Radical Overhaul

More hesitant restructuring efforts are giving way to what the @FT and others see as a major overhaul at @DeutscheBank. Big question that’s now on the table is whether #DB can shrink itself to heightened competitiveness and sustainable profitability without a merger of some sort. pic.twitter.com/EdJbFlpNjo

— Mohamed A. El-Erian (@elerianm) July 7, 2019

18,000 Job Cuts

Please consider Deutsche Bank Scales Back Ambitions, Announcing Job Cuts and Reorganization

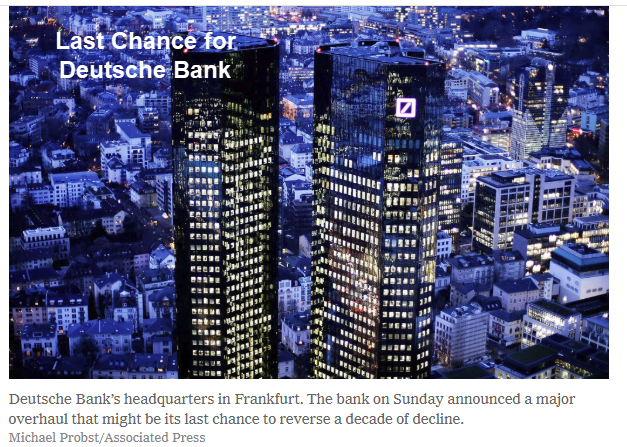

Deutsche Bank embarked Sunday on what may be its last chance to reverse a decade of decline, announcing that it would cut a fifth of its work force and slash operations in New York and London.

About 18,000 people will lose their jobs as Deutsche Bank closes or shrinks operations that sell stocks and bonds. One-third of the management board will leave the bank as part of the overhaul, and more than $300 billion in risky assets will be quarantined in a separate unit.

The question in the months ahead will be whether the turnaround effort by Christian Sewing, Deutsche Bank’s 49-year-old chief executive, comes too late. “We are returning to our roots and to what once made us one of the leading banks in the world,” Mr. Sewing said in a statement on Sunday.

Deutsche Bank’s appetite for risk was perhaps epitomized by its relationship with Mr. Trump. Deutsche Bank continued to lend to the Trump Organization long after other lenders concluded that the risk was too great. In the last year, Deutsche Bank has also been burdened by investigations of lax money laundering controls and has been under intense scrutiny by regulators in the United States and Europe.

Just One Problem

“The plan announced Sunday does not address another urgent problem, the lack of profitable businesses with potential for growth.”

Other than that minor problem, cutting 18,000 is a start of a return to the roots.

To truly return to the roots, Deutsche Bank needs to go bankrupt.

And it should have, long ago. But with incoming ECB president Christine Lagarde poised to slosh around free money, shorts may wish to consider covering.

Zombification is alive and well.

Mike “Mish” Shedlock

There is a lot of political risk to a “foreign” (non US) bank foreclosing on property affiliated with a US president. But 600MM is a rounding error for Deutche bank, even if the properties were worthless (Deutche would recover at least some money by selling the properties, so their loss in the worst case would be less than 600MM).

There was no reason for the infants to bring Trump loans into the discussion other than the NYTimes animosity toward Trump. It is petty, the kind of infantile behavior I would expect from Trump – the grey lady (NYTimes) used to be better than that

The bad bank solves two big problems. DB can offload their bad bets and the ECB will have something to buy, I wonder if the bad loans will have a negative yield to maturity,

The bad bank shifts some bad assets into a different column, it doesn’t avoid massive losses to the German state. Lets stop pretending that the rest of the EU is able, much less willing, to fork over EUR300 billion. Its serious money for German taxpayers.

The ECB is already buying trash and labeling it risk free (eg see Greek government bonds). Draghi announced, at least twice, that the Greek problem had been solved “once and for all” (at least twice). If Draghi’s scam had fixed anything, the ECB wouldn’t be imposing “temporary” negative interest rates to fix a problem that was supposedly solved once and for all.

Putting the bad assets in a separate bucket might allow management to refocus on Deutche’s “core business”…. if only someone knew what that core business was.

Deutche’s historical business model was financing German industry. Bank loans were far more prevalent than equity. But the big companies (the one’s with the best credit ratings, etc) can finance with equity and corporate bonds at much much cheaper rates than Deutche can lend (probably cheaper than Deutche’s cost of funds). The best credit customers don’t need Deutche Bank. Smaller and/or lower credit customers (who can’t borrow on financial markets) would have to pay much higher rates to Deutche, and Deutche would need to completely revamp their credit evaluation system. The risks of lower credit borrowers is very different than the risks of the broad economy including big companies. Deutche has no system to understand how those risks are different, much less manage them.

A bad bank will make German taxpayers really angry (because they will get the bill). Now Deutche is going to charge higher rates to small businesses? (to cover higher credit risk, but the optics of higher rates after getting a bailout…)

The debt will be bought with printed money. It won’t cost taxpayers anything. Maybe a little inflation. Which might actually be welcomed.

Only the debt of the well-connected will be purchased. The ensuing concomitant inflation will be the result of the well-connected’s continued capacity to live the high life, thus keeping various service industry jobs alive which under normal recessionary circumstances would vanish.

Oh! Free money falling from the sky with no cost!

Well, why not print a little more and pay off the Greek debt too? Why should Germany get all the perks?

And what is this nonsense paying off the Greek’s debt, and not also paying off Italy’s debt? Why do you hate all Italians KidHorn?

