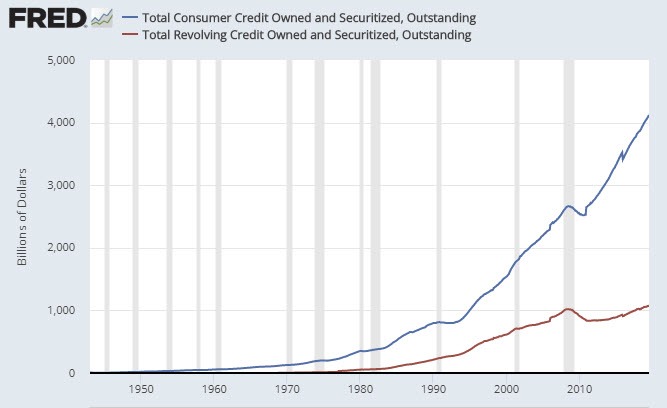

The Fed’s Consumer Credit Report shows consumer went on another credit card binge in July.

Econoday economists expected a boost of $16.1 billion in a range of $15.2 billion to $17.0 billion.

Credit jumped $23.3 billion.

High Debt Levels Are Weighing on Economies

The Wall Street Journal reports High Debt Levels Are Weighing on Economies.

Debt owed by governments, businesses and households around the globe is up nearly 50% since before the financial crisis to $246.6 trillion at the beginning of March, according to the Institute of International Finance, an association of global financial firms.

The borrowing helped pull economies out of the nasty recession, but left them with high debt burdens that make it harder for policy makers to raise rates. It also makes consumers and businesses more likely to pull back from spending money on new goods if economic conditions weaken.

“Globally, you are at worryingly high levels,” said Sonja Gibbs, managing director for global policy initiatives at the IIF.

In the U.K., Canada and Australia, central bankers have backtracked from rate increases in the past two years after consumers got bruised more than expected. U.S. consumers, who have borrowed to pay for college, cars and everyday spending, have been less affected because their debt burdens are much lower relative to their incomes.

“The world is in a delicate equilibrium,” said Mark Carney, governor of the Bank of England, in a February speech. “The sustainability of debt burdens depends on interest rates remaining low and global trade remaining open.”

Global Debt by Sector

Central banks new lower rates to keep the debt bubble growing.

Delicate Equilibrium?

The world is in a delicate equilibrium,” said Mark Carney, governor of the Bank of England.

Equilibrium Definition: A state in which opposing forces or influences are balanced.

Families Go Deep in Debt to Stay in the Middle Class

Here is an article from last month whose headline I thought to be very peculiar: Families Go Deep in Debt to Stay in the Middle Class.

The American middle class is falling deeper into debt to maintain a middle-class lifestyle.

Cars, college, houses and medical care have become steadily more costly, but incomes have been largely stagnant for two decades, despite a recent uptick. Filling the gap between earning and spending is an explosion of finance into nearly every corner of the consumer economy.

Consumer debt, not counting mortgages, has climbed to $4 trillion—higher than it has ever been even after adjusting for inflation. Mortgage debt slid after the financial crisis a decade ago but is rebounding.

Student debt totaled about $1.5 trillion last year, exceeding all other forms of consumer debt except mortgages.

Auto debt is up nearly 40% adjusting for inflation in the last decade to $1.3 trillion. And the average loan for new cars is up an inflation-adjusted 11% in a decade, to $32,187, according to an analysis of data from credit-reporting firm Experian.

Unsecured personal loans are back in vogue, the result of competition between technology-savvy lenders and big banks for borrowers and loan volume.

Late Stage Credit Bubble

Ability to buy things one cannot really afford does not make or keep someone in the “middle class”.

Those living beyond their means are not in the class they pretend to be.

There is no “equilibrium” here. Wages are not keeping up with needs and desires.

Rather, these reports show a late stage credit bubble the Fed desperately wants to keep inflating.

Mike “Mish” Shedlock

Yes, it really is. I read an article by one journalist link to marketplace.whmcs.com about the economic situation in the country. Indeed, the elements of the crisis are becoming apparent now that the debt pile is huge. We have to not only work harder but also look for second or even third job. Besides my main job, I work part-time.

Such pessimism…..the fact remains that there no real uptick in delinquencies . In fact, they are trending at historical lows. Further, historically low interest rates have helped consumers to manage debt and this is likely to be further the case as the Fed continues to lower rates complying with market wishes for yet-lower borrowing costs. So nothing really to see here yet….move on!!!

