If you have a mortgage, do yourself a favor and check out if it makes sense to refinance.

My contact at Black Knight pinged me this morning with these observations:

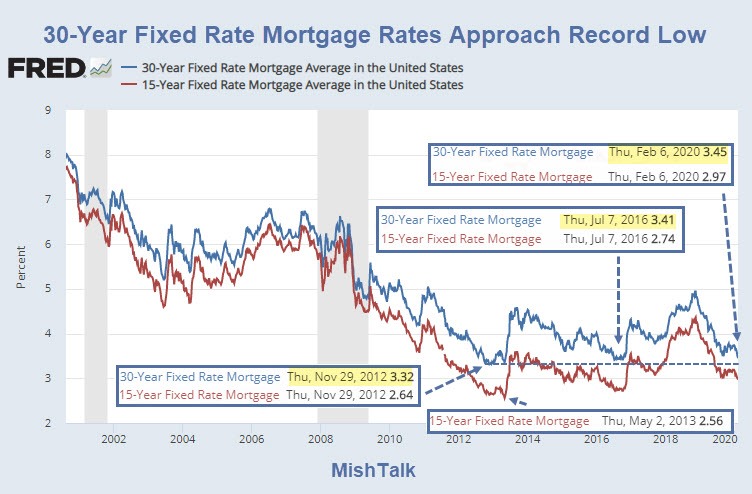

- The Freddie Mac 30-year average is now 3.45%, the lowest level in almost 3.5 years and just 14 BPS above all-time lows.

- This pushed the number of high-quality refinance candidates to approximately 11.3M, for an aggregate potential monthly savings of $3B – both the highest on record outside of a single week last September when rates also fell below 3.5% for a brief period.

- About 1.1 million homeowners could save $500 per month or more through a refi into a new 30-year fixed loan.

December Mortgage Monitor

Here is the charts from the Black Knight December Mortgage Monitor.

The bullet points above are more current than the chart.

As of December, those refinancing s could save $264 per month, for an aggregate monthly savings of nearly $2.5 billion. The aggregate savings is now $3 billion.

Home Price Appreciation

Black Knight comments that low mortgage rates makes home more affordable.

I disagree. Prices have dramatically outstripped wage growth as most looking to buy a home understand.

Refinance Smartly

If you refinance, do so smartly. This is what I suggest.

- Don’t take money out to spend it.

- Don’t extend the length of the loan. Just refinance what is left.

- Do take this opportunity to deleverage.

If you have credit card debt, pay it off, perhaps with some cash back, but don’t rack it up again.

Mike “Mish” Shedlock

“If you refinance, do so smartly. This is what I suggest.”

…

Yes. That is what I did on my only time refinancing home.

However, I can see many others not. I remember the loan officer doing her darndest to get me to refi for a much higher amount (had a lot of equity in home already) as her commission would be higher for a larger loan. “Don’t you want a new vehicle? … Go on vacation? … Fix up the house? … it won’t add THAT much more to your monthly”.

Politely declined. Though (at the time) I felt pretty bold rolling my closing costs into new loan as I was prepared to write a check.

“Prices have dramatically outstripped wage growth as most looking to buy a home understand.”

…

Give that man a cigar!

I guess it will help sell more of those slap’em ups they are building on every square inch around here.

Doesn’t do me any good as I busted buns to pay mine off early between 2005-10 but I’m thinking I might have made a mistake doing that.

Depends on how you feel about your current income situation. I made double payments on a 15 YR fixed pretty much from day one and paid it off last year. At one point I checked into a refinance and the agent basically told me to keep doing what I was doing since it made my effective interest rate 1.1%. And it happened that work was going through a major reorganization and it wasn’t all clear that I wouldn’t be reorg’d out of a job, so the time was right (and I had the money available) to end the mortgage. Immediately took that money that was going to Fannie Mae and shifted it into my 401(k) and a basic savings account for ongoing expenses.

I didn’t intend to pay it off earlier than what would have worked out with double payments, but I’m really happy I did.

Good point that if you overpay each month (I do too), your effective rate is lower. Is that easy to calculate?

Paying off my mortgage. Rather give meself a locked in 3.5% return from the extinguished mortgage than put anymore in Mr. Market.

Careful with using long term debt to pay off short term debt. It’s the “don’t rack it up again” that people have trouble with. Then they do rack it up and now they got more debt all together.. just saying

“Black Knight comments that low mortgage rates makes home more affordable.

I disagree. Prices have dramatically outstripped wage growth as most looking to buy a home understand.”

30-year mortgages make it easier to BUY at home at a given price. As rates fall, it becomes even easier.

But 30-year mortgages also make it easier to SELL a home at a HIGHER price. As rates fall, it becomes even easier/higher.

Ditto for tax deductions, FHA/VA loans, other government programs.

I was offered a 3.09% 10 year fixed rate by my current bank with ABSOLUTELY no closing costs. What the heck is going on here? In 2011 I was turned down for a 5% HARP I refinance due to LTV. What a joke. Im still the same person now as then with a 800 credit score. Anyway, I refinanced with no cash out and will pay down my house very quick.

good move

Good advice Mish.

In 1988 I bought a house for £100K. In the following few years Interest rates fell (or I had some pay rises, can’t remember which) so I increased my repayments & repaid more capital. In 1994 we moved but I sold the house for £76K. Had I not increased the repayments in the previous years I’d have been trapped with negative equity.

“What the heck is going on here?”

Wash, rinse, repeat.

Free mirrors are now being supplied to applicants, to fog.

Looking to generate income? My relatives are building a high quality car wash (automated) that will cost approx. $3.5 million to build. Generates net profit of 30-35%. You have to think outside the box.

Much higher profits if you are laundering your drug profits through it!

Little reminder: refi costs $600 for appraisal which can usually be put on the card. People sometimes forget that.

Interesting! My 30’s at 3.75%, but I’m gonna gamble it’ll all be lower within a few years, because the 0.1% crowd is going to do everything they can to continue the 40-year downtrend in rates, because it pushes their assets up … and then get a 15er.

Yep me too. 3.75%. Get it down to the 2.00% range and then I might be interested.

Fee simple and thankful on two houses here, and looking at the possibility of getting into Russian T bills. Don’t know if it’s gonna be complicated or risky in some way, but… Searching for yield like everyone else.