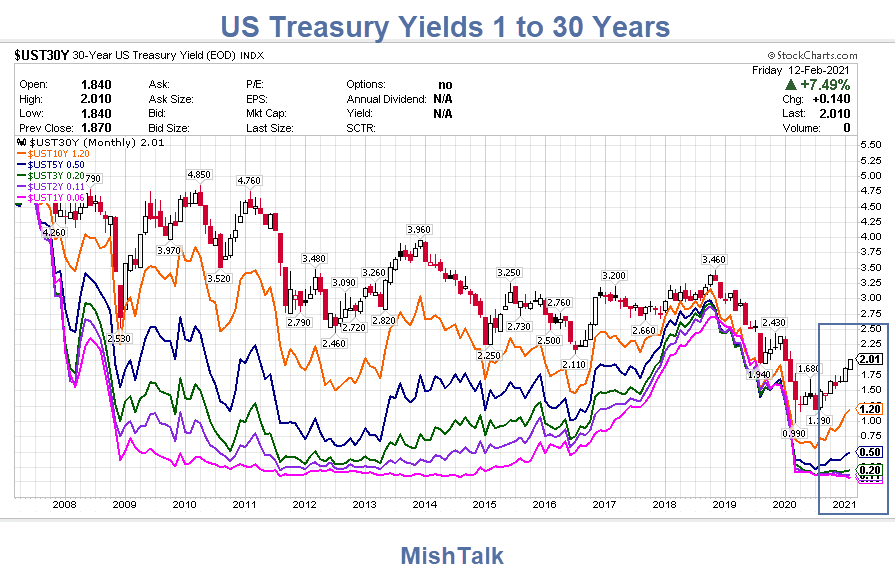

Yields Reveal a Mini-Revolt On the Long End

- 3-Month Yield: 0.04%

- 1-Year Yield: 0.06%

- 2-Year Yield: 0.11%

- 3-Year Yield: 0.20%

- 5-Year Yield: 0.50%

- 10-Year Yield: 1.20%

- 30-year Yield: 2.01%

US 30-year yield back to a 2-handle. Highest since Feb 19 (so a new post-pandemic high)

Among the developed markets, only the mighty 30-year Aussie has a higher yield. pic.twitter.com/VPYcOKaA7H

— Jim Bianco (@biancoresearch) February 12, 2021

Yield Curve Dramatically Steepens

Notes

- In July of 2018 the spread between the spreads was only 12 basis points with the 2-30 spread at 38 basis points and the 2-10 spread at 26 basis points.

- The 2-30 spread at 1.83 is higher than any time since February 10, 2017.

- The 2-10 spread at 1.07 is higher than any time since April 7, 2017.

Fed Losing Control of Long End

- On February 8, the Fed noted Monetary Policy Will Stay Accommodative For a Very Long Time. I commented “Like Forever”.

- On February 10, in a speech on the labor market Powell said the True Unemployment Rate is Actually 10%

In Powell’s speech, he reiterated the message rates would stay low.

But spreads have widened dramatically which begs the question:

How long before the Fed openly intervenes to push rates lower on the long end of the curve?

Mish

Test.

Screen Shot 2021-02-15 at 2.02.05 PM

Damn technology. That’s two. I give up.

I was just looking at the monthly on the 30 year…..and thinking the trend line says we get there by late summer…or a rate of 2.6 or so…..whichever come first….it will be interesting to see if they do something before the long term trend line gets broken.

Will the DOW stand at 40k by year end ? Wouldn ‘t be surprised ….The financial, CBs manipulated system has gone totally berserk, everything is possible now ! Put them all in, your chips, with interest rates going even lower , the only way for already overvalued assets is UP!

When Jim Bianco and Lyn Alden say inflation continuing to edge up is quite likely, I listen. On the other hand Dave Rosenberg sees no significant rising inflation in the details (free month of his service is nice, but $100/month to continue? sheesh).

Alden says she is neutral on gold for 6 months, but long-term bullish. And IF the Fed executes yield curve controls, resulting in real yields for 10-year treasuries to go down (they are bouncing around -1% right now, she says), gold could go on a tear.

Always the same number of sellers and buyers. Maybe they could say seller were more motivated than buyers, or vice versa

There basically is one buyer (Fed) and one seller (Treasury). Each is half of a single entity with multiple personality syndrome.

isn’t this a good thing since a steepening curve signals growth?

How long before, or since ?

(Courtesy trading economics)

Ever since the late 1700’s , there have been three 60+/-1 year interest rate cycles, with and without the FED. That alone says the FED is not in charge. The fourth interest rate cycle is 40 years along and has most likely formed a double bottom. The next 20 years will be part of an exponential trajectory for interest rates. Yields are so low, and budgets so tight there is little wiggle room to tolerate a doubling of interest rates. Most debtors will default. Those trying to sell anything to repay their debts will force market prices lower. The decrease in market value of the asset pledged as collateral will force bond prices even lower / interest rates UP. The tight rope act by today’s financial institutions will either blow up or fully expose the financial institutions as corrupt and fraudulent.

