Please consider taking a $45,000 Loan for a $27,000 Ride.

Consumers, salespeople and lenders are treating cars a lot like houses during the last financial crisis: by piling on debt to such a degree that it often exceeds the car’s value. This phenomenon—referred to as negative equity, or being underwater—can leave car owners trapped.

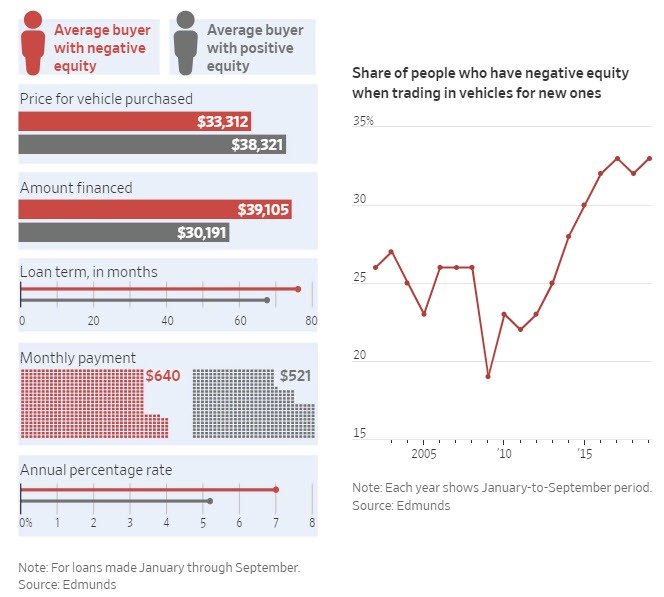

Some 33% of people who traded in cars to buy new ones in the first nine months of 2019 had negative equity, compared with 28% five years ago and 19% a decade ago, according to car-shopping site Edmunds.

Easy lending standards are perpetuating the cycle, with lenders routinely making car loans with low or no down payments that can last seven years or longer.

Borrowers are responsible for paying their remaining debt even after they get rid of the vehicle tied to it. When subsequently buying another car, they can roll this old debt into a new loan. The lender that originates the new loan typically pays off the old lender, and the consumer then owes the balance from both cars to the new lender. The transactions are often encouraged by dealerships, which now make more money on arranging financing than on selling cars.

“These aren’t Rolls-Royces,” said David Goldsmith, a lawyer who defends consumers in auto cases. “They’re Ford Escapes.”

Some 5.2% of outstanding securitized subprime auto-loan balances were at least 60 days past due on a rolling 12-month average during the period ending in June, up from 4.8% the year before and 4.9% two years before, according to Fitch Ratings.

Examples to Consider

The Journal cited the case of Mr. John Schricker who kept rolling over loans to the point that it took a $45,000 loan from Ally Financial Inc. to buy a $27,000 Jeep Cherokee.

Also consider the case of Yolanda Finley. She bought a bought a used 2011 Chevy Traverse with a loan of $25,585 from Santander Consumer USA Holdings Inc. in 2014. Finley could not afford the payment. Her car was repossessed. She now owes $27,000 on a car she does not even have.

Nicole-Malia Tennent and Shyanne Fernandez, both in their early 20s, wanted to trade in the car they shared for something less expensive last year. Instead they splurged on a new 2018 GMC Sierra truck, moving the unpaid loan balance of $12,500 into a new loan. The new loan balance is over $66,000. The old loan payment was $500. The new loan payment (I presume for longer), is $900.

What the hell do two friends need a $66,000 truck for? How will they allot the time between them?

This is how crazy it’s gotten.

Three personal anecdotes don’t constitute data but other evidence suggests the problem is widespread.

Car Dealers Make More Profit On Loans Than Selling Cars

A third of auto loans in 2019 had a term period over six years. People cannot afford the cars they are buying.

For discussion, please see Car Dealers Make More Profit On Loans Than Selling Cars

Families Go Deep in Debt to Stay Middle Class

On September 9, I noted Families Go Deep in Debt to Stay Middle Class: Revolving Credit Jumps 11.2%

These are all signs of a “Late Stage Credit Bubble“

Ability to buy things one cannot really afford does not make or keep someone in the “middle class“.

Wages are not keeping up with needs and desires.

Collectively, these reports show a late stage credit bubble the Fed desperately wants to keep inflating.

Mike “Mish” Shedlock

It is terrible. That’s why I don’t use such credits from banks. These conditions are really crazy. Sometimes I can get online loan with low interest rate from link to cashwagon.ph for some emergency expenses, but I always return money in time!

I used to think people who purchased way beyond their means would get in trouble, and those who saved would do better in the long run. But what I have seen is that when you have enough badly behaving people, their political clout increases, and the government bails out the bad actors on the backs of the good actors. Theoretically, it can’t go on forever. In practice, it is likely to go on longer than I will live (but I’m thinking my life expectancy is short.)

So I really have no idea how this is going to play out.

This is what happens when the “stock market” becomes the de facto health of the economy. Delaying the business cycle, propping up company profits to maintain a “healthy” market. The car cycle has been artificially maintained to the point we have to shift technologies (gas to electric) to maintain the illusion.

What’s going to happen to all those vehicles when the repossession bonanza goes into high gear?

Picture a child in a candy store that extends credit … that pretty much sums it up for many people.

