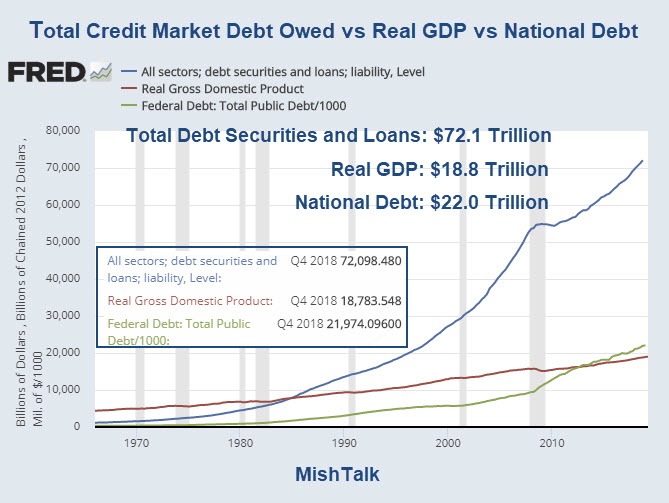

Key Debt Points

- In 1984 it took $1 of additional debt to create an additional $1 of Real GDP.

- As of the fourth quarter of 2018, it took $3.8 dollars to create $1 of real GDP.

- As of 2013, it took more than a dollar of public debt to create a dollar of GDP.

- If interest rates were 3.0%, interest on total credit market debt would be a whopping $2.16 trillion per year. That approximately 11.5% of real GDP year in and year out.

Total Credit Market Debt Detail

Tiny Credit Drawdown, Massive Economic Damage

Note the massive amount of economic damage caused by a tiny drawdown in credit during the Great Recession

Q. Why?

A. Leverage.

The Fed halted the Great Recession implosion by suspending mark-to-market accounting.

What will it do for an encore?

Choking on Debt

The Fed desperately needs to force more debt into the system, but the system is choking on debt.

That’s the message from the bond market.

One look at the above charts should be enough to convince nearly everyone the current model is not close to sustainable.

Here’s another.

Housing Bubble Reblown

How the heck are millennials (or anyone who doesn’t have a home) supposed to afford a home?

Despite the fact that Existing Homes Prices Up 88th Month, the NAR Can’t Figure Out Why Sales Are Down.

Negative Yield Ponzi Scheme

Note that Negative Yield Debt Hits Record $15 Trillion, Up $1 Trillion in 2 Business Days.

So far, all of this negative-yielding debt is outside the US.

Why?

- The ECB made a huge fundamental mistake. Whereas the the Fed bailed out US banks by paying interest on excess reserves, the ECB contributed to the demise of European banks, especially Italian banks and Deutsche by charging them interest on excess reserves that it forced into the system.

- The demographics in Europe and Japan are worse than the US.

Tipping Point

We are very close to the tipping point where the Fed can no longer force any more debt into the system. That’s the clear message from the bond market.

Currency Wars

Meanwhile, major currency wars are in play.

Under orders from Trump, US Treasury Declares China a Currency Manipulator.

Hello Treasury Bears

For decades, bond bears have been predicting massive inflation.

Once again, I caution Hello Treasury Bears: 10-Year Bond Yield Approaching Record Low Yield.

Fed Misunderstands Inflation

The Fed remains on a foolish mission to achieve 2% inflation.

In reality, the Fed produced massive inflation but does not know how to measure it.

Inflation is readily see in junk bond prices, home prices, equity prices, and credit expansion.

Note that small credit contraction in 2008-2010. Recall the ‘Great Recession” damage that accompanied it.

I do not expect a repeat on that scale, all at once. But I do expect a prolonged period of credit stagnation as retiring boomers start to worry about their retirement. All it will take to set the wheels in motion is a prolonged downturn in the equity markets.

Economic Challenge to Keynesians

Of all the widely believed but patently false economic beliefs is the absurd notion that falling consumer prices are bad for the economy and something must be done about them.

My Challenge to Keynesians “Prove Rising Prices Provide an Overall Economic Benefit” has gone unanswered.

BIS Deflation Study

The BIS did a historical study and found routine deflation was not any problem at all.

“Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive,” stated the BIS study.

