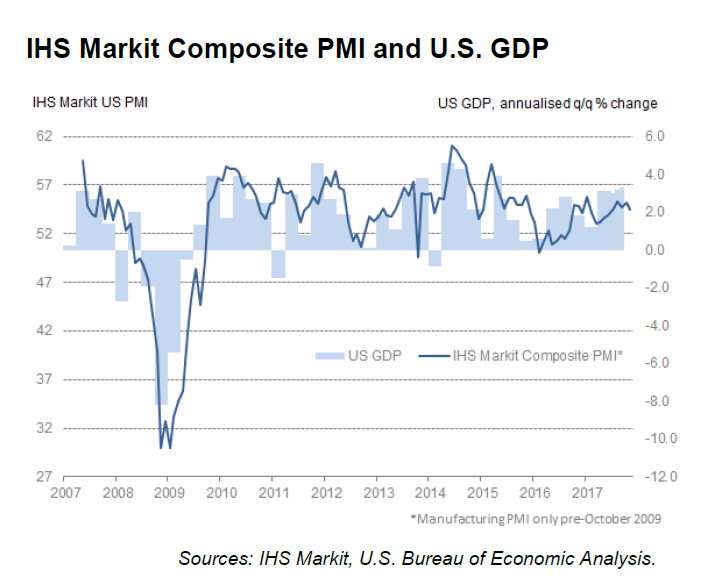

Business activity growth in the US eased in November according to the IHS Markit U.S. Composite PMI™.

Key Findings

- Service sector output expansion softens to five-month low

- Upturn in new business accelerates

- Business confidence slips to joint-weakest since February

Although output growth eased slightly to a five-month low, the upturn in new business accelerated and was solid overall. Employment growth meanwhile reached a three-month peak, which helped alleviate capacity pressures. In line with this, backlog accumulation softened to a five-month low. Inflationary pressures intensified with both input prices and output charges rising at quicker paces.

Average prices charged for services increased further in November, with the rate of inflation accelerating. Panellists stated the rise was due to higher input costs which were passed on to clients. Cost burdens faced by service providers rose at a strong rate that was slightly below the series trend. Panel members noted that the increase in input costs was primarily due to higher goods prices.

Chris Williamson, Markit Chief Business Economist Comments

- “The slowest growth of service sector business activity since June, alongside a slight dip in the pace of manufacturing expansion, means the November PMI surveys registered a modest cooling in the overall rate of business growth. Mid-way through the fourth quarter, the surveys are still pointing to a reasonable GDP growth rate of approximately 2.5%.”

- “The surveys’ employment indices are meanwhile pointing to solid non-farm payroll growth of circa 200,000 as companies continue to take on staff in encouraging numbers to meet rising order books.”

- “Disappointingly, optimism about the year ahead deteriorated as companies grew increasingly cautious about the outlook for 2018, suggesting risk aversion may start to rise, which could hit hiring and investment. However, for now, businesses generally remain in expansion mode and the upturn shows few signs of losing momentum to any significant extent.”

- “In terms of prices, the upturn continues to show signs of gradually feeding through to higher inflationary pressure. Average selling prices for goods and services showed one of the largest increases recorded over the past four years, linked to rising cost pressures.”

Stagflation Lite?

This is a stagflation lite scenario if two conditions happen.

- The economy enters recession

- Rising inflation takes hold

I expect the first condition, not the second.

The yield curve flattened again today and the flattening is accelerating as the economic bubbles continue to expand.

Rational individuals note a “Carrot Top” and a Generational Chance to Sell Equities.

When the current bubbles burst, treasury yields are going to crash, and from already amazing low levels.

For further discussion, please Yield Curve “Conundrum”: Blame Japan for Flat Treasury Curve?

Mike “Mish” Shedlock

The fed will need to start an aggressive rate increase cycle similar to 1994-1995 where rate increases need to be 50bps and one 75bps rate increase may be needed next year and in 2019

Rents are the #1 BY FAR costliest budget item in most folks budgets, and they have been going THROUGH THE ROOF. But move along children, nothing to see here))))

But most millennials have mommy and daddy to pay that and can coast on parents health insurance until age 26

The only concerns businesses have and what may slow the economy is the dearth and lack of skilled workers or any workers for open job openings. We aren’t talking about $12 hr warehouse jobs but jobs in Finance, Accounting and IT that pay in the six figures fail to get any applications or candidates when posted on Indeed.com. In cities like NY and Boston that have torrid job markets, it is hard to find most white collar corporate positions because there are simply no candidates

Rents are the #1 BY FAR costliest budget item in most folks budgets, and they have been going THROUGH THE ROOF. But move along children, nothing to see here.

Don’t forget rents…some areas rents have been inflation at 6-15% a year

“Has anyone checked home prices, heatlh care, college, food or gas?”

Not surprising prices will rise as we are forced to “buy Amerikan” or pay tariffs on imports.

“The yield curve flattened again today and the flattening is accelerating as the economic bubbles continue to expand.” Should definitely be an interesting few weeks for curve watchers with the fed supposedly raising rates next week. The feds Christmas present of an expected quarter pt. increase could provide some unexpected surprises for some.

True CPI is deliberately underestimated by the govt and I guess the sheep eat it up as fact. Has anyone checked home prices, heatlh care, college, food or gas? No one in their right mind should believe the CPI is under 2%. I do not understand why someone hasn’t pointed out the emperor has no clothes. The failure of the financial press to question this garbage is given credibility to the propaganda coming out of the monetary politburo on Eccles street.

Even with 5% CPI and 2.5% yields its nominally not a deal breaker, while for those who are hedged for inflation it represents a %100 gain over yield. People say why own TIPS, well not because inflation will be higher, but because rates are going to (stubbornly) remain at some multiple lower to CPI. Not like owning FAANG stocks of course.