by Mish

Econoday PMI

Growth in Markit’s U.S. manufacturing sample is as slow as it has been in 8 months, at 52.7 and little changed from the mid-month flash (52.5) and April (52.8). Growth in this sample peaked in January at 55.0 and has been moving lower as new orders, also at an 8-month low, and employment have slowed. Production is steady at a modest level and the sample, in a sign of caution, continues to work down inventories. Other details include slowing in both input costs and selling prices and weakness in export sales. This report, of all the private manufacturing reports, has been signaling the weakest conditions for a factory sector that opened the year with promise which it has yet to fulfill. Watch for the ISM report coming up at 10:00 a.m. ET this morning.

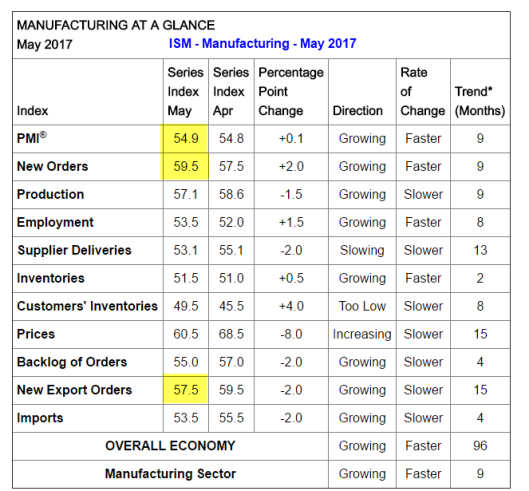

Econoday ISM

May’s composite of 54.9 doesn’t look that strong but the details are very healthy. New orders keep coming in at a very strong rate (59.5), including for exports (57.5), and backlogs are building (55.0). Production is strong, import orders continue to rise, and deliveries are slowing which are all signs of strength. Employment, at 53.5, is also climbing and at a slightly faster rate than April’s 52.0 in what is a positive indication for manufacturing payrolls in tomorrow’s employment report. In a sign of confidence, ISM’s sample is slowly building inventories of raw materials while the assessment of finished inventories is that they’re at just about the right levels. Strength in the government’s factory data have been uneven, unlike the strength of ISM’s sample which is steady and impressive.

Markit Manufacturing PMI Hits Eight-Month Low

Key Findings

- Moderate improvement in overall business conditions

- New orders rise at slowest pace since September 2016

- Input cost inflation eases to six-month low

Manufacturing Purchasing Managers’ Index™ (PMI™) was above the 50.0 no-change value, but signalled the weakest improvement in business conditions since last September. The latest reading pointed to a further growth slowdown from the 22- month high recorded in January (55.0). Weaker new business growth and softer job creation helped to offset a marginally stronger upturn in production volumes.

May data indicated that manufacturing output increased for the twelfth month running. The rate of expansion picked up slightly from April’s seven-month low, but remained relatively modest overall. Survey respondents noted that subdued new business growth and more cautious inventory policies had acted as a brake on production requirements. Reflecting this, stocks of finished goods were accumulated at a slower pace than seen at the start of 2017. Meanwhile, preproduction inventories dropped for the second month running, which contrasted with robust rates of stock building earlier this year.

New order levels increased again in May, although the rate of expansion was the least marked recorded since September 2016. This was mainly linked to subdued client demand. Some manufacturers also cited weak export sales, as highlighted by a slower upturn in new work from abroad than that seen in April.

Diverging Tones

That’s quite a difference in tone between the reports.

The GDP models focus on ISM, ignoring Markit, but Markit’s assessment has been generally more accurate for a long time.

The ISM assessment of first-quarter GDP was a preposterous 4.3% vs Markit at 1.7. I estimated 0.4% but revised the second estimate to 1.1% following construction revisions.

For details, please see …

- Six GDP Estimates (Three Revised Today): ZeroHedge, Mish, GDPNow, Nowcast, ISM, Markit.

- First Quarter GDP Second Estimate 1.2 Percent: Mish vs. Consensus

Here is my second estimate Tweet in advance of the report. Amusingly, I was higher than any Econoday economist’s estimate.

The Econoday consensus estimate for 2nd GDP estimate is 0.8%. For a change, I am higher at 1.1% due to construction. I see no 2nd Q bounce.

— Mike “Mish” Shedlock (@MishGEA) May 26, 2017

I do not have any faith in this ISM report.

Mike “Mish” Shedlock