I don’t understand, don’t you have car leasing in the US? I mean you lease a car for 5 years and at the end you return the car and walk away. Why would anyone take the residual risk on a vehicle? Buy the insurance, and lease a car! sure its probably a few dollars more but the implicit insurance of “returning the car at the end of the lease” is worth it, and doesn’t give rise to this kind of insanity.

It could be that all these people have such terrible credit that they cannot afford to “lease a car” and then the issue is why would anyone lend to these people?

Cars last a long time compared to eras past. This is why car manufacturers turned to technology features to sell new cars.

Working at CDOT in the 80’s we were discussing the housing boom in Colorado due to a spike in oil prices. I argued it was all about financing, but our auditor (from Kansas oil), said financing didn’t matter. I said why? He said “People will just pay cash for their houses if they can’t get financing.” I said: “Who can do that?” He said: “All my friends can.”

That’s the sort of insular thinking that helped propel us to where we are today.

I lived in CO for about 15 years and watched things get wacky there after the 2008 crisis. Around that time, my ex wife and I got a nice apartment, 2 bed/2 bath, a few blocks off I-25 in a nice area (south Denver) for $900/mo! The bedrooms were spacious too, I converted the spare into a billiard room, had an 8 foot pool table in there.

Today, that place must be well over 2K a month easily.

A decent tent from Tents.com costs what, $200? Big deal!

When it comes to lending, there are really only two positions. One is that everyone should have access to loans. That position has consequences, those being that, in order to make lenders willing to lend to the non-credit worthy, debtors must have no easy means to escape paying. At the other extreme, you can have a system where bankruptcy can allow people in over their heads to get out. The consequences of that are that lenders are unwilling to lend to risky borrowers, and only the most credit worthy people can borrow.

Whichever system you have, people will complain. We used to have the latter system, and Chapter 7 was easy, and you could even get out of student loans. The consequence was that the poor had no easy way to get loans, and when they did, the interest rates were high. As far as education, anyone with high academic qualifications could get a scholarship, if needed, but marginal students could otherwise only go to college if they could afford to pay. Colleges had to be fiscally prudent in order to keep tuition as affordable as possible, so that they could get enough students.

Now we have gone the other way. Lower income people have much more access to loans, and at much more competitive interest rates, but can’t get out of them. Anyone can go to college now, so long as they are willing to sign the papers obligating them to a lifetime of debt. Colleges have gone on a huge building boom, building tons of modern, new buildings, and increased salaries dramatically, and tuition has skyrocketed, since there is no longer a need to keep it affordable.

Which system is better? You decide. However, if you decide that we should have a system where everyone can borrow money easily at low rates, but then get out of it easily if it becomes challenging to repay, you are living in dreamland. That isn’t a possible choice.

I would add that, regardless of which system we have, people love to view bankers as evil. Consider the move “It’s a wonderful life”, where the banker was evil because he wouldn’t lend to the common man, trapping them paying rent forever. If you re-made that movie today, Jimmie Stewart would be the evil one, with his predatory lending practices, lending to the poor who couldn’t afford it, trapping them in a lifetime of mortgage payments. Heck, Stewart would have probably loaned them money to buy cars, too, evil as he was.

The trouble with what you write@Carl_R is that you are using what used to be called common sense. It has left the building.

When Jimmy Stewart made “Its a Wonderful Life”, high schools taught reading, writing and arithmetic.

Today, the schools teach transgender equality, safe spaces and participation trophies. And the supremacy of municipal unions over education.

Jimmy Stewart would be public enemy number one. Too much practical sense, not enough entitlement thinking.

The reason people will always view bankers as evil is easy . They are simply middlemen who produce nothing tangible or of value and function because of the system. The same is true of insurance and real estate professionals. Likewise with lawyers. Increasingly though even engineers have gone into high finance in order to get rich fast. Sadly the system wont change until it collapses but we likely have debt monetization after we go through ZIRP and NIRP. When the you owe the bank $100,000 they own you but when you owe the bank $100,000,000 then you own the bank.

If bankers aren’t providing any service/product that you feel is useful, then why aren’t you smart enough to go around them?

Either they DO provide something you can’t do on your own, or you are just a glutton for punishment.

If you could do math and could control your urges to spend money you don’t have, you wouldn’t need a banker to do it for you

Your an idiot bob. I’m rich enough to never need a banker. Bankers are screwing the system for people who arent as fortunate.

I’m an engineer so I do something productive. Banking isnt an inherently productive line of work. Even people in banking admit this.

California boy — you say you are from Texas, but you don’t have the “can do” attitude of a Texan. You have the whiny, perpetual victim-hood attitude of a California social justice warrior.

You now say you are an engineer, but if you were you would go build a better mousetrap instead of demanding the government pass a law making mousetraps an entitlement. You don’t act like an engineer, you act like a spoiled, entitled social justice warrior.

And you claim to have so much money that you don’t need a banker, but you have lots of banker friends who laugh at your whining because they know good and well you need them and their services to keep living beyond your means.

Go ahead, start your own bank and show ’em! Its easy, even a social justice warrior like you can do it! Show us that Texas “can do” attitude that you don’t have, create your own bank, and give away your money to all those other whiny humanities majors writing complaints at Starbucks. Don’t tell actual engineers that we are wrong, SHOW US.

You are all talk. Or more to the point, you are all whining whimpering nonsense. Put up or shut up. Start your own bank and give away your money for free

Money is already being given away for free bob. Are you so poor you have to pay interest ?

