Note: Please stay with this post even if you do not understand the terms. I tie this all together so that you can see what is going on.

Yesterday afternoon, Randy Woodward, the @TheBondFreak pinged me with a chart of the SOFR rate vs LIBOR.

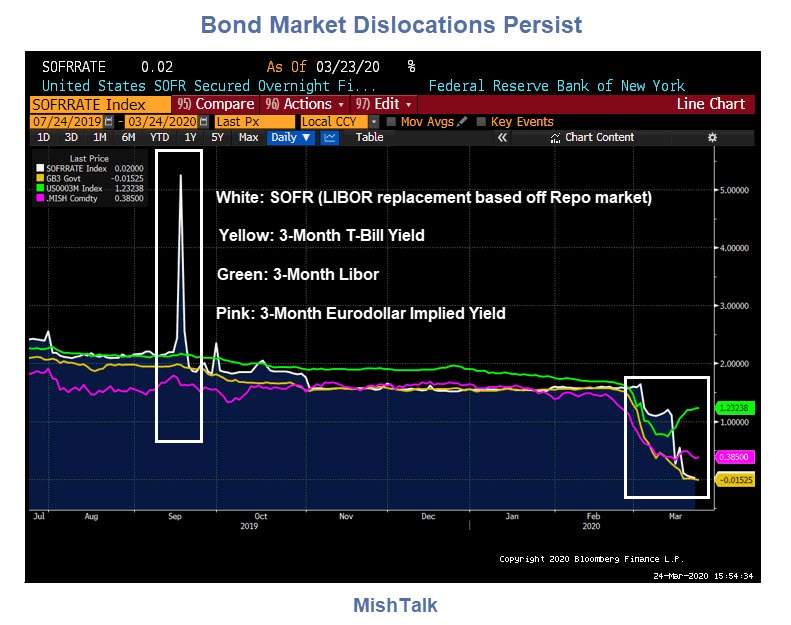

SOFR stands for Secured Overnight Financing Rate.

In June 2017, US Federal Reserve Bank’s Alternative Reference Rates Committee selected SOFR as the preferred alternative to Libor. The committee has noted the stability of the repurchase market on which the rate is based. SOFR is based on the Treasury repurchase market Treasuries loaned or borrowed overnight. SOFR uses data from overnight Treasury repo activity to calculate a rate published at approximately 8:00 a.m. New York time on the next business day by the US Federal Reserve Bank of New York.

SOFR is the new replacement for LIBOR. As such, the rates should track closely. SOFR should also closely track the 3-month T-Bill rate which in turn should closely track the Eurodollar rate. All of these are interest rate products.

In September the SOFR rate spiked as high as 9% intra-day. Since then, the Fed managed to get SOFR under control, but now we see dislocations in LIBOR and the Eurodollar.

The important point is these products should all track within reasonable spreads but they don’t.

LIBOR vs SOFR

The initial chart Woodward sent showed LIBOR spiking by over 100 basis points above SOFR.

To be more precise, LIBOR was at 1.23% and SOFR was at 0.02%.

I asked, why stop there?

Over the course of the next hour I kept asking for more and more things on the same chart, ultimately ending up with LIBOR, SOFR, Eurodollars, the 3-Month T-Bill, and Fed Funds Futures all on one chart.

Eurodollar Explanation

Eurodollars may be one of the worst named products in history. Eurodollars have nothing to do with euros. Rather it represents the interest rate on US dollars held overseas.

Eurodollars are time deposits denominated in U.S. dollars at banks outside the United States, and thus are not under the jurisdiction of the Federal Reserve. Consequently, such deposits are subject to much less regulation than similar deposits within the U.S. The term was originally coined for U.S. dollars in European banks, but it expanded over the years to its present definition. A U.S. dollar-denominated deposit in Tokyo or Beijing would be likewise deemed a Eurodollar deposit (sometimes an Asiadollar). There is no connection with the euro currency or the eurozone.

CME Eurodollar futures prices are determined by the market’s forecast of the 3-month USD LIBOR interest rate expected to prevail on the settlement date. A price of 95.00 implies an interest rate of 100.00 – 95.00, or 5%. The settlement price of a contract is defined to be 100.00 minus the official British Bankers’ Association fixing of 3-month LIBOR on the day the contract is settled.

To get Eurodollars on the same scale as everything else, we had to use inverse math as described above.

Hopefully, it is easy to see from the above explanations (even if you don’t quite understand them), that these products are all related and should all reasonably track each other.

Five Key Interest Rate Measures

Note that Eurodollars (pink) are a leading indicator of what the Fed is expected to do.

The Fed Funds Effective Rate lags. This is why Jim Bianco and I suggested the Fed would cut and cut big. Bianco was confident enough to say the Fed would cut rates between meetings while I only mentioned the possibility.

Kudos to Bianco for his bolder call.

