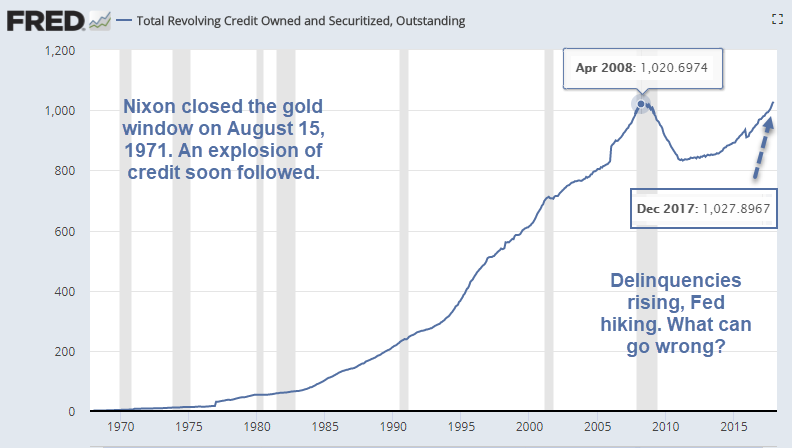

Revolving Credit Hits New Record High

In December, revolving debt has topped the previous high-water mark of $1.021 trillion set in April of 2008. Debt as of December 2017 (the latest available) is $1.028 trillion.

Relationship Killer

In addition to student loans, credit card debt is another factor holding down home ownership and family formation. Studies show Credit Card Debt is a Relationship Killer.

- Of all household debts, Americans find credit card debt the most unacceptable in a partner, but credit card balances are creeping higher.

- About 43 percent off all card holders carry a balance each month according to the American Bankers Association.

- More than 3 in 4 Americans consider too much card debt a relationship deal breaker, according to personal finance site Finder.com.

Overdue Debt Hits 7-Year High

The Financial Times reports Overdue US Credit Card Debt Hits 7-Year High.

Distressed debt, defined as debt that’s at least three month’s delinquent, totals $11.9 billion. That’s an 11.5% fourth-quarter surge.

The Financial Times also notes “More Americans are also falling behind on their mortgages, for which problematic debt levels rose 5.2 percent over the same period to $56.7 billion.”

Deflationary Debt Trap Setup

These numbers are huge deflationary. When credit expands there is inflation. When credit contracts (think defaults, bankruptcies, mortgage walk-away events), debt deflation occurs.

Here’s my definition of inflation: An increase in money supply and credit, with credit marked to market.

Deflation is the opposite: A decrease in money supply and credit, with credit marked to market.

Looking Ahead

- Credit card delinquencies are priced as if they will be paid back. They won’t.

- As soon as recession hits, defaults and charge-offs will mount. In turn, this will reduce the amounts banks will be willing to lend.

- Subprime corporations who had been borrowing money quarter after quarter will find they are priced out of the market, unable to roll over their debt.

In a fiat credit-based global setup, this is how the real world works.

Rear-View Mirror Thinking

Those looking for a huge inflation boost fail to understand credit dynamics.

Austrians who only look at money supply keep expecting pent-up inflation. The Monetarists at the Fed (central banks in general), are clueless about the situation they fueled.

Perhaps we get consumer inflation for a quarter or two, but inflation is in the rear view mirror, primarily having impacted asset prices, not consumer prices.

Rising interest rates are already starting to impact the housing market.

The auto market, home supply markets, and consumer credit in general got a temporary housing boost.

What’s next won’t be pretty, and almost no one sees it coming. They can’t. Inflation is in the rear-view mirror.

What economists expect to happen, already has. They don’t see it because they do not understand what inflation really is.

Weakening Economy

The economy is weakening and the Fed, fearing inflation is hiking right into it.

- Pending Home Sales: Pending Sales Unexpectedly Dive to Lowest Level in 3.5 Years.