It’s asset bubble deflation that is damaging. When asset bubbles burst, debt deflation results.

Deflationary Outcome

The existing bubbles ensure another deflationary outcome.

So prepare for another round of debt deflation, possibly accompanied by a lower CPI especially if one accurately includes home prices instead of rents in the CPI calculation.

Central banks’ seriously misguided attempts to defeat routine consumer price deflation is what fuels the destructive asset bubbles that eventually collapse.

For a discussion of the BIS study, please see Historical Perspective on CPI Deflations: How Damaging are They?

Message from Gold

Please pay attention to gold. As Gold Blasts Through $1500, the Message is Central Banks Out of Control, Not Inflation

Inflation is, or will soon be, in the rear-view mirror. Another deflationary credit bubble bust is at hand.

Mike “Mish” Shedlock.

You compare debt in nominal $’s against GDP in inflation adjusted $’s. Meaningless.

Yes, Mish says: “The Fed halted the Great Recession implosion by suspending mark-to-market accounting” – and somewhere in my notes I have read that until 2011? or 2012 technically the entire FDIC insured US banking system was insolvent, if you had used mark-to-market accounting.

The Fed has become the great enabler. A key role of a reserve currency is to force other currencies to toe the line or pay a stiff price. Ignoring this economic reality translates into pain for those holding the currency of any country that abuses this economic law.

The rapid expansion of debt and credit during the last decade could have occurred without the Fed being totally complicit and in agreement. It has been the Fed that decided to allow the dollar to be used as a global prop.

Trump’s desire to manipulate the dollar lower to boost exports would take the world down a very slippery slope. The article below explores the problems it could cause.

Nicely done. Finally a clear and relatively simple explanation for the disasters facing us. First, whether in housing, cars, vegetables or packaged goods, the idea that we have “2% inflation” is preposterous. From common and broad experience, it looks like something at least around 5% (note the coincidence that with a $20 Trillion economy, we’re running a $1 Trillion debt….?). That number, of course, is unacceptable to the “government,” so we’re told it’s under control at 2%; along with countless other asinine proclamations.

Second, Lord Keynes, when faced with the question of what would happen to his policies as they extended into the current circumstance, he jokingly said, “well, in the end we’re all dead.” The reality is that Keynesian economics were the intellectually absurd progressive fantasy of the time; as preposterous as today’s “progressive” thought; but eagerly adopted by the free lunch crowd.

Third, the volume of outstanding debt running at negative rates should make everyone leery of the entire structure. It appears unstable and very threatening to the overall economy.

I have a problem not with your analysis Mish, but the FRED chart that shows rent tracking wage growth while house prices skyrocketed. My rent here in Southern Oregon has also skyrocketed up about 90% since the 2013/14 lease period. That is actually a larger gain than housing to purchase, though real estate to buy is also way up from the lows. I say ABOUT 90% because the market is so screwed up that the data is hard to come by and harder to interpret, in fact the vacancy rate in this county (pop about 225k) was then 5.6% and now is well under 1% and that less than 1% available is a little bit substandard units in bad neighborhoods that nobody will rent at any price, or it is very top end lux that very VERY few can afford even with roommates. The middle market is full, when I moved back here from Las Vegas in February the first place I looked at was being shown like it was a prize dairy cow at a farmers auction, there was a line of about 50 people waiting to get in and see it so they could put in an application for it. CraigsList used to have 450-550 unique rentals on an average day in my price range (700-900 depending on the place’s features) now the only thing you find on CL in that rent range are tent sites and RV’s.

This is a great deal of the reason I say inflation is astronomically higher than the claimed headline number. Prices for food ditto, yesterday I went to Slaveway for a frozen pizza and some ice cream. The pizza I was buying at $5 last year was $9.99 yesterday, that is up 100% in a year. Even the lowly refried bean, 2 bucks a can, it was 49 cents just a couple years ago, 79 cents last year. I really want to just break some teeth when people claim inflation is 1. anything percent.

Last Year: “real estate is risk free, because housing prices always go up! And anyway, the subprime contagion is well contained”

Next Year: “Who could have anticipated that government debt is as worthless as other political promises?”