This is because everything is made abroad in China and similar place. The people here are not given a chance to earn a living, but are expected to buy things produced overseas. So, the difference between what they earn and what they are expected to purchase is filled with debt. Here’s how it works: US companies hire Chinese to make things; the $1 to 6/7 yuan exchange rate makes the things cheap (this is currency manipulation pure and simple abetted by one US administration by another); the US consumers borrow from the US bankers, and the companies sell them the things for as much as the consumers could pay. The shareholders pocket the difference between what they paid Chinese and what they sold to the US consumer (that’s their profit), and bankers pocket the interest and both become richer, the consumers become poorer and deeper in debt, the Chinese get US$ and our intellectual property.

This is why as Mish writes: “Most of the net worth is all in the top 10-20% The Debt is the 50% or lower. Something like 30% of the people have negative net worth.”

Add to that we lose industry. Chinese, Vietnamese and all sorts of other communists and totalitarian get our cash and technology.

When people claim the high moral ground and tell the American ‘middle class’ to live within their means, my feeling is that these people may be really mistaken. The wealth of American wealthy is the debt of American poor. When the middle class stops borrowing say good bye to the stock market, US dollar (it would be worthless), your offshore accounts, your beautiful mansion and carefree life. The middle class will get wiped, but everyone else will also be affected. And which way that reset will go, no one can predict or control for sure.

How the so-called ‘free traders’ can’t see this in plain sight is totally flabbergasting…

…. Mish writes interesting stuff indeed ….sometimes though he doesn t make sense, like opposing tariffs on Chinese products for example…

The reason why the “flat yield curve” doesn’t mean anything this time is because lending doesn’t happen at some spread above Treasuries anymore. Auto makers issue loans to consumers at below Treasury rates (at least for a period) as a buyer incentive — while credit card rates are well into double digits. Neither auto incentive loans nor credit card loans are tied to Treasury rates — ergo an inverted yield curve doesn’t mean as much as it once did. That is in addition to Fed manipulation, which makes Treasury rates almost meaningless.

The fact that most consumer’s income is growing slower than debt, and debt levels are already well above historical percentage of net worth — that is the reason the alleged Bernanke / Obama recovery was so anemic. Income growth is being diverted from growth to debt service, while quasi-socialists attack and destroy the tax base needed to support their spending fantasies.

A lot of defaults are coming, and not just on traditional debts. Politicians and bureaucrats think their pensions are money good, but taxpayers don’t get a pension after 40 years much less after 20.

Interest rates, and credit as such, are becoming progressively unhinged from economic reality. Negative rates alone prove this.

Keith Weiner has a theory that because dollars are IOU’s backed by Treasuries, and Treasuries (and every other currency in the world) are IOU’s based on dollars, the whole thing is a closed, fantastical system that leads to capital and wealth destruction exactly while speculators believe they are “investors” who are building wealth. The system is closed in the sense that one cannot escape from holding anything other than IOU’s, i.e. credit.

If one could escape to gold, which isn’t an IOU, interest would be objectively based on the credit risk over gold. But gold is impractical today qua money, and has been relegated to just another tool for speculation in IOU’s. Especially, ironically, among gold bugs.

IOU’s backed by other IOU’s.

Its robbing Peter to pay Paul, while also robbing Paul to pay Peter

link to phrases.org.uk

(not sure if that is the best link, it just happened to appear first on the search I just did)

Why Are America’s Three Biggest Metros Shrinking?

After a post-recession boomlet, the New York, Los Angeles, and Chicago areas are all seeing their population decline. link to theatlantic.com

New York is in decline because of Bloomberg, Deblasio and Cuomo — who collectively gave birth to AOC.

Many left wingers want big big big government, so they voted accordingly. Those same left wingers freaked out when they got the bill for the government they wanted.

Chicago failed because of Daley and Rahm.

All of California is failing, its not just LA. California is a left wing cult with zero tolerance for anything even moderate.

Not saying the right wingers are perfect (they are not), its just that concentrations at the moment happen to be extremist left wing.

Extremist anything is a problem

The top 20% in income have 53% of the CC debt, the bottom 20% only 5%. That does make the debt/income ratio about 3 times higher at the bottom than the top but in raw dollars the top quin-tile carries the bulk.

“Total net worth is more than keeping up.”

Totally Misleading Picture.

Most of the net worth is all in the top 10-20%

The Debt is the 50% or lower.

Something like 30% of the people have negative net worth.

Total net worth is more than keeping up. link to static.financialsense.com

How much of this is based on today’s bloated equities and real estate prices.

Most of it I would guess. “bloated” is an opinion though.

