PLease consider the New York Fed report How Did the Fed Funds Market Change When Excess Reserves Were Abundant?

Major Participants in the Fed Funds Market When Excess Reserves Were Abundant

Lenders – Federal Home Loan Banks

The Federal Home Loan Bank system was created by Congress in 1932 to facilitate financing in the U.S. housing market. The FHLBs accomplish this mission by lending to banks that lend in the U.S. housing market. FHLB liquidity buffer assets typically consist of fed funds sold, Treasury bill securities, and Treasury reverse repo investments. FHLB liquidity buffers also serve as a reserve of liquidity that can be drawn upon to grant member advances on a timely basis.

Because FHLBs are not deposit-taking institutions, they are not subject to reserve requirements and thus are ineligible to earn IOER from the Fed. Since they are not eligible for IOER, FHLBs are challenged in their efforts to obtain interest income on their liquidity pools. FHLBs have a strong motivation to sell fed funds, since whatever rate they obtain on fed funds transactions is greater than the zero compensation they would receive on any end-of-day balances held in their accounts at the Fed.

Borrowers – Foreign Banking Organizations

In the post-crisis environment of abundant reserve balances, most fed funds borrowing transactions are motivated by “IOER arbitrage”—borrowing overnight at a rate below the IOER rate, leaving the funds at the Federal Reserve overnight to earn the IOER rate, and earning a positive spread on the transaction. Foreign banking organizations (FBOs) currently have a large presence in the fed funds market because of their borrowing advantage over domestic banking institutions*. Since FBOs do not offer retail deposits, they are exempt from paying Federal Deposit Insurance Corporation (FDIC) insurance assessments, which all domestic banks must pay*.

FBOs are willing to engage in overnight fed funds transactions as long as they can earn a “reasonable” spread. FBO borrowers do not have a consensus on what constitutes a reasonable spread, but indications are that IOER arbitrage starts to become less attractive when the spread is five basis points or less.

Congratulations to Foreign Banks

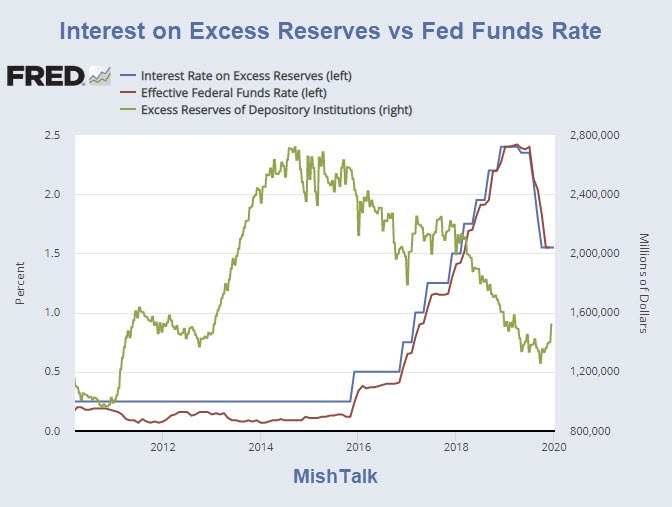

My chart shows that foreign banks were the biggest beneficiaries of the Fed’s policy of paying interest on excess reserves from the outset all the way through December of 2018.

Sorry foreign banks, you are now on your own it seems.

Mike “Mish” Shedlock

A question about an apparent contradiction here. “Because FHLBs are not deposit-taking institutions, they are not subject to reserve requirements and thus are ineligible to earn IOER from the Fed.” and “Since FBOs do not offer retail deposits, they are exempt from paying Federal Deposit Insurance Corporation (FDIC) insurance assessments, which all domestic banks must pay*.”. How can the foreign banks earn IOER if they are like FHLBs NOT depositary institutions? Is there a list of these foreign banks somewhere using this arbitrage?

Thanks!

The Fed’s actions, especially TRYING to keep rates down has ALWAYS been about helping foreign entities with massive piles of dollar-based debts that will explode WHEN the dollar and rates rise. The Fed has become the world CB, but they are all completely trapped with no escape. The will fail to keep a lid on rates!

Up until 2016 IOER was a mere 25 basis points, spread half that – tough to make a fortune off that, but it was free money

With NIRP in Europe, certainly those foreign banks could have borrowed at a lower rate than what the FED was offering, deposit excess reserves, and profit from an arbitrage. The beneficiary would have been a much stronger dollar with Euros being exchanged for US dollars.

So why didn’t foreign banks exploit the arbitrage to the point of a much stronger US dollar?

Why are European banks still in trouble despite that arbitrage lasting so long?

Would foreign banks and the Federal Reserve by chance be associated to a common entity?