- GDP Forecasts Dive: GDPNow “Real Final Sales” Forecast Dips to 1.6%

- Durable Goods: New Durable Goods Orders Dive 3.7%

- New Home Sales Down 7.8%: Six Reasons Sales Can’t Break Out

- Trade War Setup: Huge Mistake Coming Up – Trump Set to Promote Trade Hawk Peter Navarro

Moreover, real median wages have fallen in seven of the last eleven years!

This helps explain the falling savings rate. It certainly does not support consumption.

For discussion, please see How the Fed’s Inflation Policies Crucify Workers in Pictures.

Debt Deflation Coming Up

I expect another round of asset-based deflation with consumer prices and US treasury yields to follow.

Mike “Mish” Shedlock

http://vimaxmedan.xyz/obat-testo-ultra-medan/

semoga artikel yang anda post menjadi prioritas pembaca artikel sangat bagus dan mantap kunjungi juga website di bawah ini http://vimaxmedan.xyz/alamat-hammer-of-thor-di-medan/

semoga artikel yang anda post menjadi prioritas pembaca artikel sangat bagus dan mantap kunjungi juga website di bawah ini

http://toko-bose.com/viagra-usa-di-jakarta/

http://toko-bose.com/obat-cialis-di-jakarta/

http://toko-bose.com/obat-pelangsing-di-jakarta/

http://toko-bose.com/obat-hercules-di-jakarta/

http://toko-bose.com/obat-klg-pill-di-jakarta/

http://toko-bose.com/vimax-di-jakarta/

http://toko-bose.com/titan-gel-di-bekasi/

http://toko-bose.com/hammer-of-thor-di-bekasi/

http://toko-bose.com/obat-forex-bekasi/

http://toko-bose.com/obat-erogan-di-bekasi/

http://toko-bose.com/obat-penirum-di-bekasi/

http://toko-bose.com/hermuno-anti-parasit-di-bekasi/

http://toko-bose.com/blog/jual-alat-bantu-sex-pria-wanita-di-jakarta/

http://toko-bose.com/blog/jual-obat-pembesar-penis-di-jakarta/

http://toko-bose.com/blog/toko-obat-kuat-tahan-lama-asli-di-jakarta/

http://toko-bose.com/titan-gel-bandung/

http://toko-bose.com/hammer-of-thor-bandung/

http://toko-bose.com/obat-forex-asli-bandung/

http://toko-bose.com/obat-erogan-bandung/

http://toko-bose.com/obat-penirum-bandung/

http://toko-bose.com/obat-anti-parasit-bandung/

http://toko-bose.com/viagra-asli-bandung/

http://toko-bose.com/obat-cialis-di-bandung/

http://toko-bose.com/obat-kuat-viagra-australia/

http://toko-bose.com/obat-hajar-jahanam/

http://toko-bose.com/obat-pelangsing-di-bandung/

http://toko-bose.com/obat-hercules-di-bandung/

http://toko-bose.com/obat-klg-di-bandung/

http://toko-bose.com/vimax-asli-di-bandung/

http://toko-bose.com/titan-gel-jakarta/

http://toko-bose.com/hammer-of-thor-jakarta/

http://toko-bose.com/forex-asli-jakarta/

http://toko-bose.com/obat-erogan-di-jakarta/

http://toko-bose.com/obat-penirum-di-jakarta/

http://toko-bose.com/obat-hermuno-anti-parasit-di-jakarta/

http://toko-bose.com/viagra-usa-di-bekasi/

http://toko-bose.com/obat-cialis-di-bekasi/

http://toko-bose.com/obat-pelangsing-di-bekasi/

http://toko-bose.com/obat-hercules-di-bekasi/

http://toko-bose.com/obat-klg-di-bekasi/

http://toko-bose.com/obat-vimax-di-bekasi/

http://toko-bose.com/obat-rx24-di-bekasi/

http://toko-bose.com/obat-titan-gel-di-cikarang/

http://toko-bose.com/obat-hammer-of-thor-di-cikarang/

http://toko-bose.com/obat-forex-cikarang/

http://toko-bose.com/obat-erogan-cikarang/

http://toko-bose.com/obat-penirum-cikarang/