Whine all you want, there is no free lunch. You are not entitled to the work of others for free — that is just the thinking that transformed California into the 3rd world sh!t hole it now is.

Tell us when you have your credit union started, or shut up.

“You are not entitled to the work of others for free”

I earned the zero percent rates you boob. The truth is it doesnt exactly take a whole lot of. creativity or work to buy short and lend long. This is what I meant but it clearly went over your head . The banking industry is still bloated despite how much technology continues to replace workers.

Actually, Casual, that’s not true. Bankers do serve a function of value. Yes, they are a middleman, but they are much more efficient than the middlemen of the past. In days of yore, the farmer in India grew tea, and sold it to a middleman. The middleman sold it to the sailing Captain, who transported it to the country where it would be consumed, who sold it to yet another middleman, who sold it to a processor, who sold it shops, and eventually it ended up in the hands of a consumer.

In the old system, what fraction of the price that the consumer paid got to the original producer? Very, very little. By contrast, in today’s market, the farmer can sell his crop directly into the futures market, at a time of his choosing, and he gets a much, much higher percentage of the final price. The same it true for miners, and other producers.

Yes, bankers are middlemen, but they are far more efficient than the older systems, and because of that, have contributed a great deal to the prosperity of the country.

We could have the same debate regarding insurance, real estate professionals, and lawyers. In some sense they are simply middlemen that leech on the system, but at the same time, they keep the economy flowing. Remove them from the system, and the system breaks down.

Sure, we could go back to the system where we all grow our own food, and we all build our own home, and ride a horse we grew. Then no one would “leech” off our production, and we would have the full benefit of everything we produce. We would also be a lot worse off.

Btw, I’m also and engineer, and not a banker. Yet, I do understand the economy well enough to see how much more efficient the economy is today than it was even 40 years ago.

Jimmy Stewart explained all this banking stuff decades ago (Its a Wonderful Life) in a language people with a high school math background could understand…. but socialists don’t like math and think they are entitled to free sh!t.

Their demand for free sh!t defines them. Its why I don’t believe@Casual_Observer is really from Texas — the Texans I know believe in hard work and getting compensated for it. A belief in something for nothing is a California thing and a 3rd world thing; its a mental sickness

I believe in smart work Bob. If your working so hard that you don’t have a life it kind of defeats the purpose of life.

It would be idiocy to compete in a banking world that is at or

headed to ZIRP and NIRP. I am entitled to zero interest rates because my credit score makes it so Bob. Even someone who lives on the side of a mountain from NY should understand this. Comparing credit unions to banks is apples and oranges. Credit unions are not subject to some regulations that traditional banks are which is why you’ve seen an explosion of credit unions. It is another thorn in the side of traditional banks that they’ve been complaining about for years.

So we should not hold our breath for the@Casual_Observer Credit Union? You think the bankers are useless, so your credit union will do the work for free?!?!? And you will grant loans to your fellow Californians who have neither the means nor the intention to pay the loans back?

Yup, I thought so

Being critical of something doesnt necessitate starting a business in it Bob. This is probably why your family failed in the restaurant business.

Of course bankers provide some value for scaling. But in the post financial crisis world, banking has turned into a bifurcated system. The banks that help small and medium businesses are still providing good value. The problem is money center banks tied directly to the Fed. The banking system is essentially a government function in the current system we have. The economy is not nearly as efficient and it could be as since 2000 a large percentage of the economy has been dedicated to non-productive growth due to financial services, insurance, real estate etc being a bigger chunk of GDP while productivity growth has lagged.

Look at what the so-called “leaders” are doing at the state level, its not hard to see the citizenry just following the leaders (or maybe other way around?)

The poop for brains in California just approved a $3.2 BILLION municipal bond issue to fund Richard Branson building a train from outside LA to Vegas (where Branson, a multi billionaire, owns the Hard Rock Casino/Hotel). Why doesn’t Branson pay for his own train? Why don’t the casinos in Vegas pay for a train together, so all the math challenged Californians can lose their money gambling? BECAUSE, the people of California are extra stupid and will pay for both.

On top of the “high speed” (which can’t get up to speed on such a short track) train from the middle of nowhere San Bernadino to the middle of nowhere else…

The morons are now going to pay Branson to build a train from the middle of nowhere outside LA, to Branson’s casino in Vegas. Maybe it never gets finished (like the other high speed disasters), and CA spends $3.2 billion to dig a trench — or just maybe they pay to send more customers to Vegas to lose their money at the tables. Its too stupid and pointless to even be labeled “fiscal stimulus”.

California has become a 3rd world country, with a 3rd world education system and voters who can’t balance a checkbook. Basic addition and subtraction eludes them. They actually believe they can get something for nothing.

Is it any wonder they are befuddled by a seven year car loan on a machine that devalues in only five years? None of these participation trophy winners knows the first thing about car maintenance, so after years of neglect the cars are pretty much garbage in practical terms, not just depreciation terms. Changing the oil and inflating tires are white privilege according to college indoctrination staff.

Despite the highest taxes in the country, California is in debt, has the highest income inequality, rampant homelessness, poverty, garbage uncollected, rats and medieval diseases, used syringes and human feces all over their cities. And they keep voting for the likes of Maxine Waters, Adam Schiff and Nancy Pelosi (and Gov Moonbeam isn’t extreme left wing enough for them). They leave dry kindling underneath neglected high tension power lines, and then wonder how forest fires start…. well lets be honest and mention some fires were started by a California college grad dropping their lit marijuana joint into the kindling.

