The Residential Construction Report stats record the the greatest month-over-month decline in the history of the stats. The housing data dates to 1959.

Starts vs Econoday Consensus

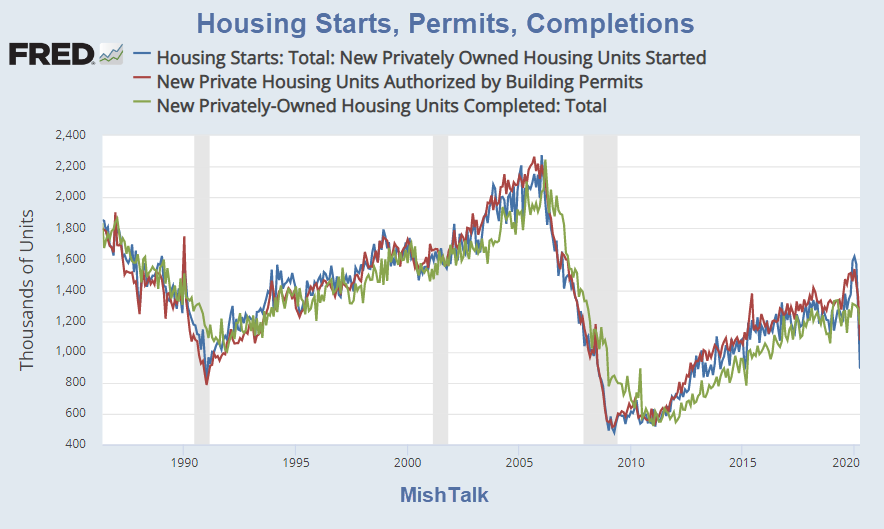

- Starts: 0.891 Million Seasonally Adjusted Annualized

- Consensus Starts: 0.968 Million

Permits vs Econoday Consensus

- Permits: 1.074 Million Seasonally Adjusted Annualized

- Consensus Permits: 1.033 Million

Housing Starts, Permits, Completions Month-Over-Month Comparisons

A data download from Fred shows the next biggest month-over-month declines were 26.4% in March of 1984, and 26.2% in March of 1960.

The Econoday consensus was

Housing Starts, Permits, Completions Year-Over-Year Comparisons

Year-Over-Year declines are not as large as in the Great Recession.

A data download from Fred shows the next biggest year-over-year declines were 54.8% in January of 2009, 52.8% in April of 2009, and 50.6% May of 1980. iand 26.2% in March of 1960.

Mish

Did you misinterpret your own article. This is “housing starts”. Means less homes are being built, means less supply. There is going to be a huge shift In buying patterns. NYC is going to suffer but suburbs will pick up. There will be changes in how people live and work that will take years to sort out. Housing prices nationally are not going down. Some areas will prosper and some will not. There is a pent up surge in demand coming and people would rather own a home than rent post crisis. If you could afford a home before the crisis chances are you can afford one now. Things aren’t that bad yet.

The Press Enterprise in Riverside, CA had a story yesterday on home sales dropping 31.5% locally. Yet the prices have increased, and in the comments section on FB all the comments are about how busy the people that are involved in the market are. Bottom line: people have to live somewhere, it’s better to buy than rent, and I don’t see a prolonged retraction in prices. I may be so bold to theorize, that someday the Gov will directly and outright finance mortgages itself if it needs to keep the market propped up. And I don’t mean the current FHA/Fannie/Freddie paradigm, I’m talking a flat out corner store like a bank.

“I may be so bold to theorize, that someday the Gov will directly and outright finance mortgages itself if it needs to keep the market propped up.”

…

Will never happen. Wall Street loves current set up. Make loan —> skim off the top —> off load to GSEs.

Why would Wall Street EVER give up honey pot?

These numbers are not surprising given the economy was effectively stopped dead in it’s tracks. Again, a lot of these numbers aren’t as meaningful when given the context under which they happen. I think by late summer, we will realize that even with economic activity picking up, the virus isn’t as bad as we had initially thought. My gut still tells me by the end of summer we will see major improvement and a waning phase in the damage Covid-19 is doing. Oddly there is very little explanation as to why some get so sick and others don’t. Today we learned that the people contracting it again weren’t actually positive but just shedding dead virus. This is good news because it will improve herd immunity by itself. Most vaccines are a dead virus. If the dead virus is shed enough to the public , then you will get herd immunity more quickly.

