by Mish

The latest non-manufacturing ISM and Markit PMI readings, out today, provide another example.

The payroll report for May was a near-disaster but one would never know it from the ISM report. Actually, one would never know anything from the IMS reports, they have been so overoptimistic for so long.

Econoday Take on ISM

The Econoday take on the ISM report was amusing.

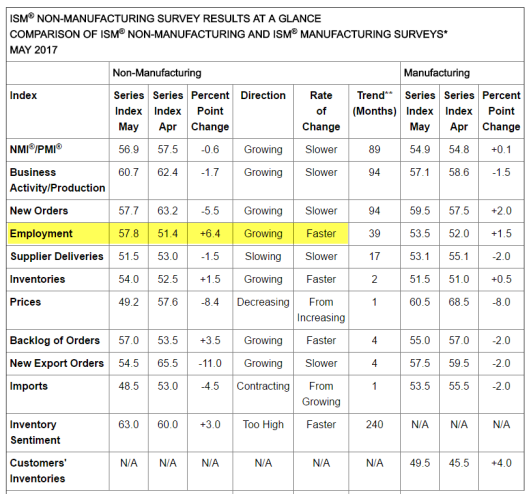

The ISM non-manufacturing index comes in just about as expected, at 56.9 vs Econoday’s consensus for 57.0. This is a very solid rate of growth that reflects strength in business activity (output), at 60.7, and new orders at 57.7. ISM’s sample reported noticeable strength in employment which however, at 57.8, contrasts with last week’s weak employment report for May. Backlogs are also unusually strong in the May report, at 57.0, which helps explain the month’s strength in hiring. The sample is building inventories in a sign of confidence with input costs, which had shown prior pressure, now flat. But this report is far from flat, continuing to point to rates of growth that the actual economy has failed to match.

Econoday Synopsis

- The ISM employment data does not match actual weak hiring in the BLS employment hard data.

- Nonetheless, strong backlogs explain the strong hiring (that did not really happen).

Got That?

IHS Markit Services PMI

Key Findings

- New business grows at fastest pace since January

- Business activity continues to expand at solid rate

- Job creation accelerates to three-month high

Hiring Trends Accelerate

The trend of job creation, which began in March 2010, was extended in May. The rate of payroll expansion accelerated to a three-month high. Panelists commonly attributed the rise in staffing levels to new projects and higher overall business activity.

On the price front, the rate of input price inflation softened fractionally from April’s 21-month high. The pace of increase was broadly in line with the series average. Anecdotal evidence generally associated increased cost burdens to higher prices for goods purchased, as well as wage rises.

Chris Williamson, Markit Chief Business Economist, Comments

- “Although service-sector business activity picked up in May, the PMI surveys for manufacturing and services collectively indicate only a modest pace of economic growth so far in the second quarter.”

- “Historical comparisons with GDP indicate the PMI is signaling second quarter GDP growth of just over 2%, suggesting there may be some downside risks to IHS Markit’s current forecast of a GDP growth rebound to just over 3% in the second quarter.”

- “However, the key message from the PMI is that the economy is enjoying steady, albeit unspectacular, growth, and that the pace of expansion has been slowly lifting higher in recent months.”

- “Hiring meanwhile remains on a firm footing, with the survey’s employment indicators running at levels consistent with around 160,000 jobs added to the economy in May.”

- “In another sign of the economy’s underlying steady expansion, average prices charged for goods and services is running at the second highest in almost two years, indicating that rising demand is helping restore some pricing power.”

Williamson questions the validity of his own model’s GDP estimate. That a smart move given the anemic hard data reports all month.

Econoday on Markit Services PMI

The Econoday take on PMI Services also reflects on strong hiring.

Moderate is the message from the PMI services index which finishes May at a lower-than-expected 53.6, down 4 tenths from the mid-month flash but up a solid 1.1 points from final April and up 5 tenths from April’s flash. Most readings rose back to strength early in the year including new orders with backlog orders showing their first build since January. Employment is at a 3-month high with optimism on the general outlook, however, remaining subdued. There are badly needed signs of inflation in the report with input costs on the rise and selling prices also moving higher. This is a positive though far from robust report.

The Econoday parrot continues to press for more inflation as a benefit. Parrots don’t understand economics. Most economists don’t either.

— Mike “Mish” Shedlock (@MishGEA) June 5, 2017

For more on the “robust” jobs creation thesis, please see Payrolls “Unexpectedly” Weak, Negative Revisions, Earning Poor: What Happened?

Mike “Mish” Shedlock