http://toko-bose.com/obat-hermuno-anti-parasit-cikarang/

http://toko-bose.com/obat-viagra-cikarang/

http://toko-bose.com/obat-cialis-di-cikarang/

http://toko-bose.com/obat-pelangsing-di-cikarang/

http://toko-bose.com/obat-hercules-di-cikarang/

http://toko-bose.com/obat-klg-di-cikarang/

http://toko-bose.com/obat-vimax-di-cikarang/

http://toko-bose.com/obat-anabolic-rx24-di-cikarang/

http://toko-bose.com/obat-titan-gel-di-bali/

http://toko-bose.com/obat-hammer-of-thor-di-bali/

http://toko-bose.com/obat-forex-di-bali/

http://toko-bose.com/obat-erogan-di-bali/

http://toko-bose.com/obat-penirum-di-bali/

http://toko-bose.com/obat-hermuno-anti-parasit-di-bali/

http://toko-bose.com/obat-viagra-di-bali/

http://toko-bose.com/obat-cialis-di-bali/

http://toko-bose.com/obat-pelangsing-di-bali/

http://toko-bose.com/obat-hercules-di-bali/

http://toko-bose.com/obat-klg-di-bali/

http://toko-bose.com/obat-rx24-di-bali/

http://toko-bose.com/obat-perangsang-di-bali/

http://toko-bose.com/obat-perangsang-cair-di-bali/

http://toko-bose.com/obat-titan-gel-di-semarang/

http://toko-bose.com/obat-hammer-of-thor-di-semarang/

http://toko-bose.com/obat-forex-di-semarang/

http://toko-bose.com/obat-erogan-di-semarang/

http://toko-bose.com/obat-penirum-di-semarang/

http://toko-bose.com/obat-hermuno-di-semarang/%5BU%5D%5B/U%5D

http://toko-bose.com/obat-viagra-asli-di-semarang/

http://toko-bose.com/obat-cialis-di-semarang/

http://toko-bose.com/obat-viagra-australia-di-semarang/

http://toko-bose.com/obat-hajar-jahanam-di-semarang/

http://toko-bose.com/obat-kuat-maxman-di-semarang/

http://toko-bose.com/obat-kuat-black-ant-di-semarang/

http://toko-bose.com/obat-pelangsing-di-semarang/

http://toko-bose.com/obat-hercules-di-semarang/

http://toko-bose.com/obat-klg-pill-asli-di-semarang/

http://toko-bose.com/obat-rx24-asli-di-semarang/

http://toko-bose.com/obat-perangsang-di-semarang/

http://toko-bose.com/obat-perangsang-cair-di-semarang/

http://toko-bose.com/obat-semenax-asli/

http://toko-bose.com/obat-kianpi-pill-asli/

http://toko-bose.com/obat-grow-up-asli/

http://toko-bose.com/condom-getar-silicone/

http://toko-bose.com/condom-duri-silicone/

http://toko-bose.com/condom-sambung-jumbo/

http://toko-bose.com/penis-tempel-jumbo/

http://toko-bose.com/penis-ikat-pinggang/

http://toko-bose.com/penis-mutiara-getar-putar/

http://toko-bose.com/penis-getar-goyang/

http://toko-bose.com/penis-tekuk-manual/

http://toko-bose.com/vagina-center-flashlight/

http://toko-bose.com/boneka-full-body-asli-silicon/

http://toko-bose.com/vagina-getar-suara-silicon/

http://toko-bose.com/vagina-nungging-getar-silicon/

http://toko-bose.com/obat-ericfil-asli/

http://toko-bose.com/vakum-pembesar-penis/

http://toko-bose.com/pro-extender-pembesar-penis/

http://toko-bose.com/vakum-pembesar-payudara/

http://toko-bose.com/celana-vokoou-usa/

http://pasutri-makassar.com/obat-erogan-makassar/

The folks were accidentally benefiting from the leftover crumbs showering down from the asset inflation process because they needed a place to raise their family and didn’t feel like moving after the children left. In the end the rent on their assisted living apartment will consume a great deal of their profits.

