Please consider Commercial Banks under Persistent Negative Rates by the Federal Reserve Bank of San Francisco.

Do extended periods of negative policy interest rates continue to encourage commercial bank lending? A large panel of European and Japanese banks provides evidence on the impact of negative rates over different lengths of time.

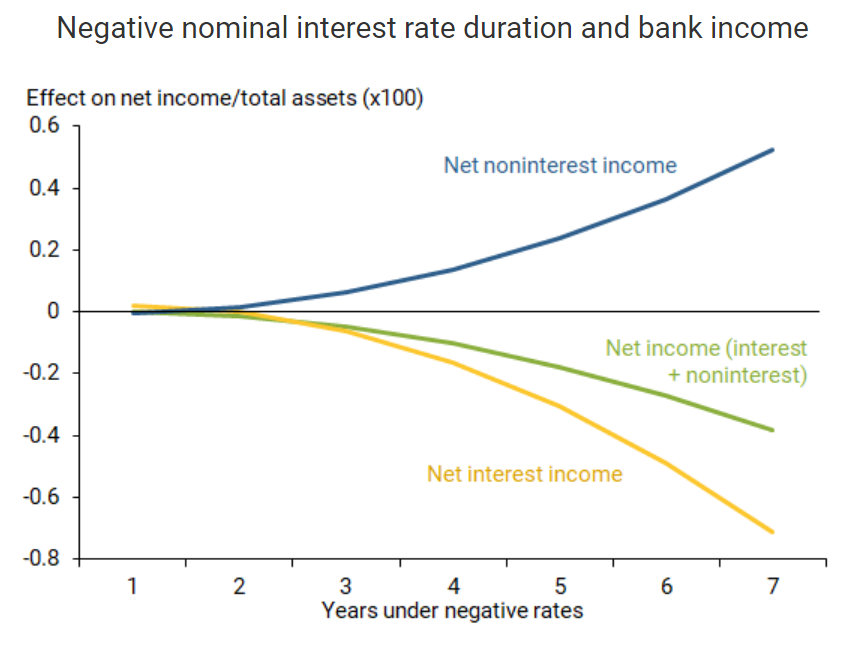

Analysis suggests that both bank profitability and bank lending activity erode more the longer such negative policy rates continue, primarily due to banks’ reluctance to pass negative rates along to retail depositors. This appears to negate one of the main arguments for moving policy rates below the zero bound.

Our results suggest that banks can only mitigate losses on interest income through charging fees on deposits and enjoying capital gains on securities holdings for short periods of negative interest rates. As durations of negative policy rates lengthen, the gains from these adjustments become increasingly inadequate to offset the growing losses on interest income due to banks’ limited abilities to pass along negative rates to depositors. The result is that, as negative rates persist, they drag on bank profitability even more.

The data clearly show that losses on interest income accelerate over time and begin to outweigh the gains from noninterest income. As a result, the impact on overall profitability falls below zero. Our regression analysis for the impact on overall bank profitability becomes negative on average with statistical significance after five years under negative interest rates.

No Surprise

I talked about this six years ago when the ECB first went to negative rates.

Statements I made then still apply,

- The Fed paid interest on excess reserves slowly recapitalizing banks over time.

- The ECB charged interest on excess reserves draining already stressed banks of capital.

I question the study’s statement “the impact on overall bank profitability becomes negative on average with statistical significance after five years under negative interest rates.”

Indeed, their own chart shows negative impacts after a year.

Impact of Negative Policy

Lose-Lose Setup

In short bank lending suffers after one year and profitability suffers at increasing rates over time.

It is for this reason I have often stated the Fed would not be stupid enough to opt for negative rates.

The effective lower bound is at least somewhat above zero.

Effective Lower Bound

Please see my September 25, 2019 post In Search of the Effective Lower Bound

The Fed is no longer talking about zero-bound but effective lower bound. What’s the difference? Where is it?

Effective Lower Bound is the point beyond which further monetary policy in the same direction is counterproductive.