Driven entirely by soaring prices,soaring costs and a permanently collapsed economy,decade long depression where the only growth is coming entirely from big govt,taxing,borrowing ,printing cash like grows on trees,devaluing the currency forcing prices to the moon.Stopped at Lowes ,picked up a handful of nuts and bolts,after taxes $30 for a couple of bolts!!!That says it all!

The rollercoaster is going higher yet until a crash of epic proportions. Last time around people figured out that you can run up the credit cards and then declare bankruptcy and come out clean in years and keep the stuff you bought. Credit is not money but it can buy you stuff for longer than you think. We don’t live in business cycles but in credit cycles (Peter Boockvar quote). How long this credit cycle can go on is anyone’s guess but the over/under is 18 months imo.

The CEOs of the largest banks in Europe, starting with UBS but including all the big EU banks, stated at a recent industry conference that negative interest rates are counter-productive and must be stopped.

This isn’t much of a revelation to the average person. But it is interesting that the political elite is openly telling the ECB that enough is enough. Negative rates will stop or the economy will grind to a halt.

The false miracle of not-modern monetary theory is collapsing. Debt growth is not the same as economic growth. These “temporary” extraordinary monetary conditions have been going on for over a decade already. If they haven’t worked for 30 years in Japan, they are not going to work

And its high time the political class figure this out. it is insulting to anyone who does their own grocery shopping to claim the Fed or ECB or BoJ are staffed by “experts” or even of average competence.

The bubble popping emergency is over. Its long over. Rates needed to be normalized years ago. Its absolutely stupid to suggest rates can go lower from here without causing significant damage.

Wait until Washington DC, Brussels and Tokyo have to live within their means. Living within your means is NOT austerity, no matter how many stupid central bankers say otherwise. Yep, this means the debt induced false growth of the past 20-30 years won’t continue. Good riddance

And yet they continue to lie about CPI and the good little sheep mindless believe without objection. I just wonder when people realize this is a fraud perpetrated by the govt and its fed minions. This is why people are migrating to socialism. The middle class lifestyle is being eroded by inflation and people can’t figure out why they are drowing while trying to tread water.

people who support socialism are stupid. The track record of socialism is 100% failure, in every culture, every time period. Its a proven failure.

Academics have brain washed students into thinking socialism might work, but these academics can’t hack the real world which is why they escape to perpetual campus life…. they don’t want to grow up

There won’t be any austerity. The interest rate on the debt won’t matter because the central banks will own as much sovereign debt as is needed to keep things moving forward.

There hasn’t been any austerity yet. Living within your means is not austerity, its life.

Zimbabwe’s central bank has been buying all of Zimbabwe’s “debt” for decades. It worked, in the sense the bonds got sold. But is Zimbabwe a major economy?

If the G7 acts like Zimbabwe, it will have Zimbabwe-like economies. Garbage in, garbage out.

What could possibly go wrong?

“And the average loan for new cars is up an inflation-adjusted 11% in a decade, to $32,187.”

I remember in 2006, housing prices exploding in my little burg in Florida. I kept thinking “where are all of these rich people coming from?”. I mean really, how can thousands of people in my area afford $350k for a stupid house? Well, we found out that those people didn’t really exist.

I am going on record and saying that the average person can’t afford a $32,187 car either. And I expect we’ll find that out pretty soon.

The average person can’t. The average person with a real income can. Loan terms are now up to 76 months for new cars. I expect once rates are cut and car dealers get desperate we will see 100 months and looser credit for “well-qualified” applications. That will only be people who don’t have much debt.

6 yrs 4 months? Seems like an odd term.

Buick has 75 months. Most deliquint car loans are 72 to 84 month loans. I think the odd periods are due to “no payment until 2020”

Being someone that lives rural and seeing these 350k sheetrock masterpiece developements spring up all over, including across the street(15 miles from town) I pray everyday this bubble blows. This expansion is insane. Worst yet are the people moving out here to get away and then trying to turn the countryside into what they were trying to escape. Pristine lawns, hoa’s, mercedes on gravel roads,etc

35mph gravel

“Rather, these reports show a late stage credit bubble the Fed desperately wants to keep inflating.”

…

Yes. And why it is hard to guess the demise of current “recovery”. Just when you think the insanity can’t go on much longer … something comes to the rescue. Like Fair Isaac making credit score easier.

“Consumers with less-than-stellar or borderline credit scores may soon have a new option to help them qualify for loans and credit cards.”

Bottom line: Debt quality at end of expansion (like 2006 and 2007) very poor and susceptible to blowing everything up. But borrowers don’t care. Remembering slap on the wrist penalty last go round, borrowers will continue to lever up.

Why walk away from $10K when you can walk away from $20K?