Yields are reaching dot-com or Miami condo flipping levels

Mish, great post. What’s the likelihood of the Fed (through their banking buddies) following the BOJ and purchasing stocks in the next downturn in order to maintain the wealth effect?

100%, if you allow for indirect purchasing, and extend “next” to “some future.”

Redistributing wealth from the productive to the wealthy and connected, meaning asset owners, is what the Fed exists to do. As long as they exist, and there exist even penny of confiscatable wealth or productive output to redistribute, that is what they will do. The exact mechanism is just minor detail and obfuscation.

How much of this upcoming recession is being planned? Going into an election cycle with a “revised” recession isn’t ever good for the incumbent. Everything in the Democratic Party debates has been economic gloom and doom and there’s plenty to blame on the current administration.

I’m not saying this is all a vast conspiracy by the Democrats, but I am saying it could easily be a vast conspiracy by the bureaucracy. That same bureaucracy who Trump compared to a swamp creature. That same bureaucracy who was told to implement a policy of eliminating two regulations for every new one. That same bureaucracy who probably has a real vested interest in an ever-growing executive branch. It would be pretty easy to massage the obviously weak economic data, or just “revise” it ad nauseam so the real numbers come out 6 months from now. And who are you going to believe? Trump with his hyperbole, or the meritocracy with their centuries (collectively) of experience?

It was not the bureaucracy that said trade wars are EASY TO WIN. And now we are to be told that currency wars are also easy to win. I doubt that the democrats have anything to do with the growing catastrophe in the economy, but, they certainly can (and should) exploit it for all it is worth.

I would be okay with a centrist of either party, I changed my registration to be able to vote for Weld in the primary, unfortunately our primary is one of the very last in the second half of May, so it is all over by then. I just donated a little sofa pillow change to Mayor Pete as well.

Finally a non Brexit post. This is the old Mish.

Brexit is not important. Britain never dissolved their own currency.

“Prove Rising Prices Provide an Overall Economic Benefit”

I can prove the Keynesians wrong once more: In addition to the BIS paper, several other studies by the NBER show that falling consumer prices are not harmful. Also, historian David Hackett Fischer in his book ‘The Great Wave’ examines price developments from the Middle Ages until modern times, and finds that periods with no inflation or falling prices are most prosperous.

Debt+Deflation=Depression.

We may see investment asset deflation if credit unwinds a bit coupled with consumer goods inflation if tariff man keep on the same path. Hard to see whats in the crystal ball, change tho is coming, the current ponzi debt stock market scheme doesn’t look sustainable long term. It sure has lasted far longer than I ever thought it would.

What if the debt is so big that it cannot be repaid unless you go full Weimar? watched Max Keiser who has said for the longest time that QE is a Ponzi scheme and you cannot taper a Ponzi. It seems to me that we are in unchartered waters and it is anyone’s guess what is going to happen. The only consensus is that it is going to be bad. How bad anyone?

And it may very well happen. Weimar is a possibility.

“What if the debt is so big that it cannot be repaid unless you go full Weimar?”

Then don’t repay it.

Bankruptcy processes are both well established historically, from waaay before the onset of the current dimwitted fascination with progressive idiocies, and in no way whatsoever neither systemically bad nor destructive.

I wish I had your equanimity. Once the general populace become aware of what is going on there will be hell to pay.

The fed needs to keep the stock market inflated. Pension plans are still underwater… can you image a few years of negative or no stock growth? There would be chaos

Technology has helped keep certain asset prices down. Technological advances are deflationary on prices by nature.

We have record number of homeless and record high housing costs. I think we should abolish ICE and open the borders and let in whoever wants in.

What in the hell would that solve? More homeless, jobless people is a solution?

It’s called sarcasm.

ICE is a government agency. A three letter one. And one which did not exist back when America was civilized, to boot. Hence, abolishing it is good, a priori. It helps solve the only real economic, social and political problem which exist in this world: Too much, and too big, government. Any other ostensible “problems” are just side effects of that one.

Of course it’s the debt. Lacy Hunt has been consistently 100% correct on this for years. Anyone (and there were many so-called Bond Kings among them) who thought the Fed could ever get close to “normalizing” rates proved themselves to be useless fools. As more and more debt is forced into the system, growth will slow even further (or cease altogether) and rates will be forced lower and lower. Credit-based, fiat currency endgame, in progress.