Hi Mish, I’ve been reading headlines lately saying higher inflation is on the way, mostly due to the corporate tax cut. I read corporations pay about 340 Billion in taxes, seems like even half of that going back into the economy wouldn’t cause inflation due to the items you highlighted in your article. Look forward to any thoughts you might have. Thanks..

Yes. For both new and existing equity loans. The interest deduction now only applies to the primary lender.

… even if demand drops off markedly.

The inflation issue is much more complex than is being represented here. Yes, a credit boom (inflationary) is generally followed by a credit bust (deflationary) but for each good and service the circumstances are different i.e. it is not one or other. The deflationary bust is going to, almost exclusively, impact asset prices and those sectors that are riddled with over-capacity. It is highly unlikely you are going to see deflation in healthcare and food costs, for example, and there are several other places where, for structural reasons, deflation won’t occur.

Mish, I have a small point of contention with your article. It’s not just banks deciding on their own to reduce lending in a recessionary environment. It’s more in relation to customers/clients unwilling to take on more debt during a recession thus causing banks to reduce lending. Banks trend to create money only when there is demand for it. Why borrow against declining asset values?

“My folks recently sold into the great housing bubble their house for an amount greater than their entire lifetime wages. “

Which exactly, too a tee, explains why the wages of American workers have been stagnant over the same period. All the value add, that all their work and all their additional productivity has generated has, by way of Fed engineered inflation, been confiscated and handed out to “asset owners” in the form of appreciation of the exact same asset.

Of course, the workers being handed the short stick during that period, were too economically illiterate to see the scam unfolding in front of their very eyes. And, even more disturbing, they are too economically illiterate even to recognize it now, in hindsight.

Instead being played like useful idiots. Told to run around like angry, dumb stooges, blaming their fellow working men in China and Mexico. While still paying no attention to The Fed continuing their mission, of handing the wealth the workers create, to the same people who have been handed it sans effort since 1971: Idle asset owners; and privileged, produce-nothing leeches in the FIRE, legal and government complexes. Which is where you’ll find every.single.penny of wages that workers are now grumbling about been shortchanged.

https://www.amazon.co.uk/Another-Financial-Crisis-Future-Capitalism/dp/1509513728 He got the last deflationary crash spot on.

Prof Steve Keen tends to agree with you.

My folks recently sold into the great housing bubble their house for an amount greater than their entire lifetime wages. For that amount they could purchase a similar house elsewhere at an equally inflated price. I don’t think I will do as well in dollars of capital gain on my house with the expected debt deflation coming. However, I believe whatever happens inflation or deflation I should be able to sell my house and buy a similar one at a similar price to what I receive in a sale. Since I need a roof over my head nothing has changed ; 1 house still = 1 house. The key is avoiding buying with a lot of debt.

“Which hole of yours did you pull that ridiculous number out of?” Reading comprehension my friend. The article states revolving debt is $1.208T with 3 months delinquent of $11.9B. That is 0.985%, I rounded to 1%.

Great – tell us what’s coming and why! Thanks in advance.

Our entire system is debt based. So what. Next please

I think the great Bearish Bear-Mish had something in mind more among the lines of “people impulsively spending on their credit card because of record low interest rates” rather than “tactfully exploiting their credit card interest rates.”

I’m sure the credit card companies see it somewhere in the middle.

The real question is this: what will the delinquency rate be when base interest rates return to pre-2008 levels? Which everyone expects caeteris paribus.

… “especially if the Fed hikes into “money-credit deflation” because of their fear of “price inflation.”

I usually do say “price inflation” or “debt deflation” as appropriate. Most of the time it is clear what I am talking about. My definition is important because that is how the real world functions.

Your comment is appreciated because you understand what I am saying.

