The Brookings Institute says a Liquidity Crises in the Mortgage Market is on the way.

This is in guest post format. What follows are key snips from a 68-page Brookings PDF.

This article isn’t very long. My comments follow.

Abstract

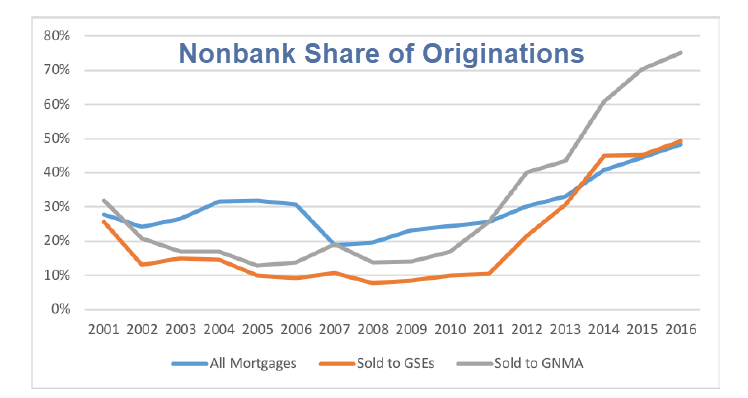

Nonbanks originated about half of all mortgages in 2016, and 75% of mortgages insured by the FHA or VA. Both shares are much higher than those observed at any point in the 2000s. We describe in this paper how nonbank mortgage companies are vulnerable to liquidity pressures in both their loan origination and servicing activities, and we document that this sector in aggregate appears to have minimal resources to bring to bear in a stress scenario. We show how these exact same liquidity issues unfolded during the financial crisis, leading to the failure of many nonbank companies, requests for government assistance, and harm to consumers. The extremely high share of nonbank lenders in FHA and VA lending suggests that nonbank failures could be quite costly to the government, but this issue has received very little attention in the housing-reform debate.

Nonbank Stress

There is now considerable stress on Ginnie Mae operations from their nonbank counterparties:

“. . .Today almost two thirds of Ginnie Mae guaranteed securities are issued by independent mortgage banks. And independent mortgage bankers are using some of the most sophisticated financial engineering that this industry has ever seen. We are also seeing greater dependence on credit lines, securitization involving multiple players, and more frequent trading of servicing rights and all of these things have created a new and challenging environment for Ginnie Mae. . . . In other words, the risk is a lot higher and business models of our issuers are a lot more complex. Add in sharply higher annual volumes, and these risks are amplified many times over. . . . Also, we have depended on sheer luck. Luck that the economy does not fall into recession and increase mortgage delinquencies. Luck that our independent mortgage bankers remain able to access their lines of credit. And luck that nothing critical falls through the cracks. . . ”

Nonbank Share in $Billions

GSEs and Ginnie Mae

Although both the GSEs and Ginnie Mae guarantee mortgage-backed securities, there are a number of essential differences. In particular, Ginnie Mae servicers are exposed to greater liquidity strains, and a greater risk of absorbing credit loss, than GSE servicers.

Guarantee and Issuance of Securities

Guarantee and issuance of securities Both the GSEs and Ginnie Mae provide a guarantee to their mortgage-backed securities (MBS) investors that they will receive their payments of interest and principal on time. One crucial difference between these institutions, though, is who issues the underlying securities. The GSEs purchase loans from mortgage originators and issue the securities themselves. For Ginnie Mae MBS, financial institutions originate or purchase mortgages and then issue securities through the Ginnie Mae platform. In both cases, the loans in the securities have to meet certain underwriting standards and other requirements. The GSEs set the standards for the loans in their pools. For Ginnie Mae pools, the standards are set by the government agency that provides the insurance or guarantee on the mortgage (Federal Housing Administration, Veterans’ Administration, Farm Service Agency, Rural Housing Service, or Office of Public and Indian Housing).

