Here are some snips from James Montier’s excellent article on the Advent of a Cynical Bubble.

For ease in reading and to display the charts as large as possible, I dispense with blockquotes. I will mark the end ofMontier’s excellent articlewith a a comment.

That the US equity market is obscenely overvalued can hardly be news to anyone. Even a cursory glance at Exhibit 1 reveals that we are now at the second most expensive level of the Shiller P/E ever seen – surpassed only by the TMT bubble of the late 1990s!

Only a handful of what we might call valuation deniers remain. They are dedicated to finding new and inventive ways to make equities look reasonable, and they have never yet met a bull market that they didn’t love.

As we have documented before, the Shiller P/E isn’t perfect, but it does a pretty good job of providing a really simple way of checking valuation. Nor is it unique in showing the US equity market to be extremely expensive. So for all the hand-wringing over the inclusion of 2009 in the 10-year average, the lack of robustness, shifting payout policy, etc., that haunts discussions based on the Shiller P/E, it is still a very powerful metric.

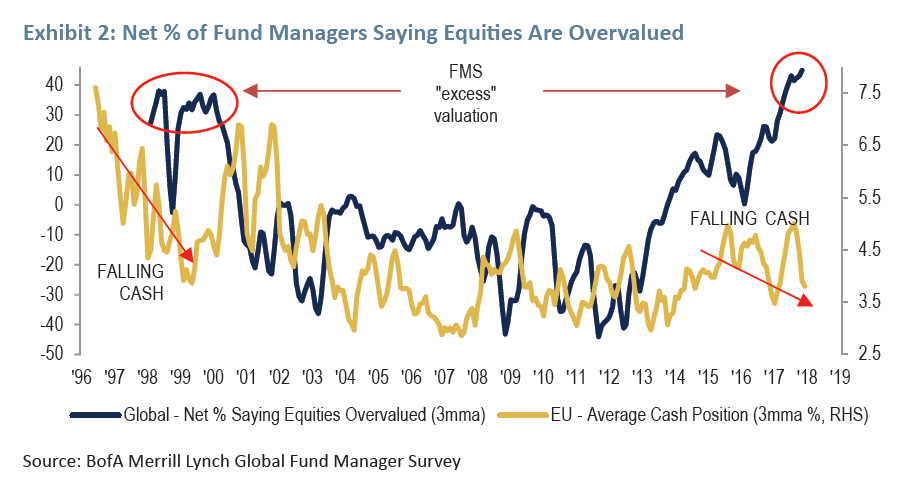

This is not news to most institutional investors. A recent Bank of America ML survey showed the highest level of those citing “excessive valuation” ever (see Exhibit 2). [Mish Note: lead-in Image]

Yet despite this, the same survey showed fund managers to still be overweight in equities.This gives rise to the existence of that strangest of creatures: the fully-invested bear. The most common rationale for such a cognitively dissonant stance is “the fear of missing out on the upside”(aka FOMO – fear of missing out). As I think Seth Klarman pointed out long ago, this isn’t really fear at all, but rather greed.

The fully-invested bear seems to essentially subscribe to Jeremy Grantham’s market melt-up scenario. I certainly can’t rule such an occurrence out. The strongest piece of evidence for it from a personal perspective comes from my own track record of being early in calling bubbles. In 1995 I wrote a piece arguing that Thailand would be the next Mexico (2 years too early); in 1997 I wrote piece arguing we were witnessing the last hurrah in equity markets (3 years too early); and in 2005 I wrote a piece on the bubble in US housing (2 to 3 years too early). This is the curse of those who follow the edicts of value. Valuation is a useful long-term indicator, but not a good short-term indicator. So perhaps the best way to read my research is to put it in a drawer for two years and then take it out and read it!

Bursting Cynical Bubbles

I have already confessed a pathetic lack of ability when it comes to timing a bubble’s demise. It is one of the many reasons I regularly extol the concept of patience as a symbiotic to following a value based approach.

However, I do know that cynical bubbles are based on a belief that one can get out before everyone else. Obviously, this is simply impossible. Like a game of musical chairs played at a child’s birthday party, when the chairs are increasingly rare, the competition for them gets fiercer. Crowded exits don’t end well – inevitably some are crushed in the stampede.

Now, perhaps you are skilled at picking the managers with great timing ability, and perhaps those managers do have great timing ability, in which case, good luck. As for me, I prefer to leave the party early, in the knowledge that I can walk away with ease.

EndJames Montier

My comments follow.

Fully Invested Bears Makes Perfect Sense

The concept of fully invested bears actually makes perfect sense.

If you are a fund manager you know full well that the one and only thing clients cannot stand is underperformance. And as long as bubbles last (this one has been amazing), you are going to lose clients for underperforming.

In this context, investing with leverage makes complete sense. Funds pour in and so do profits to the fund managers.

Doing what one believes is damn hard when client fees get in the way. If you blow up, as several VIX-related funds did, you start over with a new message.

To make a bubble top, fund managers have to be extremely one-sided to the point they just do not give a damn if the whole thing blows up. Meanwhile, as long as fees roll in, who cares about clients’ best interests?

Mike “Mish” Shedlock

However despite this, the same study shows fund managers to still be overweight in statistics. The most common reason for such dissonant cognitive deficits is “fear of losing up” (aka FOMO – fear of missing out). I got link to zotero.org . As I think Seth Klarman pointed out a long time ago, this is not fear at all, but rather greed.

link to obatperangsangmanjur.net

Schiller, and the rest who look at valuations with domestic blinders miss the biggest factor – global capital flows. When was the last time a bubble popped in the govt bond market of the reserve currency? How is CAPE or any other valuation metric going to capture the move from public to private, where stocks become the safe haven?

link to armstrongeconomics.com

link to armstrongeconomics.com

If you are an investment adviser, you have to be invested in something, because your clients will balk at paying a management fee for sitting in cash, even if that’s the best possible investment choice.

I think this is why Trump didn’t keep Yellen. I think he like the job she did (print, print, print) but was afraid he couldn’t trust her and would allow a major correction during his presidency.

The market isn’t cheap but the Shiller P/E exaggerates how expensive it is by not only still including the financial crisis years, but also the suppressed growth of the early Obama years. The point of the Shiller P/E is to smooth out earning to make them more realistic, but it may be having the opposite effect today.

As long as you believe you can count on the Fed and government being there to socialize most of your downside; fear of missing out on even fairly farfetched upsides, does become a more rational preoccupation.

Since the only thing propping the illusion that financialization, legalification, regulation and centralized managament is somehow a creator/enabler of real wealth up, is that the Fed and government has so far been willing, and able, to go to any length keep it thus, that’s not necessarily a bad bet.

You’re essentially betting that the rulers, by force, will continue to be able to beat nature and fundamental economics for a bit longer. It worked for the Soviets for quite some time, so it’s not a given that it won’t work for a bit longer here as well.