Lets see how things look in the first week of June to see if there is a path forward. NC is supposed to make a decision on phase 2 of opening up over the next day or 2. Their numbers look pretty crappy link to covid19.ncdhhs.gov

My business supporting is supporting construction, Vinyl Windows. We had 35% YOY dip in April and this month is right to where we were last year. I mentioned in my comment at earliest posts. It is lies, big lies and statistics. Good luck believing it!

This is an indication of what’s to come. It truly is difficult to wrap your mind around what is happening and how this plays out. So many spinning plates in a slow motion disaster. We’re only a few months into this.

Short of a complete government takeover/bailout of the real estate market ( ain’t gonna happen ) this is gonna hurt like we can’t even imagine. And thats just 1 spinning plate!

How are these mortgage’s going to get paid if people and business’s aren’t paying their rent or mortgage? This situation isn’t going to change in 6 or 12 months. Does this go on for 3,5,7 years?

There’s a guy down the street that is/was building a giant 4+k sqf house, they were going like crazy even during the height of the lockdown, no activity AT ALL for the last 3/4 weeks. I saw him walking around the empty shell of a house with his wife and kids looking dejected the other day. I’m guessing he lost his funding. I heard he worked as a drywall guy.

There’s just no way this doesn’t end in a disaster. Think of the drop in tax revenue for local governments.. how are they gonna deal with 25% less for years?

You ain’t seen nothing yet…..

They had to stop making the high end cookie cutter garbage at some point. The real housing market (new owners of reasonably priced inventory) won’t miss this. We need to begin to address the real demand.

More than 50% the housing bubble recovery in the new construction segment has been erased. That is how strong the shock to the housing market COVID19 has been.

This could be temporary stay at home orders. States are allowing construction again. I know demand for housing remains strong in my region so I hope these numbers turn around very quickly.

I need to buy a car before July 8, and I watch craigslist for a supply glut, and followup price drop. I fear it’s going to be a bit too early, fall will be the buyer’s market.

I have a feeling there will be a Government program to sell ALL the “excess” cars to several giant investment corps for pennies on the dollar, on the condition that they have to sell them in Indonesia, Malaysia, Vietnam (you get my drift) at a STEEP discount, but still producing a hefty profit. The program will be done secretly, of course. That way the “value” of the 2022 vehicles stays intact. I’m only half kidding.

This article is about houses not cars.

LOok at hertz and other rental car agencies for your purchase. They are selling them under cost.

They are giving them away. I just rented a premium car for a week for $147. They are taking a loss at this point.

I was wrong. Too pessimistic at Dow 400K. It’s clear it will be Dow 500K. Fed will simply pay people’s mortgages. Or give them loans which will be forgiven if 80% of the amount is used for mortgages. Sort of a Fed Heloc.

People out of work don’t buy houses. Trapped AirBNB hosts and aging boomers will add to supply of existing homes.

We just had another lesson in leverage.

This is going to take a while.

“People out of work don’t buy houses.”

All they need is the Ownership Society Program 2.0. Fog a mirror, get a home loan.

I still believe you are underestimating the lengths they will go to this time.

Government sponsored 100 year mortgages at 0% would do the trick.

500k a year house could be gotten on McDonald’s wages.

I wish someone would give me a reason they will ever quit printing? Seems like nothing is out of bounds at this point.

Why stop there? government car loans, government creditors cards, government personal loans.

Mish I think you are completely overlooking the power of the printing press. Deflation can be avoided in any longer term capacity if you flood the system with direct to consumer money.

“Government sponsored 100 year mortgages at 0% would do the trick.”

I do wonder how that would play out.

But I’m not sure all the McDonald’s kiosks that will coming our way would buy a house even if they could.

I can’t predict an exact percentage of home price declines, but I hypothesize 5% to 20% over the next 9 months. However, I believe 2% 30 year mortgages are on the way and possible government support. Prices will be back at their pre-Covid levels sometime in 2022.

I don’t think it’ll happen that fast… last time was 5 years to the bottom, and 6 back to peak.

Last time was a subprime debt bomb, much worse. This will go quicker and heal quicker.

There was way more near-subprime shenanigans going on than they claim. My friend works as a smartphone seller in an AT&T store and somehow got approved for a mortgage last year. My jaw dropped when I found out.

I don’t think there is much difference between 2009 approvals and 2020 approvals.

I the number of approvals is the difference. There are other players that have taken that place now.