I propose the Bank of Japan and the ECB are already below ELB. I further propose the ELB can never be negative but it can be well above zero.

Negative interest rate policy can never work as it violates basic economic principles on time preference and the time value of money.

Moreover, a dive below the ELB supports the position I presented on September 23, 2019: Negative Interest Rates Are Social Political Poison

Deeper Down the Rabbit Hole

Yesterday, I noted Draghi Open to MMT and a People’s QE

Every attempt to fix the perceived problem of “too low inflation” goes deeper and deeper down the rabbit hole.

It’s economic madness, yet, here we are.

It took a multi-year study for the San Francisco Fed to come to the right conclusion.

That’s a step in the right direction. Many of these studies come to the wrong conclusion.

The solution is to let the free market set interest rates rather than a tail-chasing consortium of economic wizards who have never spotted a bubble or a recession in real time.

Mish

The whole notion of making money off money that is free to create is silly. Governments and central banks should just do away with so-called private banks and stop pretending the whole system isn’t backed by the government.

I think we are already heading into that direction. Bank balance sheets are getting impaired so they can lend less. The central banks pick up the slack. We are gradually moving from credit money to fiat money so private banks become redundant.

In a few years everybody has a direct account at the central bank, which will then charge deeply negative rates if they want to. Or not. It won’t matter if everything has become fiat.

Just goes to show how smart American financiers actually are. Where else in the world is there to invest? No where except the USA. Evan China can’t derail that as Mish has pointed out.

I think the only real market to invest in, ironically, is Russia. Low PE ratios, high dividends, and low debt

Elliott Wave International has done studies showing central banks (not just the FED) FOLLOW the markets. Markets are already setting the rates. No amount of central bank interest rate targeting is going to work.

The fact that so many corporations have been borrowing at negative real rates just to buy back their own stock (which does nothing for the economy) already tells you that the price of credit is definitely not a constraint. And the increased leverage makes the company more vulnerable to economic shocks.

On the other hand, negative real rates is a real loss to many savers and pensioners, who have been forced to reduce their spending because of it. I for one have massively reduced my spending because of this. And many will have to save much more if they ever want to retire.

Consider this: in 2020, £100k at age 65 now buys you an annuity that pays £2900 annually for the rest of your life (indexed). In 2007 this was more than £6200. In other words, you have to save more than twice as much for your retirement or cut your lifestyle in half.

Many people are still in denial about this, but when people will become more aware of this or are suddenly confronted with reality, it is going to be a massive drag on consumer spending.

A negative yield curve, an excess of savings over real investment outlets (and associated mal-investment), stems from the fact that adding infinite money products (QE-Forever), decreases the real-rate of interest and has a negative economic multiplier.

Whereas the activation and discharge of monetary savings, $15 trillion in commercial bank-held savings (income not spent), of finite savings products (near money substitutes), increases the real-rate of interest, produces higher and firmer nominal rates, and has a positive economic multiplier.

Monetary savings (funds held beyond the income period in which received), flowing through the nonbanks decreases the bank deposits owed to the public and indirect investment increases those deposits owed to the nonbanks, NBFIs. Thus, there immediately becomes an increase in the supply of loan funds – but no increase in the money stock (a velocity relationship). Loan funds will essentially go up dollar for dollar.

But thus far, the banks have experienced no change in their total deposits, their total reserves, so their lending power remains unchanged.

Other things are not equal. Because the nonbanks have an increase in the supply of loan funds and the nonbanks expeditiously activate savings, spending will be stimulated. The banks will then be forced by by the FED to restrict commercial bank credit. That’s what raises the real rate of interest.

Thus, the prosperity (and bankable opportunities), of the DFIs is dependent upon the prosperity of the NBFIs. It is much more desirable to promote prosperity by inducing a smooth and continuous flow of monetary savings into real investment, than to rely, as we have done c. 1965 (after 5 successive rate hikes in Reg. Q ceilings for the commercial bankers exclusively), on a vast expansion of Reserve and commercial bank credit with accompanying inflation to stimulate production (i.e., stagflation).

