I got the idea for the above graph from a similar idea by Sven Henrich.

In my chart, I indexed all the values to 1982.

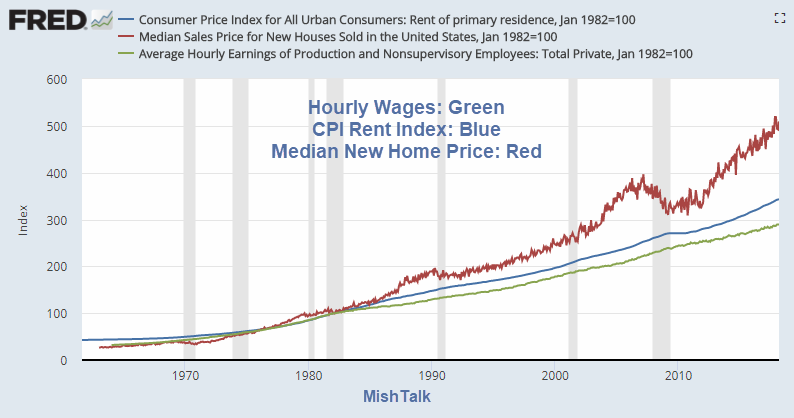

Key Ideas

- Those who seek to buy their first home will have a very difficult time finding one that is affordable.

- There was a small window of buying opportunity from 2009 to 2011 but that window has since been closed.

- Making matters worse, rent prices accelerated in 2011 and far outstrip wage growth.

Median vs Average Wages

It’s important to note that hourly wages are averages. The median wage earner is even worse off.

The latest median wage data is from May of 2016. It shows real median wages decline in seven out of the last 11 years.

For details, please see How the Fed’s Inflation Policies Crucify Workers in Pictures.

Mike “Mish” Shedlock

@krungthep

The trick the Fed, the Junta, and their support army of rent seeking leeches, are trying to pull off; is to allow for rents to drift low enough to be ultimately affordable. BUT, ensuring all new units are located underneath freeways next to Uranium mines, are at most 40 square feet, are built of recycled toilet paper, has tightly allocated running water and no access for privately owned vehicles.

While being sold on contracts that 1) mandates that the residents are “gainfully” (for the leeches, of course..) employed; picked up by the labor transporter at 6am, dropped back at 8pm. 2) stipulates that the lucky owner’s daughters (and in San Francisco, sons as well…) receive mandatory sexual education by members of the leeching class. All for national security, of course. Wouldn’t want risking them becoming one of those scary virgins past the age of 12….

IOW, nothing new under the sun. Just a natural continuation of ensuring the captive population is always getting less for more. Which was, is and always will be, the sole and only purpose of a Fed, 98% of “our”/any government, and 99% of “our” financial and legal “systems,” along with all their backers and beneficiaries.

Perfect picture of where we are and how we got here: By running the same, broken inflation-assuming model for 37 years. If the actual CPI over the period had been 4.44% instead of 3.44%, and wages had spiraled up in lock step with CPI, as in all past history, there’d be no gap. Two problems with the model’s assumptions: 1.The Chinese wouldn’t show up in a global economy with 500 million peasants willing to work for under $3.00/hour and 2.Ten years of cheap, saver-robbing capital wouldn’t greatly accelerate the pace of automation.

If rents and sale-prices both outstrip income, I have a pretty good idea what’s going to happen to rents and sale-prices. Tick tock.

The Fed reality: If you already have assets, congratulations, you might just stay afloat (and even feel the thrill of rising on the bubble of the moment). … If you don’t — sorry things didn’t work out for you!

That ain’t gonna happen without a revolution. Right now, the lenders own the government. To them, the government is a tool that is used to privatize profits and socialize losses.

Prices will plummet (and homes become less of a speculative asset class) as soon as the government gets out of the market place and lenders assume losses for bad loans.

This is how we transition from 1st world to 3rd world. One visceral reality at a time.

“Yet a little sleep, a little slumber, a little folding of the hands to sleep: So shall thy poverty come as one that travelleth, and thy want as an armed man.”

Mish, Does the deviation in median home prices start in 1987? From the chart it appears the deviation is fully the effect of the Fed’s (and other CBs) meddling with interest rates (and QE). Probably it has gone up and away after Draghi ‘s ‘whatever it takes’ . Looks like any time at moves to the trend line, the CBs just pull it away with asset inflation.

It’s a utopia that only a central banker would love. Excellent chart by the way.

Joe 6-Pack has his “balls in a vise” when it comes to housing, healthcare and higher education.

“Those who seek to buy their first home will have a very difficult time finding one that is affordable.”…which is fine since if no one can afford to buy a home, sellers will need to lower their price – that’s how markets work if allowed. The problem occurs when the government steps into the market in multiple ways to “make it affordable”. For example, did the multimillionaire Hannity really use HUD financing to purchase real estate? Why is the government backing the majority of loans originating today?

Trump’s partial elimination of the mortgage-interest deduction tax break and his increasing of the standard deduction are small, but important steps toward leveling the playing field.

Glad I bought my house in 1994. We had a choice of maybe 50 similar homes in our price range. Houses would frequently sit for 6 months or longer before being sold.