And if everyone is getting free money from the printing press, than obviously France should get some too. Do you hate French people too KidHorn?

Now that we know we don’t ever have to pay debts, we can spend as much as we want. Sooner or later the debt will get “too big” and we just turn on the printing press. The ECB can’t play favorites and print money for some without printing money for all.

On and on, every member state in the EU will want some of your free money, hot off the printing press. The Euro will quickly be worth the same as a Zimbabwe dollar, because Zimbabwe thought of the printing press decades before Bernanke did.

Mish: “Enough to support eurobonds?”

The reason the eurobond proposal failed 999+ times already is that many EU members cannot (and will not) pay. Is there anyone actually gullible enough to believe the Greek government could make good on their share? Ignore whether Athens would be willing to bail out a French or German bank, Athens can’t even if they wanted to. Its not just Athens in this situation, its most (all?) of the EU.

Eurobonds is just a fraudulent way of saying “make the Germans pay for it, maybe have the UK kick in a little”.

DB’s “bad bank” is rumored to be around EUR300 billion (notional) in assets, which dwarfs the EUR160 billion slush fund Merkel has to cover EU related losses (and some of that 160B was already used).

I think there will be a lot of second order effects coming from Deutche’s retreat from global finance, but there doesn’t seem to be much interest discussing the scenarios here…

DB’s investment bank enjoyed years of subsidisation by the German retail bank and, to a lesser extent, asset management. Both of those weren’t sexy enough ROE-wise to get much respect, though the retail bank was at least recognised as enough of a cash cow to keep it in the brand despite efforts to spin it out during the few years CIB was thriving after Bankers Trust.

CIB got the biggest share of the bonus pool in good years “because they earned it,” and they got the lion’s share of the bonus pool from the still profitable retail bank in bad years “because without CIB, DB is toast.” During bad years the German staff had bonus cuts or “null rounds” while their counterparts losing money in New York and London still got industry-competitive bonuses. After years of being stiffed by management to the benefit of American and other foreign colleagues, it is no wonder there is little love in DB Germany for the investment bank in general and the Americans in particular.

The Americans are resented the most because on top of being pillaged by the American staff, DB is constantly being raped for fines by US regulators. One less cynical that I might suggest JPM et al are using regulators to take out what was once a serious competitor.

Yes, there were plenty of bad actors in DB, and that is why they deserved hefty fines for a host of offences. One of the bigger failings of management was to never once attempt to claw back ill-gotten bonuses that stemmed from the dishonest practises. In that sort of environment, it quickly becomes clear that mideeds are not just going unpunished but are instead rewarded.

There was a point in the early ’00s when DB had a half-billion set aside for retention and a half-billion set aside for severance, and there were more than a few cases where entire teams of investment bankers drew money from both.

The biggest failing of management, a problem that is common to many major German corporates, is that they refused to call the shots and occasionally make an example of an American or a Brit who didn’t run a tight ship. Now, as they whimper out of New York, I can only imagine that there will still be relatively large severance packages from those who should instead have been outright fired. Professional courtesy, from one buccaneer to another.

DB built a huge derivatives book against which vast amounts of capital are tied up, yet booked the profits upfront (and paying out bonuses on the strength of said profits). Many of these derivative trades are long duration (10-30yrs) so will take many more years to roll off, releasing the capital for more profitable deployment. In addition they probably have some toxic legacy GFC positions which are actually eating capital as provisions are taken in bite-sized chunks, y-o-y. No wonder the share price suggests they’re effectively insolvent.

“German taxpayers are going to be really angry at the bill they get for this. “

Bingo

Enough to support eurobonds?

Or more importantly, enough to say: “Screw that clownshow! We’re not paying a Mark more to prop up failed experiments in social engineering!”

Probably not, in the homeland of publicly funded, pervasive indoctrination; but one can always hope sanity, and economic literacy, still has some adherents…..

Good grief these conspiracy theorists at the NYTimes are destroying their papers’ reputation. Deutche Banks’ troubles have nothing to do with Trump borrowing money or not. What a stupid thing for a news organization to write. We get it, you voted for Hilary. You stomped your feet and soiled your diapers and yet still the public voted for the outsider. The grey lady has been overrun by infants.

Mish’s comments about zombie banks is well taken, but Draghi also promised to do whatever it takes… and he ended up spreading the bankruptcy around. Lagarde can’t do anything different.

Can Germany continue to float the follies of Brussels, now that their biggest lender admits to being in serious trouble? The EU could extend and pretend as long as their paymaster (Germany) could cover it. But Deutche Bank is seriously wounded, and Merkel faces full rebellion in her own party.

SocGen already announced they are in similar retreat. BNP too. Macron has to evade yellow vests to get to his office. Italy already elected anti-EU government and is preparing to issue their own currency. Brexit seems to be happening in slow motion, but England can’t afford to bail out Brussels even if they stayed.

Brussels abused Deutche Bank (and Germany in general), now Brussels’ paymaster is in trouble which puts Brussels in trouble. This is true no matter what Farage or Johnston or anyone else in London dithers on about.

German taxpayers are going to be really angry at the bill they get for this. It won’t help Merkel or her supporters, or her puppeteers in Brussels.

And secondly… does this not make Deutche Bank a forced seller of equities? Will Deutche traders, who are getting the ax, hold out for best prices as they close their positions?

Richard Bookstaber wrote a long article about when Travelers / Salomon Bros decided to exit prop trading. Travelers told the news papers (and competition) before they told their own trading desk or risk group. I don’t remember where to find that article, but Bookstaber said it made for chaos both at Solly and others who had similar trades on.