Should I be glad that their biggest concern is bank profitability and not the effects on individuals?

Welcome to the Thunderdome!! If we have to impoverish the risk-averse to keep capital asset prices inflated so be it. We’ve been doing it for 40 years, why stop now.

I don’t think the Fed can get way with negative rates here unless we go cashless. At that point it gets much easier from a coercion standpoint. I always figured they’d get trapped into it eventually. I hope you’re right.

I still see the low rates as an opportunity to borrow long with rates locked for 30 years. It seems like the best kind of liability you’re ever likely to find…..if you can use it to buy a high quality asset at something like a reasonable value. That’s the hard part now, finding value.

Negative interest rates are not implemented because they work. They are implemented because they are the only option in certain situations. In Europe the banks were sacrificed to protect the PIGS. They needed cheap infusions just to keep the project together.

I fully expect the Fed to eventually implement negative rates if they can’t get inflation to jump. You can stealth bail out the banks but bailing out companies it less politically supported.

I wonder why the banks put up with negative rates as they do nothing for their profitability. Why don’t they protest by limiting deposits. That would cause a few problems and make CB’s think twice. Maybe they’re not allowed to.

Because your don’t bite the hand that feeds you. The fed could cut them off from FDIC or I would imagine 11 dozen other ways to punish a bad child.

What we have at this point isn’t capitalism.

“I wonder why the banks put up with negative rates as they do nothing for their profitability. Why don’t they protest by limiting deposits. That would cause a few problems and make CB’s think twice. Maybe they’re not allowed to.”

I see it as a compromise, they know that if there is a strong deflation their own values will also be ruined and they will mostly all fail. So they work with CB and its mandate, negative rates are best reflected in sovereign debt which equates to allowing increased government spending and so inflation. I don’t think the US will go negative, it would use other methods because negative rates clash strongly with bank independence, but who knows. In europe it was and is a political endeavour between various nations – germany gets negative borrowing costs and continued southern demand, the south gets bailed out of depression, all while banks merge and take each other over in a controlled fashion behind closed doors … however the net imbalance just increases (target 2), as well as recovery being feeble, propped up, and not organic.

Yes it was a daft thought after more reflection 🙂 They have to pass on the costs eventually then.

Yeah I figured as much.

I just don’t know that there is an end to the insanity. Negative interest rates don’t work long term but short term if you go deep enough they will work. Imagine -5% corporate credit refinance facility Who needs earning when you have the fed making money for you.

With debt at GDP climbing at its current rate across the world and the world economy headed in the wrong direction I don’t think anything is off limits anymore. Inflation of course is the goal but it might just be extremely one sided inflation this time. Goods cost could skyrocket while asset prices collapse. Helicopter money in route.

I personally don’t think the US will follow Europe to negative rates because of the potential affect on the USD. The current account deficit is already growing & likely to get worse. However I can’t weigh that up in my mind against the offshore demand for euro dollars that supposedly creates an endless demand for dollars. There must be a point at which a deteriorating current account deficit would offset such offshore demand for dollars.

A world reserve currency requires a current account deficit.

It is called the Triffin Dilemma. Used to be based largely on mideast oils sales. Now based largely on offshored US production. Great way to export all the dollars we create just to keep the US functioning. Works (for now) because the cheaper imported goods mask inflation. Most of the dollars that make it back go into real estate or government bonds.

Many thanks, I didn’t know it had a name. I understand a World Reserve Currency requires a deficit, but how big a deficit, and at what rate does it need to grow? The Triffin Dilemma explains why the dollar is over valued versus the deficit, but presumably the degree to which it is over valued varies as the deficit fluctuates. In which case periods of excessive growth in the deficit should cause dollar weakness, if only temporarily? Anyway, I don’t expect you to know, 🙂 I’m just pondering out loud.