The hillbillies, allegedly not that bright, know how to change their oil. The allegedly educated Californians have absolutely no clue. Time to update our stereotypes

Wow the place you live must really suck to have this burning desire to pull down California to your level. California is the place just about everybody else in the World wants to live in.

Let me guess, you live in some flat, square state with crap weather and no rural medical coverage, a crap economy, and nothing interesting happening at all.

Not sure what you have against Texas, but I don’t live there so I will let actual Texans defend their state. Something tells me they are busy putting up signs telling Californians to stay the hell out.

I used to live in New York City, and my family used to own a restaurant in the ‘burbs of NYC. The smart money moved to Florida (along with my parents), which meant lower spending clientele for the restaurant. A restaurant that held my parents in good staid could not support 4 kids and our spouses, even if the big spenders hadn’t moved south.

This is really advanced math, so pay attention and maybe you can explain it in stupid talk to@Casual_Observer … if you take the same (or less) revenue that supported one couple (my parents) and try to divide it among four couples (my siblings and our spouses)…. everyone gets a much smaller amount. And since my siblings can do math, we don’t live beyond our means like Californians.

My brother ran the restaurant until Obamacare made it impossible. I went into a different field, did well, and then moved south with the rest of the smart money. I live on the side of a mountain with an amazing view. The nearest metropolis is a half hour away, easy travel in locale with functioning roads (no traffic jams!). My taxes are higher than Florida, but I get much better value for my tax dollar so I am happy.

I will not tell you my location because I don’t want a$$holes from California moving here. If anyone asks, my county is terrible with terrible weather and terrible everything else — stay away

Your PARENTS had to support you and your spouses? No wonder they and you had to move.

Yes genius. My parents raised four kids. They did not depend on welfare like California. They taught us math, so we knew the family restaurant could not support four couples once we grew to adults.

I am not surprised this concept eludes your math skills. You moved into California, so we all know you are not too bright

Sounds like I hit the target dead on Bob – not only do you have to pull down California obsessively but you are too embarrassed to even mention the state you live in. You must really hate that you are stuck there can’t afford to live somewhere nice.

At this point, Bob will point to drug addicts in SF and equate the whole of CA to one 6×6 block area of one of the smaller cities, LOL. You’d hate it here Bob, we understand science, respect people, and are rich and warm – even in November it is a sunny 80 degrees today. How’s your weather?

Yes, my state is horrible and no one from California should even think of coming here.

Bad weather. You are expected to work. Limited entitlements. Electrical power generation plants IN STATE. Limited public employee pensions, but they are fully funded. In short, its everything Californians hate.

Bob, I’m sure I’d like your state, but even if I didn’t, I wouldn’t obsessively try to pull it down. I just wouldn’t care. What is it that makes you consumed with hatred for California – could it be you are jealous of our lifestyles – where I live most people are rich, warm, and happy. I just went downtown and everybody was out shopping in shorts and t-shirts – the only downside was an excessively busy Apple Store (I know, the hardships we have to bear here in CA), but I can go tomorrow and it will be quiet.

Bob lives somewhere in the south (but not as far south as Florida) and he was forced out of New York as his parents couldn’t afford to live there anymore and support their 4 kids and their wives. They tried to do this in the highly competitive restaurant business. Bob blames government, unions and immigrants for his lot in life. He had trouble adjusting to living in the south but given he is a white person it probably never should have been that difficult. Bob misses New York but his anger knows no bounds. Bob probably lives somewhere near the Tri-cities area but it really doesnt matter. Bob is angry and will never be happy anywhere.

I live somewhere south of NY but not in FL… everything else@Casual_Observer wrote he made up. Good parents raise their kids, and then retire. My parents did not support any of their four kids once we were adults — that is just @Casual_Observer ‘s piss poor reading comprehension skills, which are apparently as bad as his math skills.

I left NYC after a very successful career, and started a 2nd business in my new location — and I still don’t want socialists like@Casual_Observer moving here, especially now that I know he can’t read and also can’t do math.

You make no sense bob. You said you moved because it was lower cost. You sound like a cheap banker. That would explain why you got offended when I insulted them. Either way living on the side of a mountain in Tennessee means you’ve arrived somewhere. Congratulations.

I don’t live in TN either. I would suggest you move there to avoid the consequences of your dumb voting, but I don’t want to offend people in TN. They don’t deserve to suffer your foolishness

I pointed out how spineless and stupid your banker comments are. If you were half the man you think you are, start your own bank and show them how its done! You can’t, because you don’t have the math skills to be a banker. You also demonstrated poor reading comprehension skills.

I continue to hope you stay in California and suffer the results of your own voting decisions. Even if you visited, you don’t have the can-do attitude of a Texan, and that probably factors in to why you had to move to a sissy state like CA.

California is economically over $1T more GDP then the state of Texas. And yet Texas lets 2 voters determine their bonds. No one really even knows what the bonds do in Texas’ case.

Your so-called trillion dollar economy just reflects a lot more inflation and a much higher cost of living…. The smart money figured this out already, which is why they sold their houses to morons like you.

