxes

Lacy came up with six excellent reasons to expect lower inflation. To those we can easily add two more.

Bubbles Pop

The expansion of bubbles is highly inflationary and popping is the reverse.

Please note the Largest Increase in Margin Debt Since 2007 Fuels Stock Market

What happened in 2000 and 2007? I think you know the answer to that question.

Bubbles inevitably pop and the result, by definition, is not inflationary.

Higher Taxes

Tax hikes are hugely disinflationary. Look at where we are headed.

- IMF Joins the Choir Singing the Holistic Praises of Higher Taxes

- Prepare for 3 Things: Big Government, Huge Boondoggles, Massive Taxes

- Biden’s Divide and Conquer Tax Plan Strategy Is Likely to Succeed

- ‘Millionaires Tax’ in NY Likely a Done Deal, Expect a Big Exodus

- A Single Democrat Senator Stands in the Way of a Very Progressive Tax and Spend Agenda

Not all of those tax hikes will pass but some of them will.

Biden wants to increase the corporate tax rate to 28% from 21%. Look for a compromise at 25% or so.

Progressives want huge tax hikes, via reconciliation, some of them will get through.

These tax hikes are very recessionary and disinflationary.

Recovery in Low Paying Jobs

Finally, please note It’s Been One Heck of a Recovery in Low-Paying Zoomer Jobs

That’s not a big inducement to higher inflation either.

Add Things Up

Add it all up and you have 8 reasons to expect inflation will soon peak.

Mish

Thanks for posting the other side of the coin. I like the use of “decelerating” as it still indicates an increase, but at a lower rate.

Predicting the Fed and US Governments actions in the future are key to any accurate prediction of inflation. I can’t see any future where the government doesn’t keep giving out money. If it stops, everything will slow down and the stock market will correct. Even 1M jobs a month does not make up for the stimulus being lost. The 20M jobs lost with the pandemic added up to about $1T in lost GDP. The government borrowed nearly $5T to make up for it. “Eye-popping growth” is based on borrowing money.

We are in uncharted water. so using models of past recessions are going to lack accuracy. For the first time ever we have a significant amount of the population that doesn’t want to work. Also, for the first time ever, we have the government handing out money like there’s no tomorrow to many that need it and many that don’t.

The USG and the Fed have no choice but to inflate their way out of debt. That’s been the path since 2008 – about $1T added to the deficit /yr until 2020 – and then huge injections. Those that think inflation is transitory are not taking into account that there will be significantly more money borrowed and printed in the future.

My guess is that it will pause in the coming months and then when the correction happens, the USG will announce NEW stimulus and UE benefits to pump it back up.

The evidence of inflation, contrary to the conventional wisdom, cannot be conclusively deduced from the monthly changes in the various specialized price indices. The price indices are passive indicators: for the average change; of a group of prices. They do not reveal why prices rise or fall. I.e., inflation targeting depends on how inflation’s defined (which somehow neglects to encompass the vast proportion of all past and present asset-bubbles).

Only price increases generated by demand, irrespective of changes in supply, provide evidence of monetary inflation. There must be an increase in aggregate monetary purchasing power, AD, which can come about only as a consequence of an increase in the volume and/or transactions’ velocity of money.

The volume of domestic money flows must expand sufficiently to push prices up, irrespective of the volume of financial transactions consummated, the exchange value of the U.S. dollar (per the Nattering Naybob: “reflected in FX indices and currency pairs”), and the flow of goods and services into the market economy.

Money and money flows may be net robust, net neutral, or net harmful, depending upon the distributed lag effect of money flows, volume times transaction’s velocity. That saturation point is determined by the rate of inflation, the monetary fulcrum, the lag’s pivot. This is perfectly clear. It is aptly demonstrated by the distributed lag effect of money flows being mathematical constants, for > 100 years.

Inflation will remain high until 2/22.

—Michel de Nostredame

The economy is a hollowed out shadow of it’s former self. Isn’t that deflationary?

I hiked to the Wahweap Hoodoos this morning and got there before sunrise which means I started in the middle of the night.

Just got back to the hotel.

Is that doable on bike? Sounds like the perfect distance

Define middle of the night. lol.

I left the hotel at 3:00AM

DiMartino Booth interviewed Richard Werner recently with a different take.

Saying rates follow growth not the opposite. Inflation occurs when consumption is targeted. So he thinks inflation continues. My question

Is why is the profession of economics has so many various opinions as banking has been around for 5000 yrs?

And not Whatever because when the Fed gets it wrong and blows bubbles they are Squeezing the young adults. Debt slaves for life living in a world where we keep alive zombie companies and dinosaurs and crush the innovation .

Even Germany has more Hidden Champions than us, That’s why they’re productivity is higher as is they’re growth.

So let’s Think about the economy we want to live in and work towards productivity and innovation not stimmy makes market go up. The casino is not the economy and does not make the world a better place to live. Look at Japan with something like 30 different programs after 1990 to fix their economy and all failed. Ppl better get Woke or your kids will live in a dump working for WMT or Amazon.

well done but I believe the China story will make this discussion wrong—China shifting to a domestic consumption based dynamic with a rising YUAN will signal that China will not be the disinflationary forced upon the world after the 50% devaluation of the YUAN January 1,1994 unleashing the power of 1 billion workers to suppress global wages.China has been using the recent YUAN strength to stockpile raw materials—enhancing middle -class wealth through a stronger currency driving all prices higher

Mish, With a read-

Time to look to increase exposure to defense, gold and tge miners?

