by Mish

“Gains were broad-based in the month led by the ISM new orders index and including, as always, the interest rate spread where short-term rates are unusually low. The LEI has been very solid and continues to point ahead to rising economic strength.”

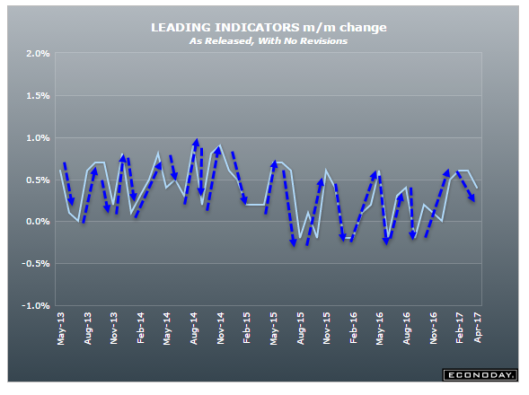

Leading Economic Indicators Rise Again

The Conference Board press Release says the LEI Index Points to Continued Economic Growth Through 2017.

“The March increase and upward trend in the U.S. LEI point to continued economic growth in 2017, with perhaps an acceleration later in the year if consumer spending and investment pick up,” said Ataman Ozyildirim, Director of Business Cycles and Growth Research at The Conference Board

Useful Prediction

The economy will perhaps accelerate if consumer spending and investment pick up.

That’s useful information since I thought it was a given that the economy wouldaccelerate if those things happen.

Thank you, Conference Board for this important clarification.

Leading Index Components

The above from the Conference Board Description of Components.

Bear in mind, standardization factors are not the same as weights.

While some of those indicators may actually lead something, especially at the bottom of the cycle, it is debatable if they lead anything now. Other components, notably the stock market, don’t lead anything. The stock market is a coincident measure of attitudes towards stocks.

The interest rates spread is nearly always positive except right before a recession. I would suggest, to no avail that the direction of the spread (widening or narrowing) is what’s really important.

I would also suggest housing starts, not permits are what to watch. Watching permits is sort of like watching a leading indicator to a leading indicator, but not quite. Permits are a measure of builder sentiment of expected activity and thus highly likely to be very wrong at turns.

Revisions

The above chart looks impressive but the components and weights are constantly adjusted so the curves match what happened. There was a major revision in 2011.

Note the sharp turns at the bottoms.

Soft data is far more likely to be correct at the bottom of economic cycles than the top.

Mike “Mish” Shedlock