Edwards Comments

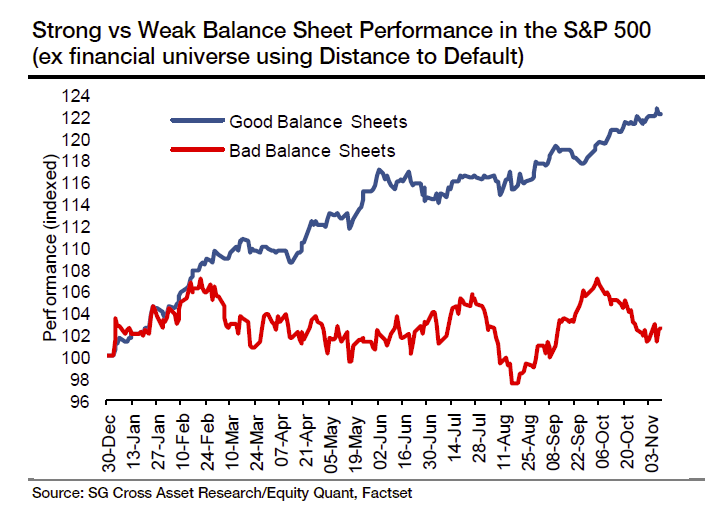

“With bullishness sentiment at extremes, is it significant that my colleague Andrew Lapthorne noted in his widely read “Global Market Arithmetic” that despite the overall equity market continuing to hit all time highs, there has been a clear divergence in performance between companies with highly leveraged (bad) balance sheets and those who do not. Is this a straw in the wind that a bear market is arriving far sooner than most investors had anticipated? It might be.”

“And we think the high yield corporate bond market should have been revolting against balance sheet debauchment some time ago. That would be the normal state of things with net debt/profit ratios so very high (see chart below but note bottom-up data shows a far higher peak than this top-down Fed data but peaks normally occur as profits fall in recession).”

“We continue to highlight that it is not QE per se that has caused US companies to debauch their balance sheets. Japan is awash with QE but balance sheets are in relatively good shape. The problem in the US is how QE has worked its way through the financial complex.”

Mish Comments

US net debt to total assets is not quite at the 2008 peak. But what will those assets really be worth in the next downturn?

Also note that a handful of genuine cash cows such as Apple and Google distorted the debt ratios.

EBIT vs Interest on Debt

Here is one more chart from the “Global Market Arithmetic” report that Edwards mentioned.

Lapthorne notes that while average interest as a percentage of Earnings Before Interest and Taxes (EBIT) is healthy, the bottom 50% of the S&P isn’t.

This is at a time when interest expense is at or near record lows, and profits at or near record highs.

Lapthorne concludes, and I agree “It is difficult to envision a scenario in which this ends well.”

Mike “Mish” Shedlock

Professor Cowen missed the point on the bases for corporate tax cuts. He says: “When companies have more “free cash” at hand, they tend to invest more, and this effect is distinct from any effect of the tax cut on expected rates of return…. a “giveaway” to business…is precisely the mechanism that tends to boost investment.” He admits an effect from expected [after tax] rates of return but suggests simply giving corporations more cash is the main effect. The expected risk adjusted after tax return on investment (ROI) may not be the only consideration in investment decisions but it is certainly the primary consideration for well-run companies and for investors considering investments. Relative ROI of alternatives also affects decisions on where the investment facilities will be physically located and deal structure. Investment options with attractive ROI will tend to get funded, either from available cash, by borrowing, or if need be by selling additional stock.

The corporate tax cut is expected to increase investment by increasing expected after tax return on investment. However, a primary objective is to influence both where the investment is located and where the corporate owners of investments are located (domiciled for corporate tax purposes). Specifically it is intended to increase the probability that new investments will be made within the US and to increase the probability that investments will be owned by US domiciled companies.

Professor Cowen missed the point on the bases for corporate tax cuts. He says: “When companies have more “free cash” at hand, they tend to invest more, and this effect is distinct from any effect of the tax cut on expected rates of return…. a “giveaway” to business…is precisely the mechanism that tends to boost investment.” He admits an effect from expected [after tax] rates of return but suggests simply giving corporations more cash is the main effect. The expected risk adjusted after tax return on investment (ROI) may not be the only consideration in investment decisions but it is certainly the primary consideration for well-run companies and for investors considering investments. Relative ROI of alternatives also affects decisions on where the investment facilities will be physically located and deal structure. Investment options with attractive ROI will tend to get funded, either from available cash, by borrowing, or if need be by selling additional stock.

The corporate tax cut is expected to increase investment by increasing expected after tax return on investment. However, a primary objective is to influence both where the investment is located and where the corporate owners of investments are located (domiciled for corporate tax purposes). Specifically it is intended to increase the probability that new investments will be made within the US and to increase the probability that investments will be owned by US domiciled companies.

Corporate balance sheets are in terrible shape, other than for a few gigantic, monopolistic companies. In the next crisis, I think we will see widespread corporate bankruptcies. And I suspect events will most likely move too quickly for the Fed to effectively counter them. But treasuries will be very popular! Buy the 10 year note now at a healthy 2.3% yield or buy it later at a negative yield – the choice is yours.

“For “the good of the country”, of course.” …. Will we able to get rid of these charlatans when the market seizes this time or again will the slippery eels manage to wriggle away and make out that it is not because of them. It is time to get rid of these creeps or at least remove the tools of money printing and interest rate from these no-gooders if America wants to be great again. Keeping these cheats in the saddle is akin to setting yourself on fire… without your knowing it – after all it is for your own good.

“For “the good of the country”, of course.”

Fed purchases and buybacks are a drop in the bucket compared to global investment. With the rest of the world (periphery) collapsing ahead of the US, expect the fundamentalist to continue to be wrong, as capital flows into dollar-based assets that will cause the DOW to double by 2020. Few question how overvalued and “risk free” govt bonds are when stocks crashed in the past. Why would the same people question how over valued stocks are when the soveriegn debt bubble pops, which are backed by nothing but the hot air of career politicians?

For “the good of the country”, of course.

“It” ends with the Fed printing money like crazy and using it to “bail-out” (and wind up owning) practically everything.