“A further consideration is that the current stockbuilding cycle could be shorter than average. The covid shock appears to have extended the previous cycle to 4.25 years. If the current cycle were to display an offsetting deviation from the average 3.5 years, the next low would occur in early rather than late 2023 (i.e. 2.75 years from the Q2 2020 trough). This, in turn, would imply that the 18-month negative period for markets ahead of the low would start in H2 2021.”

These tax hikes are very recessionary and disinflationary.

Not really. The average tax paid in most brackets stayed the same as the Obama administration. The only thing that changed is some loopholes got closed while others opened. We are the above 400k household and it was a big fat zero difference on our taxes between Trump and Obama. The same will be true under Biden. The disposable income bracket (from 200k and above per household) drives 80% of consumer spending, pays most of the taxes and is the engine of the economy. Aside from the Covid blip there hasn’t been a recession felt in the part of the economy that drives the bus and fills the gas that is the American economy. It will be more of the same this decade as the 2010s.

Inflation peaking is not the story. It will settle back to higher than average because of financialization of assets. We have more derivatives driving commodity prices because of cheap money. Don’t expect housing prices to fall anywhere because of availability of money for qualified borrowers. Globalization is going to come back in a big way. I expect the Fed to unexpectedly raise interest rates once they realize they acted late. They will wait until the job market improves further. We muddle our way through another decade. Nothing to see here folks move along.

there is something to see here, and actually participate in. s&p500 is likely to double before we see the next 20% drop. my guess is that it gets to 8000 in 5 years or less.

They’re looking very seriously at how to tax wealth at the moment, presumably because they realise they can’t continue to issue dollars at the same rate. If you’re right about these stock market rises and the widening wealth gap they’d be calls to tax unrealised stock market profits. Only a little bit at first of course.

it’s all kabuki theater.

Many a billionaire will be made, and we will possible see the first trillionaire in the next 5 years.

Forbes will stop publishing a billionaires list, and instead require a minimum of $100B to be listed — the centi-billionaire list.

For every 2x move in stock market price, the .1%-ers wealth will go up 10x.

Inflation is already here and going through the roof 🙄

Inflation is already here and going through the roof 🙄

Exactly.

lacy hunt has no idea what powell and yellen are about to do next.

Investors have put more money into stocks in the last 5 months than the previous 12 years combined

Corp profits have been flat for last 9 years. Buybacks and financial engineering goose prices higher. Fed backstops everything . Growth is dismal and zombie corps prevail. Great we make some money but at the expensive of the future generations.

I call BS

I read in an article somebody had been visiting the US and said there were “Wanted” signs everywhere for extra staff. Maybe he just saw a few and leaped to conclusions.

Nothing says inflation like wage inflation.

It’s hard to get someone to come work for $12/hr when they are getting $15 on benefits.

My son hired a new person (again) and he is dreading tomorrow because he has to train this person. They all want to come to work and F around with their cell phone all day. It’s what happens in the job market way too often.

You know what’s different about the previous recession recoveries and this one? $5T in stimulus payments. 2009 was around $800B.

OT…Tesla CFO buys house in my neighborhood. This is on my jogging route, just across the freeway.

Got to change that bridge. Need something snazzy.

That is a historic railroad trestle sir. 🙂 One of the oldest bridges in the state, built in 1912….there is a very, very snazzy pedestrian bridge just downstream, btw.

That one is cool!

You can use the old one for cross-tie walking.

Bats love that railroad trestle as they do the road/pedestrian bridge. Went on the river tour back in 2017.

Seems the elephant in the room is China and a lot of what happens China dependent

The economy seems to be accelerating. We see it in freight traffic and pulp pricing ( boxes tissues etc). Likely this is transitory

What a great addendum to the Hoisington letter that is always thoughtful and full of insightful historical context. The over-hyped inflation consensus is creating a nice opportunity to position the portfolio for the disinflationary dynamics that will hit in the second half of the year.

Whatever.

For us:

You drink imported wine?

Un-American.

You only drive 2000 miles a year?

Hell, that’s un-American too. In a slow year, I drive 10X that….even though I no longer drive out to the farm every day.

1. We live in the Socialist Paradise of the City & County of Denver..

2. We are retired.

3. Our grandchildren live 8.2 miles away.

4. We prefer the more acidic styles of European wines. My current favorite is Lagrein.

5. We walk to the butcher, seafood shop, cheesemonger, bakery, chocolatier, and 3 grocery stores.

6. We have 5 breweries within 6 blocks of our house.

We’ve visited Denver a few times, and it’s a genuinely gorgeous part of the country. The home prices there, though, are astronomical!

Sounds nice, actually. Socialist paradise with cannabis indica gummy bears….what’s not to love.

My wife and I work and live less than a mile from work. I use to drive like you when I lived in Texas and it sucked. Most of our miles are for the actual purpose of coastal vacations, which are less than 250 miles away. I’m more like@davebarnes2 but not retired. We too prefer European wines.

I was kidding above…..I’m not opposed to French or Italian wines…..but I think California wines are excellent, for the most part.

I’ve cut my carbon footprint a lot over the last decade. I used to drive a lot more. I just read that Chevy is coming out with an all-electric Silverado pick-up with a 400 mile range. I plan to be an early adopter.

Good arguments. But I can’t help being skeptical here.

Too many providers of services, too many businesses in food service and hospitality, won’t be able to keep from raising prices to compensate for lost income that isn’t coming back. Some of them will still fail, of course, but the ones who make it will be the ones who can raise prices and get away with it….whatever the reason might be.

This is a Mom & Pop POV, from here on Main Street. I have no idea about corporations and the typical consumer goods…..although food and energy look to go up to me. I promise you the cost of dental treatment is going to jump substantially. It has to….. because the rules are different, and the cost equation is different than it was before.

Rents will go up in markets like mine. Not that that matters in CPI inflation, of course.