Bond kings are in trouble. Hedge funds are in more trouble. Many hedge funds have had it.

“Mish, why do you expect next recession/crisis to be less severe, or less sudden, than the Great Recession? There’s even more debt now and fewer tools for papering it over, no?”

Credit conditions different

The bubble in junk bonds bigger than the housing bubble

Fewer jobs lost and fewer homes repossessed

A longer and shallower recession

May revise this a bit and write it up

“The Fed remains on a foolish mission to achieve 2% inflation.”

…

Great question. Partly due to erroneous thinking that threat of inflation will induce consumers to not delay purchase, but,(imo) main reason is to benefit … you guessed it … Wall Street. The Federal Reserve damn well knows it has/is/will create asset inflation … in spades. All for the sake of the skim. If an asset class generates double digit returns annually … no one really cares about 2% or 3% management/sales fees. OTOH, if asset class return grew (a lot) slower (ie: organically), then people would damn well care about those 2% or 3% fees. Sustainable growth does not lend itself to flipping/hot money/etc. which plays right into Wall Street’s hands.

People need to realize the Federal Reserve is not owned by the government / the people, but by major banks. Who want to profit off the people, not help them.

Mish, why do you expect next recession/crisis to be less severe, or less sudden, than the Great Recession? There’s even more debt now and fewer tools for papering it over, no?

One of the areas I disagree with Mish.

Fully expect a repeat of Fall of 2008 / early 2009. For several reasons, but main one is for another episode of Shock Doctrine (massive taxpayer funded bailout of Wall Street. A see-saw down trend for several years does not allow the opportunity.

During the summer of 2008 I watched a fair bit of the Larry Kudlow Show. He spent the summer talking over (that is how you win an arguement, right?) anyone hoo dared to suggest country in recession. Well, he – finally – capitulated around Labor Day. A mere few weeks later he was pounding the desk for TARP – “a reboot for kapitalism”.

Hhmm, wonder where that guy went …

Maybe he figures they will be quicker intervene on an even bigger scale?

The price increase/decrease(and base inflation/deflation) debate continues among the big league/well known observers of the stock market/Fed Res policy/Gov’t debt set.

I really don’t know which side is right…time will tell obviously.

It’s pretty simple. Inflation is coming. No, really.

Smart Indians prospered by knowing to get off a dead horse. Today, smart central bankers know to stay on the dead horse until others believe it’s dead.

“When you discover that you are riding a dead horse, the best strategy is to dismount.”

However, many leaders and organizations relent and persevere with the dead horse and more advanced strategies are often employed, such as:

And, of course…

“It’s asset bubble deflation that is damaging.”

Exactly how is blatantly mispriced goods becoming less so “damaging?”

Negative interest rates cause deflation. The rational response to negative interest rates is to remove currency from banks and from circulation. The effective money supply must contract.

How amusing that the European Central Bank responds to deflation with more and more negative interest rates.

There is nothing wrong with debt if you have the means to service it and pay it off in the end. Young people arent gonna be able to get started without it. Obviously, someone forgot about any plan to service the debt … on ALL levels (govt., business, personal, etc)

“There is nothing wrong with debt if you have the means to service it and pay it off in the end.”

Depends on the specifics of the “means” you are referring to. Anyone with a printing press, has the means to service their debt, Weimar style.

For “debt” and “servicing debt” to have any meaning at all, it first needs to be well defined. In economically meaningful terms. Which requires debt to be nominated in something which is stable, or at the very minimum predictable. And which hence cannot simply be altered/printed up etc.. Otherwise, all you’re doing is arguing over how tall someone is, when measured in units you can arbitrarily change at your will.

“There is nothing wrong with debt if you have the means to service it and pay it off in the end.”

Yes, there is something wrong with it, especially when you are NOT using debt, yet are forced to compete with those that are. You end up paying higher prices than you otherwise would in a free market. How many people buying houses today are actually planning (and have the means) to pay it off? Same with higher education. Those paying full asking price become the patsies when the future bailouts come.

Production debt good, consumption debt bad.

Logically, yes.

But the two are, in practice, indistinguishable. Even in theory.

Excellent article, Mish. It’s the debt.