Same reason Mish sold his Chicago sh!t hole to a different math challenged moron so he can move to Utah

Idiot. California is a large state with both high and low cost regions. We have a flood of people from the coast moving to our region for the very facts you state just like other states. We bought at the bottom of the cycle and debt is not an issue. Not everyone is like you who couldn’t make it in NYC and had to move to a low cost poorer region of the country.

And ironically the region Mish is moving to has an index of 102. The region I live in had an index of 95 when I moved here. Even at a higher index now it continues to draw people with money who can afford to live here. The black money from China has helped California boom. Someone is buying that real estate on the coast but it’s not Americans.

I don’t make important decisions based on some newspaper cost of living index. If the newspapers had a clue about business or math, they would have figured out the newspaper business loses money. Advertisers left the papers and went to Google, and they are not coming back. Only an idiot would take financial advice from a newspaper.

I don’t know if your 102 index is correct, but I’m guessing the correct number (whatever it might be) is less than what Mish pays in Chicago. Mish likes taking photos of national parks — there are many in Utah, and nothing but concrete in Chicago. So the move might make sense for him…. depending on how he adapts to Mormonism. We can all place our bets on the Mormons, but ultimately he will save money versus Chicago and more of his money will go toward photos and less into corrupt taxes.

California is still a 3rd world sh!t hole either way!!

Of course it’s less than Chicago.Chicago is the worst of all worlds. It acts like the coasts but has no underlying economy. Utah is a nice state but St George is getting as expensive as Sedona or some places in Calfiornia.

I am sorry your parents abandoned you and left you to fend for yourself as a child. The USA used to be better than that, back before socialism took hold. You shouldn’t have had a 3rd world childhood.

But you apparently did, and you got a 3rd world math education to match. I don’t want to spend time explaining basic addition and subtraction to you, and this divide by four thing is way over your head.

Come back and debate after you learn basic math.

Thankfully my parents provided me with enough to support them. Parents supporting children and their spouse would be a drag. I feel bad for your parents Bob. You were a burden.

I think most readers of this blog, outside of California anyways, understand that a restaurant that supports one family (my parents and their children) would have trouble supporting four families (the now adult children, their spouses and next generation children). Four families need more revenue than one family…. seems obvious.

Then again, if Californians could do simple math their state wouldn’t be buried in debt that they cannot pay. Its no surprise that a group that can’t do addition and subtraction would find dividing by four too much of a challenge.

I wouldn’t suspect a restaurant could even support 4 kids. I know because I worked at a restaurant in Texas growing up and saw the owner with a wife and newborn struggling to make ends meet even as the restaurant had great foot traffic. This was in 1990 when things were way cheaper. 4 kids is just nutty Bob no matter where you live or what you do. It is about 2 or 3 kids too many for

Years ago, US families had to support fewer municipal union dopes and fewer illegal immigrants.

In New York City harbor, they built Ellis Island to filter out “undesirable” immigrants, even though the country had more space/ more need for younger families. Immigrants that were allowed in were required to have sponsors that would house them and help them find WORK, not welfare.

Then the socialists came in with their safe spaces and their backassward belief that immigrants should get free sh!t while taxpayers get punished. Socialism is having the same disastrous impact on the USA as it had everywhere else.

You watch too much fox news. The productive part of the economy is way better than 8 years ago. The problem isnt immigrants. Pensions are a bigger issue and they are primarily held by citizens. Immigration both legal and illegal has effectively been shutoff by the last two administrations.

Keep painting with your broad brush Bob. And keep subtracting CPI. I’m sure your cost of living will only go down.

Cuntry Boob at it again lol

“Disneyland remains the central attraction of Southern California, but the graveyard remains our reality.”

― Charles Bukowski

Maybe stop feeding Cunt-troll Boob?

Left wing extremists don’t like being called out on their bullshit. Too bad, you are still morons

Oh Bob clearly I’ve struck a nerve with my banker comments so you must be one. It is ironic your defense of the the banking industry which has effectively been a federalized function under the government and had constant backstops and bailouts whenever needed. Effectively you are supporting an industry that has had repeated government bailouts over the last decades and has a backstop with daily repo operations. You argue against socialism but in fact the Fed and government are socialists of a different kind. I’ve never worked in an industry that got bailed out by anyone. This is what true capitalism looks like bob.

At least I didn’t move into California

You have demonstrated that you are unable to grasp simple math concepts, and your reading comprehension makes me wonder if you are even a native English speaker.

Whether I’m a banker or not, whether I’m from TN or not — you are still an idiot and I think I’ve been more than patient with you. Enjoy California and stop bothering everyone else

Oh Bob. I’m a citizen just like your big sorry white butt except I actually do something productive in the private sector and don’t get government bailouts and handouts. It has been irksome to show you are in fact in an industry that is socialized by the government through the central bank. There are clowns to the left of me but you are one of the jokers on the right. Both are socialists of different kinds. Now that you’ve been exposed people can call you a socialist too.

Cunt-try Boob. You’re a dumb fucking cunt Boob.

childish name calling just proves you lost the whole argument

Don’t give a fuck you dumb cunt

BTW idiots going in debt on cars has been going on for a long time it’s just worse now. I can remember more than once my drunk dad going to the car lot in the 80’s and then crying in his beer when the coupon payment book showed up. I am just blown away by prices on things these days its insane.

