Strong Rebound But

The BEA reports real gross domestic product (GDP) increased at an annual rate of 33.1 percent in the third quarter of 2020 according to the “advance” estimate released by the Bureau of Economic Analysis. In the second quarter, real GDP decreased 31.4 percent.

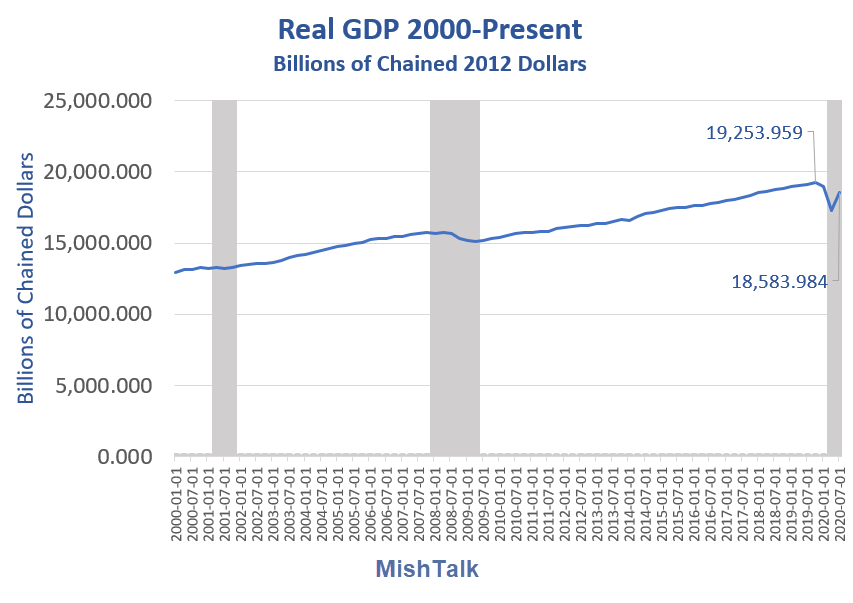

Economy Not Recovered

The above chart from the BEA makes it appear as if the economy has fully recovered. It hasn’t.

The economy is about a trillion dollars short of the peak as my lead chart shows.

The BEA assumed an effective annualized deflator of 1.38% for Q3.

That estimate dramatically understates what the inflation rate would be if housing prices were factored in. It also ignores the stock market bubble, another measure of inflation but one impossible to quantify accurately.

The end result is GDP is very overstated.

The Consumer Metrics Institute accurately comments:

This astounding headline number is a consequence of the BEA’s methodology of annualizing quarter-to-quarter changes, similar to last quarter’s preliminary headline of a catastrophic 33% contraction. Down 33% and then up 33% does not put you back at the point where you started. After a 33% contraction you need 50% in growth to accomplish that feat.

Notable Items

- Consumer spending for goods was reported to be contracting at a -0.27% rate, down -0.39pp from the prior quarter.

- The contribution to the headline from consumer spending on services was reported to be -4.99%, down -6.11pp from the prior quarter. The combined consumer contribution to the headline number was -5.26%, down -6.50pp from the prior quarter.

- The headline contribution for commercial/private fixed investments was reported to be -0.43%, down -0.34pp from the prior quarter.

- Inventories subtracted -0.53% from the headline number, up 0.45pp from the prior quarter. It is important to remember that the BEA’s inventory numbers are exceptionally noisy (and susceptible to significant distortions/anomalies caused by commodity pricing or currency swings) while ultimately representing a zero reverting (and long term essentially zero sum) series.

- The contribution to the headline from governmental spending was reported to be 0.13%, down -0.31pp from the prior quarter.

- The contribution from exports was reported to be -1.02%, down -1.26pp from the prior quarter.

- Imports added 2.32% annualized ‘growth’ to the headline number, up 1.05pp from the prior quarter. Foreign trade contributed a net 1.30pp to the headline number.

- The annualized growth in the ‘real final sales of domestic product’ was reported to be -4.26%, down -7.36pp from the prior quarter. This is the BEA’s ‘bottom line’ measurement of the economy (and it excludes the inventory data).

- Real per-capita annualized disposable income was reported to have increased by $11 quarter to quarter. The annualized household savings rate was 9.6% (up 2.0pp from the prior quarter). In the 47 quarters since 2Q-2008 the cumulative annualized growth rate for real per-capita disposable income has been 1.45%.

No V-Shaped Recovery

There was a strong rebound but don’t expect a V-Shaped recovery.

Why?

- A third wave of Covid is underway in the US. Covid Cases are at a Record High. Covid Records Shattered In The US and Europe. More cities and states are shuttering restaurants and bars again.

- Boeing, Raytheon, and the Airlines are all laying off workers starting October. These layoffs have not hit the jobs reports yet.

- Congress did not pass another Covid stimulus package. There will be another stimulus package after the election, but it will kick in with a lag.

- State Level Unemployment Benefits Are Rapidly Expiring

- The Herd Immunity Theory is in Serious Doubt

Mish

A couple of quotes from an article on Goldmoney.com “The fate of the pound Sterling” on GDP as a measure.

“At this juncture, it is important to understand something to which macroeconomists are generally blind: GDP is the sum total of all transactions, which without the addition of extra money is a static figure.”

“Another way of looking at the relationship is to understand that, apart from some minor variations in money retained for liquidity purposes, all money and profits earned are spent or saved, the latter being deferred consumption, supplying investment capital. With no change in the quantity of circulating currency there can be no change in the total spent and saved, and it is these totals that make up GDP, whether accounted for from the production or consumption sides.”

Therefore, without QE, the monetary value of transactions in the economy measured in pre-expansion dollars would have been a lot less than the reported GDP.

