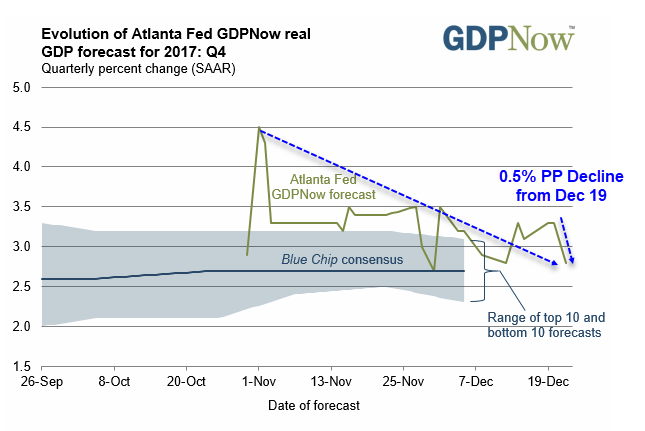

The Atlanta Fed GDPNow Model has shown similar patterns for three quarters: High initial estimates followed by a choppy dive much lower as the quarter progresses. The reasons vary quarter to quarter but the pattern remains the same.

In contrast to GDPNow, the New York Fed Nowcast Model frequently starts the quarter low then rises.

GDPNow 4th-Quarter Forecast: 2.8% — December 22, 2017

- The GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2017 is 2.8 percent on December 22, down from 3.3 percent on December 19.

- The forecast of fourth-quarter real consumer spending growth fell from 3.1 percent to 2.9 percent after this morning’s personal income and outlays release from the U.S. Bureau of Economic Analysis (BEA).

- The forecast of the contribution of inventory investment fell from -0.14 percentage points to -0.40 percentage points after this morning’s advance durable manufacturing release from the U.S. Census Bureau and the release of the revised underlying detail tables for the National Income and Product Accounts by the BEA this morning.

Nowcast 4th-Quarter Forecast: 3.9 Percent — December 22, 2017

Whereas GDPNow only forecasts for the current quarter, Nowcast forecasts two quarters.

Nowcast 1st-Quarter Forecast: 3.2 Percent — December 22, 2017

Nowcast Summary

- The New York Fed Staff Nowcast stands at 3.9% for 2017:Q4 and 3.2% for 2018:Q1.

- News from this week’s data releases decreased the nowcast for 2017:Q4 by 0.1 percentage point and left the nowcast for 2018:Q1 broadly unchanged.

- Positive surprises from survey data and from housing data on net were offset by negative surprises from manufacturing data and by the negative impact of data revisions.

Data Impact on Nowcast

Nowcast vs GDPNow

- Housing had no impact on GDPNow.

- The current housing reports added a net 0.06 percentage points to Nowcast, but revisions subtracted 0.09 percentage points.

- The manufacturing report subtracted a miniscule 0.01 inventory percentage points from Nowcast but a relatively whopping 0.26 from GDPNow.

- The income and expenditures report added a tiny 0.01 percentage points to Nowcast but subtracted a hefty 0.2 percentage points from GDPNow.

Durable Goods

Given my take Durable Goods Orders Disappoint, I am not surprised by the GDPNow dip from manufacturing.

Housing

In regards to housing, GDPNow does not even look at the new home sales report.

For Nowcast, it would seem that the revisions to October new home sales would weigh on the fourth-quarter GDP a bit, but the current report should add quite a bit to first-quarter GDP.

My reasoning is construction may not start immediately but construction for October sales (revised lower) will likely start this year, adding less than previously estimated to 4th-quarter GDP.

I would recon the sharp increase in new home sales in November would be quite positive for first-quarter GDP.

However, the net impact was more along the lines of the apparent GDPNow take of “why bother?”

For housing details, including the oversized October revisions, please see New Home Sales Spike Most in 25 Years: What’s Going On?

Income and Outlays

Also consider Spending Up Far More than Real Income: Per Capita Income Stagnates.

The income report shows spending rose 0.4%, a seeming positive for GDP.

Yet, the impact was benign for Nowcast and sharply negative for GDPNow.

Model Synopsis

Once again, it’s not the news itself that matters, it’s what the model predicted vs the actual data that matters.

Nowcast did not react to spending or inventories because that’s what its model expected.

In that regard, the volatility of GDPNow vs Nowcast on any given report makes it difficult to accurately game how the models will react to any give news.

In recent quarters, despite the volatility, GDPNow has been reasonably accurate in its final estimate.

Mike “Mish” Shedlock

Inflated GDP figures boost consumer confidence, consumers spend more on Christmas, Christmas season is over, GDP goes back to where it was, don’t you know anything?

I think weakness from inventory reduction is positive for future growth

No matter if the final is 2.8 or 3.whatever, it is far better than 1.5 growth we had the 8 years of Obama. More growth to come.

new fed head will push for even moar money printing,powell 1st day in office look for interest rate cut,NIRP.Deficit will double,might triple as the money printing (an inflation)soar