I was an idiot when I was a bit younger making the big bucks and dodge hotrod trucks come out. I had to have 2 of them. Good news is I still have them both and one only has 33k on them. I’m pretty sure they were the last brand new vehicle ill ever buy ( unless we go full on tard and have AOC require everyone to have an 80k electric pile of **** in the drive). Right now my main driver is a $1000 95 honda accord with over 200k on it. Of course, it helps to know some basic mechanic stuff I just redid all the brakes and calipers. Off topic, but im waiting for HOA’s(which im no part of) to start requiring all electric lawn equipment in order to cut down on noise pollution and those dreadful emissions. The riders are only a few k and stay charged for an entire hour and a half or so. What a joke. I wake up everyday wondering what planet im on I hate it.

Well, dinosaur pee-powered leaf blowers are:

There’s a sweet spot for cars built in the mid-1990s to early 2000’s. Vehicles built then seem to be tanks. The manufacturers figured out fuel injection, clear coat paint (and galvanized dips), V8 engines able to make a lot of power, OK fuel economy, and still able to be repaired by anyone. Few airbags. Reasonably simple automatic transmissions or hydraulic assisted manuals.

These days with all the edicts and regulations from the “leaders” cars are basically disposable. The feats of engineering involved to make a straight 4 punch above its weight class are amazing, but will probably come at a cost of longevity and expensive repairs. 10 speed transmissions with 6 overdrive gears. Dubious “features” like automatic stop-start (where the engine stalls at red lights, intentionally). And of course a dozen or more airbags, any one of which will basically total your car if it goes off (if it doesn’t kill you in the case of the Tanaka recall). And all those electronics, which need software updates, aren’t replaceable, and will tattle to the manufacturer, the insurance company, and the police.

Cars don’t need to be as expensive as they are, but you’re not buying a car, you’re buying a “transportation system,” that includes the vehicle, the manufacturer, the state and several different private industries.

A Michigan Man Underpaid His Property Taxes By $8.41. The County Seized His Property, Sold It—and Kept the Profits.

A state law allows counties to effectively steal homes over unpaid taxes and keep the excess revenue for their own budgets.

In Florida, our system has tax deed sales. If you can’t pay your property taxes, they’re auctioned off by the local tax collector to whomever wants to pay it for you at interest. So you can pay someone’s tax of say $2000 and collect a 10% interest on it per year. If the homeowner can’t pay the interest, the house is sold at auction, you get first dibs on the interest, the bank gets second dibs on the balance of the mortgage, and the original homeowner gets whatever is left.

Interesting that none of the anti communist/socialist zealots have commented on this blatant thievery Could it be that Michigan is just a red state?

The stock chart for Credit Acceptance Corp (CACC) shows its bubble has burst. This company specializes in subprime at the border of loan denied. Their proprietary algorithms help then rationalize taking risks. It is my understanding they use only their money and hold loans until maturity, but I don’t believe it.

The concept of unlimited contracts… Governments spending resources enforcing any crap that 2 parties agree upon at a point of time, under the assumption that adults always take wise decisions… Happy to be in the Netherlands where there are limits to what our gov will enforce, especially in these cases.

The buyers probably have double digit IQs, so they naturally make bad choices. Education would likely have very limited effect on them.

In a sane world, if a lender behaved this way, it would mean that they were not very bright either. But they know that they will get bailed out if they screw up and the marketers and sales people all get their commissions, so why should they care, right?

Maybe making this stuff illegal is not such a bad idea. We all know that neither lenders nor borrowers will start behaving responsibly any time soon.

Spot-on: The lenders know that Uncle Sam has their backs (as proved by the TARP & the GM/Chrysler bailouts), so they have no incentive NOT to lend.

In the desire for ‘Equality’, we tend to forget that the mean IQ, by definition, is 100. Assuming IQ has a normal distribution, as many people have an IQ below 100, as above 100. This is not Lake Wobegon, not all children are above average.

Sadly, a person with an IQ of 80 is ill-equipped for modern life, whether understanding financial matters, making health decisions, or getting a job. At the end of the day, IQ is the great discriminator.

If we hold lenders accountable if they loan to low-IQ borrowers, do we then sue the lenders for IQ discrimination?

The average IQ for the US is 102 and the average for the world is 82. 70 is borderline retarded. There are countries where the average IQ is below 70. That is hard for me to digest, but I think it means you don’t want open borders.

A union of debt slaves would have considerable leverage if they all voted one way or simultaneously decided to step off the merry-go round and sto paying.

The law courts wouldn’t cope and the financial-industrial complex would implode. Quickly.

It might happen anyway in the next downturn, by force of unemployment. Another shot show in plain sight waiting to happen.

And another example of recency bias where borrower and lender expect borrowers ability to pay to remain as it is ad infinitum.

Yes, I know they don’t care so long as they get the fees.

There is a case for laws to set boundaries especially when our values have become so twisted. Knowingly trapping others in debt – WRONG.

It takes government regulation to recognize certain actions as fraud. Not gonna happen here.

Another example of a sick extractive financial system, exploiting people lacking education/common-sense, supporting an industrial complex that is about to collapse.

If I were caesar, the following warning in 50 point type, red lettering would be the mandatory front page of every car loan:

I hereby formally acknowledge fair warning receipt that any car loan for greater than 36 months is dangerous to my financial health and, although legal in every state, the attachment of negative equity to any loan document I ever sign is a sure sign of cosmic scale ignorance and stupidity.

