This post is in reference to my previous article Plunge in Interbank Lending: The Straw that Broke the Fed’s Back.

Here is an email a reader Andy sent from the Fred team.

Dear user,

There have been some structural changes to that data in addition to the corrections.

More information can be found at https://www.federalreserve.gov/feeds/h8.html

The Interbank Loans have been discontinued and we are confirming the validity of the last value in that series.

Sincerely,

FRED Team

The chart has been updated one last time, removing the plunge.

Reverse Repo Adjustment

Reader Parker commented:

Through the end of 2017, the Fed tracked “interbank loans” which included “Fed Funds and reverse repos with banks” and “loans to commercial banks”; starting in 2018, the Fed is now tracking “Federal Funds and Reverse Repo” for bank and non-banks together (one number) and breaking out “Loans to commercial banks separately”; as a consequence, it looks like the chart you showed basically had the Feds data feed of Fed Funds and Reverse repo with banks + loans to commercial banks through 12/31/17 and subsequently it is only picking up “loans to commercial banks” because “Reverse repo with banks” is no longer reported as a standalone. I track the Fed H8 report every week which is why I noticed the change in reporting classifications across years.

Fed Funds and Reverse Repo is getting tighter which is still news worth but it didn’t suddenly drop by 90% in a week.

Please let me know any questions – best, Parker

Tightening Analysis

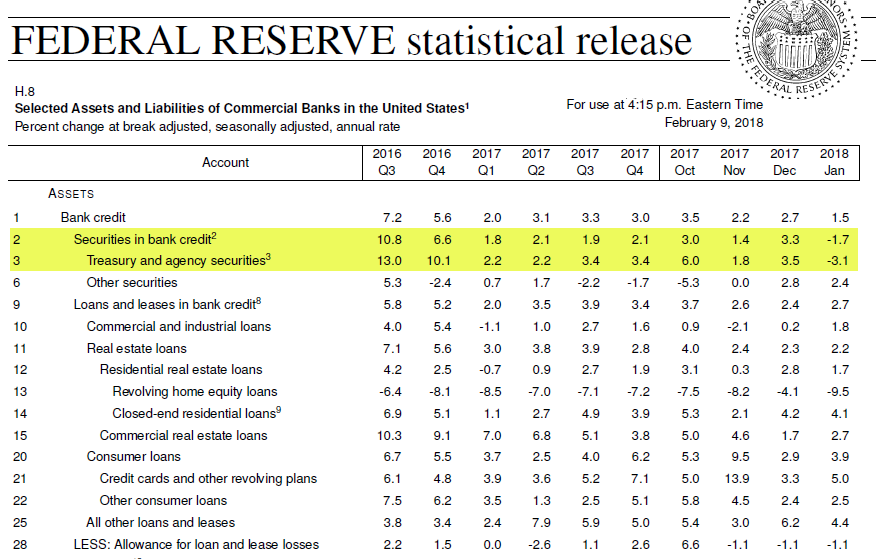

My analysis stands as to what is happening even though the previous chart is inaccurate. Note the lead-in chart for this article. Securities in bank lending took a sudden dive.

My overall message stands as previously delivered, just not the chart itself.

Apologies for the error.

Mike “Mish” Shedlock

link to pasutri-makassar.com

link to obatperangsangmanjur.net

http://vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

link to vimaxmedan.xyz

The rate hikes began with a 105B RRPO seed money, (assumed to reset quarterly or when any a new rate hike is approved) and since then the terms of RRPO have been buried (deep) in their boilerplate as an open window per day, amount in the billions. So there is no real measure of how much the FED is actually paying for these rate hikes. RRPO is QE, coupled with rate hikes has brought the market to a schizoid crisis. Meanwhile the EU runs QE while their LIBOR runs ahead of Fed Rates. If interbank lending is down the Feds RRPO payments will decline as well as bank reserves you would assume. And of course the yield curve dived to new lows, now you can believe one of two things, seeing the brief jump in that number, one that financial repression at the short of the curve can lift the ten year, or that the real lower rates at the short end is asserting itself.That rates are collapsing.

StillCJ, I was about to make a similar wisecrack, but you beat me to it.Maybe Anderson Cooper will spend an hour on it tonight.

This is not a “Fred” decision. This is a “Fed” Decision,

Am I to understand FRED has suddenly decided not to publish historic financial data on interbank loans? This is public information because they are wielding a power of the people and our Congress. What is so important that would cause them to stop publication? To me, this indicates the importance of continuing to publish. We have to pass HR 24, the Federal Reserve Bank Transparency Act (Fed audit) and then the Senate has to come through for we American’s with S.26. It’s passed the House 2x now and failed in the Senate 2x now. It must pass the House again and then the Senate. If they fail, those who voted against it did not vote with the American people… and do not deserve to be continued in office.

The FED stops reporting on things for no good reason.

The banks are so important they are everything. Liquidity is everything to them. What is liquidity? It is what is left over after banks pay their daily obligations. You know, funding. Wholesale funding. I don’t see that there is a problem with liquidity for US banks. It doesn’t matter what Libor is if it isn’t above the Fed Funds rate. Somebody please, figure this out. If there is a liquidity problem, Jay Powell, anti-Yellen or pro-Yellen, doesn’t matter. He will provide liquidity not matter what if banks need it. NO MATTER WHAT. Because banks are everything.

I can’t do it on a moments notice. Probably I can’t do it at all. But it needs to be explained. On the surface this looks like a good change in reporting. Sherlock Holmes would notice that the FRB discontinued M3 because it appears they didn’t want to have exposure to Repos. Something is wrong here.

Raynor, I’m guessing the media is not reporting on it because they are still trying to find someone that can explain to them what it means.

I was wondering why a sudden 90% drop in banking activity had not made it to the media. But activity is dropping nonetheless.