Insurance Against Credit Risk

Another crucial difference between the GSEs and Ginnie Mae is who bears the credit risk associated with mortgage default. As shown in figure 3, for loans in GSE pools, the mortgage borrower takes the initial credit loss (in the form of her equity in the house), followed by the private mortgage insurance (PMI) company (if the mortgage has PMI), and then the GSE. For loans in Ginnie Mae pools, the mortgage borrower is again in the first-loss position, followed by the government entity that guarantees or insures the loan. However, the Ginnie issuer/servicer — unlike in the GSE case — is expected to bear any credit losses that the government insurer does not cover. Ginnie Mae covers credit losses only when the corporate resources of the issuer/servicer are exhausted.

Loss Priority

Servicing Strains

Figure 12 shows the share of all mortgages in 2016 that were originated by nonbanks and insured by the FHA or VA.

Servicers with heavy concentrations may be more vulnerable to servicing-advance strains.

Consequences of a Nonbank Mortgage Company Failure

In the event of a failure of a nonbank mortgage company, there are three main types of parties who would bear losses: (1) consumers; (2) the U.S. government and, by extension, taxpayers; (3) the nonbanks, their shareholders, and their creditors.

If nonbank failure resulted in a reduction in mortgage origination capacity, it is not clear that other financial institutions would extend credit on the same terms to these borrowers, or perhaps even extend credit at all. This contraction in mortgage credit availability has the potential to be a significant drag on house prices.

Mish Comments

The Brookings article is 68 pages long. The above snips capture the essence of their liquidity crisis claim but they provide much more detail.

Shocks Coming

Nonbanks are vulnerable to macroeconomic shocks, rising interest rates, home price declines and job losses, often with a bare minimum down payment.

This is happening while debt-to-income DTI ratios are on the rise and median FICO scores are dropping.

This is hardly surprising given homes are not affordable.

Failure is a Given

Brookings provides the failure hierarchy, and failure is a given.

To keep the latest bubble going, nonbanks kept lowering and lowering credit standards as home prices kept rising and rising.

This is a recipe for disaster, and disaster is at hand.

Housing Collapse Coming

Four days ago, before I saw the Brookings article, I commented Housing Collapse Coming Right Up.

The Brookings article reinforces my opinion.

Meanwhile, overdue debt is at a seven-year high. Distressed debt surged 11.5% in the fourth quarter.

The Financial Times also notes “More Americans are also falling behind on their mortgages, for which problematic debt levels rose 5.2 percent over the same period to $56.7 billion.”

Deflationary Debt Trap Setup

These numbers are huge deflationary. When credit expands there is inflation. When credit contracts (think defaults, bankruptcies, mortgage walk-away events), debt deflation occurs.

Here’s my definition of inflation: An increase in money supply and credit, with credit marked to market.

Deflation is the opposite: A decrease in money supply and credit, with credit marked to market.

Looking Ahead

- Credit card delinquencies are priced as if they will be paid back. They won’t.

- As soon as recession hits, defaults and charge-offs will mount. In turn, this will reduce the amounts banks will be willing to lend.

- Subprime corporations who had been borrowing money quarter after quarter will find they are priced out of the market, unable to roll over their debt.

In a fiat credit-based global setup, this is how the real world works.

Unanimous Opinions

Seldom are opinions nearly unanimous. This is one of those times. Nearly everyone is looking for “inflation”.

We have it! It’s in home prices, junk bond prices, and equity prices.

The equity bubble is about to burst. For discussion, please see Sucker Traps and the Arithmetic of Risk.

Rear View Mirror Inflation

We have so much inflation that Inflation is in the Rear-View Mirror.

The inflation economists expect to happen, already has happened, in stocks, in home prices, in junk bonds.

They don’t see it because they do not understand what inflation really is.

Debt Deflation Coming Up

I expect another round of asset-based deflation with consumer prices and US treasury yields to follow.

Mike “Mish” Shedlock

Mish. I heard you speak on a podcast about this article and I believe you said (I could be wrong) that the ‘non-banks’ have been doing ‘liar loans’. If that is true, do you know for how long and what percentage of their total loans are ‘liar loans’?

With all the said though, it is TRUE that a MUCH higher % of mortgages today are Gov’t backed. Far higher then in a looooong time. So the US Gov’t is more at risk. There is basically almost no private label mortgage market. It was decimated in 2008 and has not come back. Dodd Frank has been a big deterrent to non-Gov’t lending. I think 90-95% of all mortgages originatedtoday are fannie, freddie, fha or va. Jumbo high end loans though are still private label non Gov’t backed.