The Fed is hiking and all those corporate buy backs are about o backfire.

I always appreciate the cogency of your financial analysis. I also appreciate that you’re bold enough to translate that analysis into practical economic prediction, as long as conditions hold (most will not, except in the softest of terms; and the predictive value of others’ is too often based on the stopped-clock principle).

Pet peeve: arguments over the “real” definition of inflation—whether the conventional “general rising of prices” (which the monetarists tend to claim is purely a monetary problem), the Austrian “increase in money supply” or your own (insightful) expansion on the latter. Definitional disputes are tedious and confusing (and, in the end, a bit silly). I suggest simply talking about “price inflation” versus “money inflation” versus “money-credit inflation” (and deflation)—and explaining the differences—rather than simply declaiming that economists of other schools “do not understand what inflation really is.”

With that said, I can’t argue with your analysis—especially if the Fed hikes into “money-credit deflation” because of their fear of “price inflation.”

Rayner, I really haven’t heard or read as you say that “*everyone* is going delinquent on credit card debt”. But what I have heard is that a lot of people are exploiting arbitrage oppurtunity on these 0% APR credit cards contributing to “outstanding debt balance” (reflected in the chart Mish posted at the top of the article).

Also, since the article was focused on credit card delinquencies, then perhaps Mish should have posted the chart from FRED that reflects credit card delinquencies instead of outstanding balance to demonstrate his point and then wait to see what would be audience’s reaction?

And yes, there is small uptick in credit card deliquency rate. But it is nowhere close to 2007/2008 rate. Maybe the folks who managed to buy Bitcoin with their credit cards will soon start to have hardship, but I really don’t know at what scale that would be and when and if they can cover the debt with their Bitcoins.

Not seasonally adjusted:

https://fred.stlouisfed.org/series/DRCCLACBN

As Mish says, it’s the direction not the amount.

Why would anyone be going delinquent when all these 0% APR credit cards abound?

https://wallethub.com/credit-cards/0-apr/

Here are the best 0% APR credit cards:

Overall: HSBC Gold Mastercard® credit card

Runner-Up: U.S. Bank Visa® Platinum Card

Third Place: Citi Simplicity® Card

Initial Bonus: Chase Freedom Unlimited®

Low Regular APR: Bank of Hawaii Visa Signature® Credit Card with MyBankoh Rewards

0% Balance Transfer: Chase Slate®

Student Card: Bank of America® Cash Rewards credit card for Students

Mish, would this chart reflect the credit card deliquincies better – https://fred.stlouisfed.org/series/DRCCLACBS than simply outstanding balances?

That $11.9 billion applies to credit cards only.

Hint: Home Equity Lines of Credit and Overdrafts are counted in the revolving category. It’s not just credit card balances.

https://fred.stlouisfed.org/series/RELACBW027SBOG

Above hasn’t dipped since 2011. It’s now stagnating. If it dips, call a recession.

They are not delinquent if you owe no payment

It’s the direction that matters, not the level

One of the best explanations of the problem I’ve seen! And your definitions are spot on as well.

Which hole of yours did you pull that ridiculous number out of?

Yes, we are definitely at the end of this credit/economic cycle, but don’t expect the Fed to stop tightening until we are already at least SIX MONTHS into the oncoming recession. It will take them that long to get far enough above the “zero bound” so that they can begin cutting rates again, without crashing the stock market and having to contemplate NEGATIVE rates at the bottom of the cycle.

;TLDR credit card debt with intoductory 0% APR should be excluded from that chart in case it isn’t already.

There are a lot of credit cards with 0% introductory APR for 18 months. There are also FDIC insured High Yield savings accounts that yield 1.5% or hort term USGT that yield 2%. Now, it does not make sense for me to pay my credit card bills early in full when I have such debt arbitrage oppurtunity, does it?

If I wanted, I could pay off all the credit cards in full, but it just does not make sense.

Credit card debt is not the debt that I worry about.

Severely delinquent revolving debt is 1% of the total. That’s considered high?