Not only did the Fed cut once intra-meeting but twice, again as discussed by Bianco and I. But look at the result.

Fed Fund Futures vs Fed Funds Rate vs Eurodollar Implied Yield

Not only did the Fed’s second cut totally blow up LIBOR by 120+ basis points, it also dislocated Eurodollars.

The implied Eurodollar rate suggests the Fed needs to hike interest rates by 1/4 point.

Well, good luck with that.

What Happened?

It appears the market was not prepared for the Fed to cut all the way to zero.

Moreover, the speed of the cuts caught nearly all the market participants off guard.

Take a peek at that top chart again.

Then recall the Fed’s message for months heading into 2020: “No more cuts, no more hikes for a year.”

Note how closely the 3-month T-Bill, Eurodollars, LIBOR, and SOFR all tracked each other, until they didn’t.

Spotlight Japan

Important –> Japan repo rates are now the most negative ON RECORD as banks scramble for dollars, meaning borrowers of collateral are paying a lot for it, so they can exchange it for $ funding through the Fed’s FX swap lines.https://t.co/3BfTthoxq6 by @StephenSpratt pic.twitter.com/rgYpYWZVRd

— Tracy Alloway (@tracyalloway) March 25, 2020

Hooray!?

Hooray, the Fed has SOFR under control. But what about LIBOR and Eurodollars?

Eurodollars are the most widely traded futures contract. And despite all the time allotted, the market is still not prepared for the switch from LIBOR to SOFR.

Let’s return to one of my opening statements “In June 2017, US Federal Reserve Bank’s Alternative Reference Rates Committee selected SOFR as the preferred alternative to Libor. The committee has noted the stability of the repurchase market on which the rate is based.”

But what about the stability of all those LIBOR and Eurodollar contracts?

Commercial Mortgages on Brink of Collapse

Here’s a link that caught my eye: Real Estate Billionaire Barrack Says Commercial Mortgages on Brink of Collapse.

By any chance are those contracts LIBOR based?

Very Deflationary Outcome Has Begun: Blame the Fed

The Fed is struggling mightily to alleviate the mess it is largely responsible for.

I previously commented a Very Deflationary Outcome Has Begun: Blame the Fed

The Fed blew three economic bubbles in succession. A deflationary bust has started. They blew bubbles trying to prevent “deflation” defined as falling consumer prices.

BIS Deflation Study

The BIS did a historical study and found routine price deflation was not any problem at all.

“Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive,” stated the BIS study.

For a discussion of the study, please see Historical Perspective on CPI Deflations: How Damaging are They?

Deflation is not really about prices. It’s about the value of debt on the books of banks that cannot be paid back by zombie corporations and individuals.

Assessing the Blame

Central banks are not responsible for the coronavirus. But they are responsible for blowing economic bubbles prone to crash.

The equities bubbles before the coronavirus hit were the largest on record.

System Wide Margin Call

Please note “The worst scramble for cash is happening in an opaque corner of the market that the Fed can’t control.“

Unfortunately, We’re Looking at a System-Wide Margin Call

The Federal Reserve ushered out a second wave of quantitative easing Monday. But the worst scramble for cash is happening in an opaque corner of the market, where Chairman Jerome Powell has little control. What we’re witnessing is a system-wide margin call.

With the coronavirus outbreak intensifying, asset managers are getting squeezed by a record outflow from bond funds and billions more from stock funds. Even bigger withdrawals are probably happening in the over-the-counter world, where trades are conducted out of public eye, through broker-dealers. When traders get margin calls, they resort to selling their most liquid assets, usually stocks and U.S. Treasuries. This only deepens the slide.

As of June 2019, the notional amount of such derivatives rose to $640 trillion, the highest since 2014, data provided by Bank of International Settlements show. Gross market value, which gauges how much money would be transferred if all trades shut down, totaled about $12 trillion in mid-2019, 30% lower than in 2014.

In ordinary times, gross market value is a better gauge of the amount at risk because of netting agreements. If a bank is $99 short on a trade and $99.10 long with other clients, its exposure is only 10 cents.

But we live in extraordinary times, and gross market value can also serve as a proxy for how much money the financial system has put aside to sustain that $640 trillion OTC derivatives exposure, according to research conducted at Prerequisite Capital. As of last June, the margin requirement, which the firm defines as the ratio between gross market value and notional amount, was 1.9% — a record low. In other words, there isn’t enough balance sheet provision for black swan events.

From risk parity strategies to statistical arbitrages, the coronavirus is unraveling the most sophisticated of trades. This is a reminder that there’s only so much hedging we can do. Today you’re in, tomorrow you’re out.

Mad Scramble to Rebalance $640 Trillion

So, we have a mad scramble for cash with $640 trillion in derivatives floating around.

If you prefer, the actual gage is a a mere $12 trillion of which interest rate derivatives are likely the single largest component.