I would say its great to be an optimist in life in general. But when it comes to investing and your life savings I think you need a hefty dose of skepticism and pessimism.

I would not agree that mortgage lenders are lowering their standards much. Maybe a little. Mortgages are still waaaaaaaaay more difficult to get today then they were then say between 1980’s to 2008. Average fico scores are still much higher then the past. There is basically still almost no real subprime lending market in existence. Even in the 1980’s and 1990’s there was subprime lending and option ARM’s. None of that today. FHA & VA loans are pretty tightly underwritten. Very little mortgage equity withdrawal going on as well. Appraisals are more stringent then pre-2008. Low 30 year fixed fully amortized loans (very little interest only…means borrowers building equity every payment). The housing supply across the USA is also very low and they built FAR less new homes this time then prior recoveries.

“Seldom are opinions nearly unanimous. This is one of those times. Nearly everyone is looking for “inflation”. We have it! It’s in home prices, junk bond prices, and equity prices.” ——–> you forgot inflation in rent and health care. Inflation in rent has been near “hyperinflation” in places like CA, Portland, Seattle……

This is interesting… 30yr mortgage has gone up .2% y/y while 1yr LIBOR has gone up .7%. It seems to me the stress will start in the ARM financed mortgages in particular the subprime mortgages where around 80% are linked to LIBOR.

if you are fixed rate hard to see the problem. raising mortgage rates put the post W2 generation into the sweet spot, rising wages, fixed mortgage payments. bankers were begging threatening mortgage consumers. (they got their revenge) . for sellers it opens the door to carrying the note yourself at a lower rate. of course construction is probably the main US industry and higher mortgage rates hurt new buyers, and they killed energy with higher rates, and now housing.

Meanwhile, LIBOR keeps moving up indicating bank liquidity is drying up. Considering most US mortgages are priced off LIBOR I can see further pain as rates go up.

Hmh. I would agree, but having the most extreme, unconventional monetary policies in remembered history give me some pause. And that includes times of war.

“Here’s my definition of inflation: An increase in money supply and credit, with credit marked to market.” So simple, yet so difficult to grasp for the boys whose job description starts with “Central”.

Realist, I’m in the same boat as you in regards to living life to be enjoyed not feared. I keep up with Mish and other sites that are contrarian just so I can have a balanced look on economics. In my 52 years of existence, I have learned that economies run in cycles, they never go in one direction. We have had a good 10 year run, I’m expecting a recession soon, such is life. In my 30+ years of investing and saving I have learned to play by the rules the markets assign and not fight it. It has provide well for me and my family. Life is good!

You: ponder this here image every night before you go to sleep.

link to s3-us-west-2.amazonaws.com

But, yeah, I mean, Keynes (the guy who said more debt is the answer) did say we’re all dead in the long run. Let not the ruin of tomorrow ruin today.

I wonder if there is any connection between this phenomenon and the recent Senate vote on loosening regulations: link to washingtonexaminer.com

And we know Greenspan is the god of economics so we must follow!

This was a very good article but I doubt many people see anything bad coming. I had also thought of a stagflation scenario (I remember the 70’s) but now believe it will be full on deflation. It should not be too long now before we know. Trump is moving on tariffs with extremely poor timing. We may start calling tent cities Trumpvilles.

Wrong again Mish. Shadow banking is good for economic growth and mitigates financial crises. Alan Greenspan said so back in 1999.

link to federalreserve.gov

You are wrong to insinuate that nonbanks are responsible for intermediately fuelling another even more reckless housing bubble whilst the banks were this time around too shy to directly fuel it themselves. Nonbanks facilitate the MANAGEMENT of risk – not the taking of risks.

Alan. Greenspan. Said. So.

anything for the sake of “national defense”

What would a Plunge Protection Team look like under Trump? Yikes!!!

Great Article. I’m in Canada and our housing bubble is starting to pop. Likely a recession on the way here and maybe in the US as well. Time to clean up the portfolio and ensure I only own what I want to own during a bear market.

Absolutely spot-on. And BTW, when was the last time the Fed didn’t tighten right into a recession? I’m sorry, but I’ve only been following financial markets for 30+ years, so I can’t answer that question.