This is true….but what THAT quote misses is that we have this issue….it takes more and more money to be created…….to achieve the same amount of GDP growth……QE works a little less well each time we turn on the faucets.

Error: “After a 33% contraction you need 50% in growth.” A 31.4% contraction in this context is essentially .314/4 since it was annualized. Quarterly growth needed to restore that is 8.5% which would be annualized to 34% which is not similar to the innumerately calculated 50%.

After a budget deficit of some 3T and other measures, this is the most expensive recovery ever. The GDP should be overlaid against debt or it’s just a fake number (actually one of many).

It was good number but we’re still 4% below where we were before the pandemic. Employment is lower and it doesn’t seem like there will be much additional momentum. Pandemic is getting worse in all 50 states and Europe is heading towrd more lockdowns. And without a government spending bill i don’t see where the impetus comes from. Companies and state governments aren’t getting help from the federal government either on testing . Seems clear we’ll see layoffs at the local government level too.

I agree. This is all stimulus related. Once unemployment runs out and the holiday season is finished, then we will see. Im not counting a second lockdown just yet, like France and Italy. I do think a 2nd lockdown would cripple more businesses and increase unemployment. Another stimulus is required in my opinion, but a more comprehensive plan is needed to get things moving again

I don’t see lock down like France or Italy or Spain but i think we’re headed to some localized ones. In some areas of the country the infection rate is above where it was in the spring. Nobody wanted to take small helpful steps like wear a mask. We need reset now. We’ll probably see bars and restaurants closed and travel and gatherings limiited . We’re not even well into the fall and winter. this looks like freaking disaster. it will get worse

As usual, it’s only the headline that matters. Everything is just great. #sarc

The U.S. Supreme Court’s conservatives are carving a path that could let President Trump win a contested race

Q3 is much better than Q2 and even though Q3 did not make up for Q2 the trend is still positive. It is not a V recovery but it will do.

Brutus:

“There is a tide in the affairs of men.

Which, taken at the flood, leads on to fortune;

Omitted, all the voyage of their life

Is bound in shallows and in miseries.

On such a full sea are we now afloat,

And we must take the current when it serves,

Or lose our ventures.”

The trend is your friend.

The Hubble Space Telescope spies a metal ore asteroid worth an estimated ten-thousand times the global economy of 2019 link to observer.com

It’s almost all composed if iron and nickel which are readily available here on Earth. There is no mention of handwavium, unobtanium and wishalloy so I assume they are in insignificant amounts.

Iron & nickel are very heavy and would be prohibitively expensive to lift into manufacturing factories in Earth orbit with today’s technology. We would need to move source asteroids closer to Earth or manufacture in the asteroid belt and then tow finished products back to planetary orbits for use in building ships or stations..

Other solutions might include mining the moon, Mars or a space elevator.

Nickel-Iron asteroids are common enough to mine. Even a small one yields enough building material to make habitations. No need to go for the big one when small ones are much easier to work with. Nullifying its rotation would take way too much energy.

Just tell Elon to hit the remote start on that Tesla he has floating around out there and pull that bad boy back to low earth orbit.

If you actually get the whole asteroid onto the earth, its quantity will make it worth close to $0, just like ordinary earth soil.

The asteroids up close are always different than expected. NASA landed something on an asteroid they thought had a soft surface. Instead it was covered with rocks.

This is a good tie-in article.

I Ran the Numbers Again. Stocks Are Not the Economy.

Even when using an equal-weight measure for the S&P 500 and not adjusting for inflation, there is no correlation between the market and GDP.

By Nir Kaissar

October 27, 2020, 6:00 AM EDT

Ever since U.S. stocks began rebounding from their depths of late March, there has been a glaring, and many would say disturbing, disconnect between the devastating impact of Covid-19 on the economy and the celebratory mood of the stock market. Seven months later, that disconnect is as deep as ever. The virus continues to plague the economy and the well-being of millions of Americans while the market marches higher.

I agree GDP is a rubbish measure. The long term relationship is with company earnings.

Added Blurb:

The BEA assumed an effective annualized deflator of 1.38% for Q3.

That estimate dramatically understates what the inflation rate would be if housing prices were factored in. It also ignores the stock market bubble, another measure of inflation but one impossible to quantify accurately.

The end result is GDP is very overstated.

Inflation is always going to be low. If beef becomes too expensive, people will eat chicken. If chicken is too expensive, we’ll eat tofu. etc… until if food in general is too expensive, we’ll plant our own seeds and grow our own food for free.

What rate is used to convert nominal to real? Do the “real” numbers reflect all the printing or is there a lag?

They use the “GDP Deflator” it frequently varies widely from the CPI.

For this estimate the BEA assumed an effective annualized deflator of 1.38%.

Thank you – some day we’ll stop lying to ourselves, until then I appreciate the filter.

How could there not be a strong rebound after government pumped trillions in the economy after shutting it down. If you shut it down, it was obvious GDP was going to slide by double digits. Isn’t it expected to do the opposite once everything starts looking more normal while government pumps money into the economy?

The quarter that it seems to me is a more accurate depiction of where we are at would be the fourth quarter wouldn’t it? Unless of course there is another lockdown…

Using annualized quarterly numbers make sense in a steadily growing economy, but they’re a ridiculous measure during a shock. The year-over-year (YoY) numbers are the only ones that make sense in a shock like COVID.

I think the YoY for Q2 was something like -10% and YoY of Q3 is something like -4%.

if we step up the number of covid tests, will that help gdp?

Nooo!

Fat Donnie says: reduce the number of tests and we reduce the number of cases.

It would give communities and states a better sense of where hotspots are so that they can target shutdowns, rather than do a blanket shutdown everywhere.

Had we done what Harvard University called for back in April, and done massive testing, we wouldn’t be facing this looming national shutdown.