Two Questions

- What can possibly go wrong?

- Where to from here?

I will leave number one to your imagination.

In regards to number 2, US Output Drops at Fastest Rate in a Decade

More importantly, please consider Nothing is Working Now: What’s Next for America?

I discuss 20 things that are likely.

Final Question

I leave you with one simple question:

Got Gold?

Mike “Mish” Shedlock

The ” virus” did NOT crash the world…the REsponse did.

The US COULD have spent 5 million to save/Quarintine EVERY

person that was in the vulnerable 60 + / weak ect…

in 1 st class hotels IN Hawaii….

But the mission was to SAVE the BANKS / Conex paper fraud system

ALL paper gold will now be ” paid in CASH ” while they smash the fake price down…

AFTER easter – prices will…magically EXPLODE for real

GOLD in your HAND….or be FDR ..ed…deemed illegal for the AVERAGE joe six pack…ONLY bankers allowed to own that BARBEROUS relic…

Mish, I know you are a big deflationista but I just don’t think the fed is going to allow deflation no matter what. I think they will get inflation and they want it badly enough they will SETTLE for hyperinflation.

There will be NO sustained inflation until the debt overhang addressed.

Disinflation / deflation for now.

Well we have to part company there. The debt overhang is the reason and the way they inflate. Money is created into the economy by borrowing/lending. All that debt IS MONEY. Getting rid of it, somehow just defaulting or otherwise wiping it out of existence would basically be the definition of deflation.

Want to add there is a story at CNBC: Here’s why stocks are rising on terrible news

Let’s just say if you thought the response to this economic catastrophe was going to be unlimited bailouts by the fed, negative rates, and trillions upon trillions of stimulus by the federal treasury what would YOU expect? Vast and towering inflation because of all that new minted money chasing now far less production of goods and services, prices MUST rise. So, if the equity markets were at almost 30,000 on the DJIA and dropped to 17k for some that looks cheap in spite of the sorry economy. But, if you expect 17k to be the bottom and the DJIA to be at 125,000 by 2023 this would indeed be the market buying opportunity of a lifetime. Of course it is all just inflation, but that does not matter just as it has not mattered since 2009’s low under 7k.

The economy will eventually recover most of what it lost, but wealth inequality will make sure those gains are concentrated in the top 10% and mostly 1%, the average American will be poorer, and the poor will be much poorer.

The impossible has now happened: 1 & 3 mo T-bill yields negative:

“Did the Fed Cut Too Much?”

…

3 month Treasury yield sporting a negative sign.

Press release

20 March 2020

Coordinated central bank action to further enhance the provision of US dollar liquidity

ECB and other major central banks to offer 7-day US dollar operations on a daily basis

Operations with 84-day maturity continue to be offered weekly

New frequency effective as of 23 March 2020, to remain in place for as long as appropriate to support smooth functioning of US dollar funding markets

The Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, the Federal Reserve, and the Swiss National Bank are today announcing a coordinated action to further enhance the provision of liquidity via the standing US dollar liquidity swap line arrangements.

To improve the swap lines’ effectiveness in providing US dollar funding, these central banks have agreed to increase the frequency of 7-day maturity operations from weekly to daily. These daily operations will commence on Monday, 23 March 2020, and will continue at least through the end of April. The central banks also will continue to hold weekly 84-day maturity operations.

The swap lines among these central banks are available standing facilities and serve as an important liquidity backstop to ease strains in global funding markets, thereby helping to mitigate the effects of such strains on the supply of credit to households and businesses, both domestically and abroad.

“SOFR is the new replacement for LIBOR. As such, the rates should track closely. “

…

Maybe, just maybe, SOFR is the lead dog.

With Fed repo operations responding. I had no idea they changed the scheme in 2017. I guess the “S” in SOFR is supposed to instill confidence.

The graphs look like analogues for every suddenly flooded engine: Reduced power output and wasted fuel. All that’s missing is a stall soundtrack and clouds of smoke.

…and that BANG! KERWHACKETA KERWHACKETA KERWHACKETA Sound.

SOFR is collateralized with US Treasury debt. Eurodollars a backed by the full faith and credit of the banks doing the borrowing and lending. This is a statement about perceived risk in the banking sector and not about the rate cut itself.

Mish: I’m one of your poorer readers. I have gold bullion coins but a lot more in silver in the form of “junk silver”. Do you believe I’m OK. I feel small denomination US pre 64 silver coins will be more “tradable” when the SHTF.

Mish what about silver? We haven’t seen a gold:silver ratio like this before

Is libor being replaced by sofr or just an alternate for overnight funding only. Libor tracks multiple currencies and has longer loan durations so I am not clear how it can be replaced by sofr. Also eurodollars seem to be the same product as libor? They both track borrowing for USD in foreign banks, so am don’t see how these differ in theory.