You are relying on the Fed to do the right thing. In response to massive defaults they will probably start buying more bonds, even junk bonds. I think that the Fed will invite inflation rather than risk defaults and deflation. It would be better to allow defaults (perhaps in a slightly controlled manner) and support people directly than to try to support people indirectly by propping up marginal (and worse) businesses.

Mish, the EWI guys have maintained for years that the Fed follows interest rate markets. I’d be interested to hear your take on that assertion.

I’m an EWI follower as well. They are spot on with macro social trends and global patterns of finance. The Ewaves are not always clear, even when they have completed a larger degree of trend.

I often wonder how fiat money can distort the waves in an equity market. As an engineer I’m going to do an advanced study using my signal processing skills to look at the internals of the markets for “shock” that would indicate the FED stepped in to support markets. Just by simple curve fitting, an exponential curve can be generated that correlates with a value greater than 0.80 to the Dow Jones Industrials since the Great Depression. The data set is a whopping 23000 points!!! That tells me markets are NOT random and NOT stable in the long term. Stability occurs during bear markets.

Markets are positive feedback systems, which by definition is unstable.

I concur with EWI’s premise markets are too big to be manipulated or supported for long, if at all. If something moves the direction it was supposed to, it’s only because it would’ve anyway.

My biggest laughs come from reading what market “experts” say is the “Reason of the Day” that supposedly explains why the market did whatever. I wish just once they’d say “the market went up because there were more buyers than sellers today!” Now THAT would be news (and correct)!

This is something that is obvious if you understand larger trends. Business investment in the US is historically low. That’s because software and tech require much less capital than manufacturing. And its getting lower as the low-hanging fruit of invention has been picked. This means the demand for money is low. On the other side of the equation, 40 years of tax cuts, big deficit spending, and deregulation has moved money into the upper regions of the wealthy, and they can’t spend it all. So the supply of money is at historic levels. Low demand and high supply means interest rates must be low.

The Fed’s real job is liquidity in the over night lending market, and making the yield curve positive. Both require that it follow the market. And the market rates are very low and will remain that way well into the future.

What impact on high yield (HYG) now sub 5%?

Where is it heading, why and when if current situation persists, long end yield rises further or long end pushed down?

I would bet shortly after the $2 trillion stimi bill is passed, the Fed will have to deal with the long end of the curve.

Manipulate is such a loaded word. Every action or advisory could probably be described as manipulation

I never understood the idea that the Fed has no control over long term rates. The 30 year rate is built on the term structure of rates and reflects an expectation of future short term rates. If the market believes the Fed will keep short term rates low for an extended period that has an impact. The Fed isn’t just any player either

The market believes the Fed will keep short term interest rates low but it doesn’t believe they should keep them as low. In fact the market believes they’ll keep them lower for much longer than they should do. Which poses inflationary risks and currency instability. Hence the positive yield curve or a more positive yield curve. The Fed can attempt to keep longer end yields down too but it’s more difficult. The further you go out along the curve the more stock there is. They’d have to buy everything out to however far they want to control. That in an environment when a lot more stock is also going to be issued. Of course they can keep issuing dollars to do so at the cost of much more debt and the flack they get for that. It doesn’t mean they won’t though.

Someone who’s more knowledgeable explain it better. But why does it really matter? Can the Treasury just perpetually issue short term debt instead and roll it over? I mean it has an unlimited buyer, the Fed.

Other new issues, corporate bonds etc are priced at margins over treasuries, so if treasury yields rise, so will the yields of new issues. That’ll mean existing secondary market bond yields would look more expensive against new issues, and perhaps cause selling pressure etc etc.

The idea that as treasury yields rise, so will the yields of new issues would be correct if the situation was stable and treasury yields were driven by inflationary concerns. However, we are going into a period of substantially rising corporate defaults and it seems that the yields of new issues during a general all encompassing fairly dramatic increase in defaults would push treasury yields down i.e. the push is the other way round. I mean there is going to be a flight to treasuries. For all that the Fed are credibly commiting to reflating the economy, it could not be more clear that the main risk is still von Mises style deflation which must be why they pressed the nuke button (or maybe shouting broken arrow down the radio for a naval bombardment on your own position might be more appropriate).

Here is an interesting article that suggests we are heading into a high level of default (as i suppose might reasonably be expected anyway)

Perpetually yes. The more people save and keep their savings inside of the banks, the slower the velocity of circulation. I.e., banks don’t lend deposits. Deposits are the result of lending. So all bank-held savings are frozen – much like Japan.

The curve from 5 years out looks odd to me. You can pick up 70bp extending 5 years from 5 to to years, but you only pick up 81bp extending 20 years from 10 years to 30 years? Either the 30 year is expensive or the 10 year is cheap, or a bit of both.

Sounds like a good time to short financials.

Inflation picks up, Fed has no option but to pursue yield control and subsequently force financial institutions to buy treasuries (cos who else will at that point). Not a good outlook for Financials.

A rising spread-curve mans the market is predicting a better economic conditions in the future. Why would Fed try to suppress it? Debts do not matter as the US never has the intention to pay them back.

Or inflation.

My bet is inflation

I agree.

As soon as they can. The Fed speakers have been consistent on the policy. We may not like it but it is what it is.

“it is what it is.”

You mean vicious oligarchic vulture capitalism for the rich ? Thanks Jay and Janet…