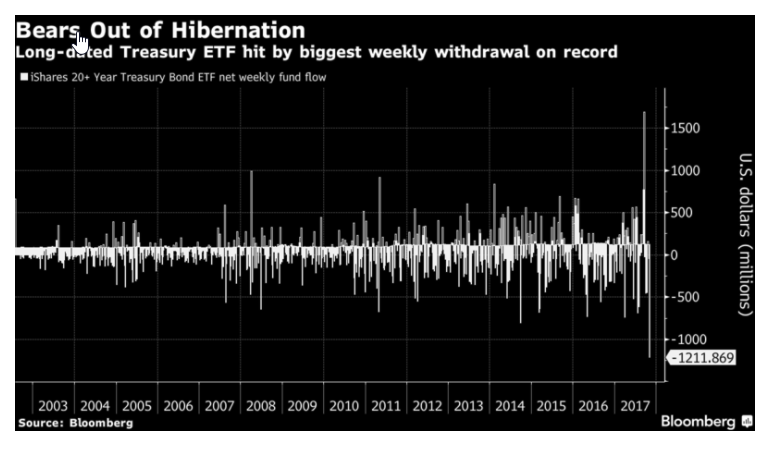

In what I view as a strong contrarian indicator, Long Treasury ETF Posts Record Outflow in Duration Rotation.

Some investors are paring exposure to longer-maturity U.S. debt as the Federal Reserve moves closer to normalizing borrowing conditions in the midst of a leadership transition.

The iShares iBoxx $ Investment Grade Corporate Bond ETF was hit by $460 million of outflows last week, its fourth-biggest withdrawal of the year. The $38.6 billion fund has an effective duration of 8.8 years, meaning it’s acutely vulnerable to price swings spurred by interest-rate changes.

By contrast, shorter-maturity Treasury and corporate funds saw inflows last week, including the SPDR Bloomberg Barclays Short Term High Yield ETF, the iShares 0-5 Year Corporate Bond product and SPDR’s 1-3 Month Treasury Bill fund.

Treasury Yields

There is no reason to believe the long-term treasury bull market is over, either fundamentally or technically. The trend is down, down, down.

Money managers pulling out now will likely chase the rally when it’s clear the economy is going nowhere. By then, yields may be much lower.

I stick with my call made two days ago: I Expect New Record Low Long Bond Yield.

Despite all the economic cheerleading about the allegedly strengthening economy, I see things differently. Job growth is shrinking. Average the last two months to smooth out the hurricanes and you get growth job growth of 114,000. For now, it’s still positive.

Household formation is the weakest since 2010.

Hooray, autos rebounded. However, 100% of that rebound is due to hurricane replacement. It won’t last.

Rental Vacancies Are Rising. What will that do to new apartment construction?

What growth we have is due to a diminishing savings rate . That’s another hurricane aspect that won’t last.

Construction Spending Shows Serious Signs of Rolling Over.

If the economy was getting stronger, trends in long-term treasury yields would not look like they do.

Mike “Mish” Shedlock

@TheLege. Even in deflation yields can go up. The investing landscape is heavily leveraged. As companies default on loans, leveraged investors will unwind even their safe investments to cover margin calls.

In any event, I think similar easy money policies in our neck of the woods is going to have a markedly different outcome — even if the Japanese economy must eventually bow to the laws of economics.

3. I believe in Japan there is a culture that leans toward keeping everyone employed — companies would be more inclined to run with their deadwood and ‘bloat’ than follow the aggressive Anglosphere model of hire ‘n fire. The staff bloat, along with the fact that Japan is still full of zombie companies (from the heady ’90s bust) means that staff wages are necessarily stagnant (with possibly some downward bias).

That was 2. 🙂

2. In addition, the Japanese have the largest demographic headwind of any developed country — this is deflationary and counteracts some/all of the inflationary policies in play.

1. QE works slightly differently in Japan in that only reserves are credited in the bond ‘purchase’ process, whereas, in the US new bank deposits are created as well so there is a direct boost to money supply in the US but not so in Japan.

hmk, how’s this for size …

Not buying it. Construction has labor shortages and skyrocketing material costs. This equals inflation despite the propaganda numbers the monetary politburo spews out. The only way they keep Treasuries yields low is by printing money and having the fed buy them all like in Japan. This in theory would weaken the dollar and cause inflation again. Somehow this crap works in Japan and maybe it will here. I don’t know I’m confused.