I recall being astonished when I was in the States (after GFC, don’t recall the year) about the wall to wall advertising on the radio for 1. loans to go to college; 2. loans for cars. All of them were saying it doesn’t matter how much you earn, even without work, bla bla. Astonished was I. In Canada and Europe I had never once heard advertising for financing cars/college, let alone for people without income. Negative car equity. I’m sure there would be a few takers here, but nobody is crazy enough to be offering. Seems like a losing business.

Not a losing business at all. American banks take those fruadulent loans, package them up, and sell them to Canadian and European pension funds.

Household debt as a percentage of disposable income is far higher in Canada than the US, so there are more than a few takers there.

Europe tends to nationalize its “debts”, and debts is in quotes because like the people taking out $66K truck loans in the USA, Europeans have no intention of actually paying.

All the G7 economies have been living beyond their means, even if the financing is aggregated at different levels. The system is coming off the rail now (in Europe, Japan and the USA) because it has become obvious the debtors both will not and can not actually pay.

No intention nor ability to pay means the “debt” facade is crumbling

When will the US’s foreign used car market slow down enough to clog Uncle Sam’s arteries with cars coming off lease?

Is it shocking to find out there are stupid people and that others are taking advantage of them? I don’t think this is anything new. It’s been happening for ever!

Exactly why we need negative rates. :>))

This is just another version of extending and pretending. In Texas where disposable income is high, is where there are the most $ per capita outstanding debt on car loans. There will be a big repo market there soon when the party ends. More than any other state during this economic boom, Texas represents the place that will blow up on the downside.

I lived in Dallas on and off for 20 years. At least there it was a big deal what car you drove. That might explain the per capita debt on car loans. One street I lived on, very low end of upper middle class, had Rolls in three of the driveways…..

Yep. I grew up in a middle-class suburb of Dallas. I believe it has only gotten worse with more disposable income over the years. It is ironic to me how much of Texas is slowly morphing into Orange County South – especially around Houston and Dallas.

“Wages are not keeping up with needs and desires.”

That’s new?

With the birth of the assembly line, Henry Ford paid his employees much better than most did, so they could actually buy the cars they made. Automakers continue to automate, but now they are at the forefront of wage cutting.

This sounds like the “In the long run, we are all dead” kind of thinking. Isn’t that what Keynes meant when he said that? Instead of buying the thing outright, we just take out a loan and pay it till we die? Or no?

Somebody is buying the loans and repackaging them and selling them. At some level the risk is being taken by those buying the risk associated with the loans. They are likely being sold into unsuspecting pension funds under opaque instruments.

And then, since being a well indoctrinated idiot involves being suckered into believing there exists such a thing as a “System” which it would somehow be a bad thing if “collapsed”, the ever dwindling group of productive Americans, will be forced, at gunpoint, by some moron who insists “guns are bad and should be banned” no doubt, to ultimately pay for the 100% childish idiocy.

The same people keeping the system alive are the ones giving our the loans and then repackaging them and selling them as collateralized debt obligations. There are always 2 sides to every loan but with derivatives there are so many more sides. This all sounds familiar.

If you stop to think about it you are getting nailed by the banks and sellers of goods and services for almost everything now, unless you pay cash for the full price of something you are using plastic. Even groceries are getting put on credit cards by people who are too deep in debt to pay off every month.

Seems like the education system should teach people how to do basic math.

It should be illegal to charge taxpayers for an education that apparently was not received — or else the persons taking these neg equity loans perhaps should be declared mentally incompetent. Probably some of both cases.

In any event, the finance industry can’t force a buyer to sign a dumb loan for a $66K truck. There are lots of affordable cars that buyers could purchase instead

These loans wouldn’t be happening if the buying public could do simple math.

They should just subtract the interest the way you do with CPI in states with low costs thr way you do Bob.

FWIW the state with the highest outstanding car loan amounts per capita is Texas. This means Texans are living above their means the most when it comes to cars.

For God’s sake california boy… nominal minus inflation equals real rate.

Its just not that complicated. Even a mathematically illiterate moron like you should be able to grasp this.

Then again, if you had a brain you wouldn’t have moved INTO California when all the smart money is moving out

The map says real GDP moron. If you want nominal GDP you add inflation back. Real gdp is a poor indicator of personal progress unless your a country bumpkin that cant afford to live anywhere but low cost areas that have have 1% GDP.

Yep, your map says real GDP and that seems to be confusing the hell out of imbeciles like@Casual_Observer

Your map took a nominal California GDP of 4.1% NOMINAL, subtracted 2.2% CPI and printed 1.9% real GDP.

People smarter than you know that California’s inflation rate, and its cost of living, is much higher than the national average — much higher than CPI. So the smart money (the people leaving your sh!t hole state) knows the correct math involves subtracting a much bigger inflation number.

The smart money takes the same 4.1% California NOMINAL rate, and subtracts 4% California inflation (its probably higher than that, but lets be generous) and they know the real GDP for California is (at best) 0.1%. Much less than the lie you tell yourself.

Inflation in Utah, where Mish is headed, is less than the national average, so the same math 4.1% nominal – 1% Utah inflation => 3% Utah growth. Using CPI understates real GDP in Utah, and overstates it in sh!thole California.

You are just too dumb to grasp simple math, which explains why you moved into California while the smart money moved out

Here he goes this moron….blah blah blah. Insulting everyone…

Just standing up to the sh!t heads from California who try to force themselves on the rest of the country and the world. No one asked you losers to mess up our health care system (it was bad enough without your help). No one asked you to fill our cars with your “safety” nonsense, we can pick safety measures ourselves. No one asked you to dictate MPG requirements either.

You forced yourselves on the country, and you are dumb enough to think there wouldn’t be blow back.

You are not “everyone”. You are extremist left wing a$$holes who think you are better than everyone who never asked for your opinions. Just shut up.

It should also be illegal to charge taxpayers for a court system abused to serve as a crude shakedown mechanism for collecting on loans well in excess of the value of the thing the loan was made for. A change as simple as that, would get rid of this sort of nonsense virtually overnight.

The NEW truck sales people lost me YEARS ago when the cool ones were 50k+.

However, I be abbey normal: the F150 I bought new in 2000 is now 19 years old.

Without loans prices of cars and trucks would have fallen long ago. Same as houses. Take away the loan market and prices plummet. The same would happen with healthcare if insurance disappeared. In some alternative universe without bankers it’s possible.

The cool pickups are 100k now.

Sick and twisted financial industry. It should be illegal to roll negative equity onto a new car purchase, particularly when the new car depreciates the minute you drive it off the lot.

Seems like the education system should teach people how to do basic math.

It should be illegal to charge taxpayers for an education that apparently was not received — or else the persons taking these neg equity loans perhaps should be declared mentally incompetent. Probably some of both cases.

In any event, the finance industry can’t force a buyer to sign a dumb loan for a $66K truck. There are lots of affordable cars that buyers could purchase instead

In addition to schools teaching basic math, they should teach a course I would call “Defense against marketing” which would help people understand when they are being manipulated to their disadvantage. Marketing is the reason people by $66,000 trucks when they don’t otherwise have a pot to piss in.

It is also marketing the monthly payment as opposed to the whole loan. It is the same as what’s been happening for decades in real estate. You can afford the monthly payment. Forget about the number of years.

I also agree with Country Bob. We don’t need to protect people from doing stupid things. Why is economics not a required course in junior high and high school?

I also agree with Stuki that the only legal change required is to go back to the old bankruptcy rules, with easier access to Chapter 7. People should not be debt slaves. If people do get in over their heads, they should have a way out. That also causes banks and other lenders to be much more careful to whom they lend, of course. But, then people will scream about how discriminatory and unfair lending is, that some people can get loans while others can’t. You can’t have it both ways, though. Either you have a system where lenders will lend to everyone, and people have a hard time getting out of it, or a system where people can get out of it easily, so only the most credit worthy can get loans. I favor the latter.

Economics used to be a required course, back when education was used to prepare children to be contributing members of society.

Now education is used as a political indoctrination tool, with a dual objective of providing make-work jobs for municipal unions. Practical courses like home economics were replaced by courses teaching transgender neutrality. History courses were transformed into lessons on how to shift blame to the other guy and demand reparations; facts and practical limits on holding a grudge be damned.

The failed education system in the US costs too much and it doesn’t serve the function it was intended for.

I agree with Country Bob. We don’t need more laws to protect people from what we might consider poor financial decisions.

Nonsense, you think it should be legal to practice predatory lending just because some desperate and inexperienced people fall for a conman’s game?

We need lending laws that consider a contract with predatory lending elements to simply be void. The same way we now have the right to sue if we buy a house and it turns out the previous owner did not disclose information affecting the value of the property, real estate loans have recourse, auto loans pretty much don’t unless there is outright fraud, and even then getting your rights enforced will cost more than the value of all but a very few cars/trucks.

Quicker and easier to come by access to banksruptcy also curbs this sort of stuff. Just mail in the keys and walk……

This used to be one of America’s strong points. Instead of Middle Eastern debtors prisons or European style permanent wage garnishments trapping potentially productive people and resources for the rest of their lives (and beyond in some cases), Americans went bankrupt and started over. Much, much more efficient allocation of scarce resources, as it simultaneously puts the onus on lenders to not act like idiots and then come crying to Massa Gommiment to harass someone in order to make their idiot selves whole.

Of course, the era of American “laws” and governance having anything whatsoever to recommend them, has long since passed.

I’d say simply take the government out of it. If you walk away from the purchase, the lender gets the vehicle back with no other recourse, including no marks on anyone’s credit score. That’ll make lenders be a little more responsible with their depositors money.

Yes. Let’s undo all those years of contract law to make bad deals unenforceable. We can put a 9th DCA judge in charge of it all and she can tell you years later if she has unilaterally undone your contract. Maybe you’ll have to buy back that car, house, old bike you sold 15 years ago b/c she has determined the guy you sold it to got a raw deal even though it was an arms length transaction with all the terms spelled out in writing.

Also, why does anybody feel bad for Mr. Mr. Schricker? I’m in the top tier of income earners and I’m driving a car w 120k miles on it; broken sunroof, engine light on the last 30k miles but I refuse to pay $800 to fix the sensor that went bad. And I’ll continue to drive it (like my last car) until a mandatory repair exceeds the value of the car. Meanwhile, Mr Schricker has traded cars 4 times in the last 2 years (think about the time and transaction costs alone). “ He replaced one because it had 100,000 miles and another when he went through a divorce, and he changed cars again when his family was expanding.” (how does your family expand shortly after a divorce?). Sorry but i don’t think there is any law that could be passed to help Mr. Schricker.