Expectations vs. Reality Gap

The Expectations vs. Reality Gap is huge when it come to millennials desire to own a home.

In a nationwide survey of nearly 7,000 prospective homebuyers, Point2 found that 74% of the Millennials who are interested in purchasing a home would like to do so in the next 12 months. However, 88% of respondents between 25 and 40 years old have significantly less in savings than the average national down payment amount, which is $62,600. Moreover, 14% of the Millennials surveyed stated that they hadn’t managed to set aside anything at all, meaning that the desire to buy a home might be in conflict with Gen Y’s budgetary realities.

Time Needed to Save a Down Payment

Click on the above link for an interactive graph of cities.

Assuming a saving rate of 8% and a 20% down payment, in Austin it would take 11.8 years to save a down payment, Chicago, 9.6 years, Denver 12.8 years, Los Angeles 25 years, San Francisco 18.3 years.

Budget Realities

- Most Millennials tend to greatly underestimate the amount of money they will need for a down payment.

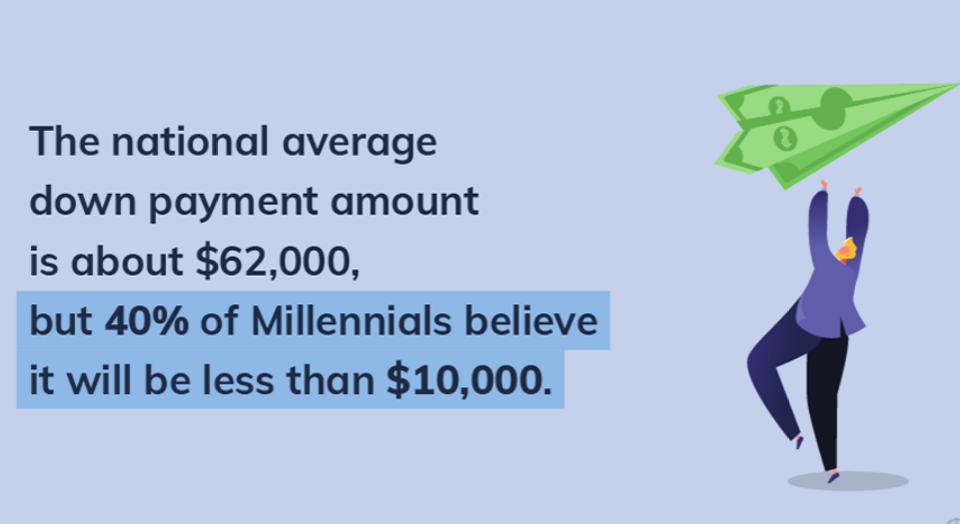

- The national average down payment is about $62,000, but 40% of Millennials expect it to be less than $10,000. What’s more, 61% of young people have less than $10,000 in savings. Of those, 14% have no savings at all.

- The average savings rate in the last decade was 8%. And, although personal savings went through the roof in April (reaching 33.7%) one month of extraordinary budgeting may not move the needle.

- Considering savings rates, median incomes and median home prices, the time needed to save for a 20% down payment in the 100 largest U.S. cities varies significantly: from 10 years in Los Angeles and around nine years in Long Beach and Oakland, CA to a little more than two years in cities such as Buffalo, NY, Cleveland and Toledo, OH and Pittsburgh, PA.

- Perhaps unsurprisingly, the only large U.S. city where Millennials could save for a down payment in less than two years was Detroit, which makes this market the most attainable.

I somehow doubt that Detroit, Pittsburgh, and Toledo rank high on the dream list of cities for millennials to live in.

Mish

For me people (specially millennials) need to start doing investments in reliable cryptocurrency sites like http://www.mintme.com, there they can manage their accounts, and buy and sell any kind of cryptocurrency at any moment

A life of enslavement to government debt and societal norms that puts them deep into debt after graduating high school as they chase paper.

borrowing money for personal shelter is a scam. investment property is a different story.

“The crisis consists precisely in the fact that the old is dying and the new cannot be born; in this interregnum a great variety of morbid symptoms appear.”

Antonio Gramsci

Now that I’ve retired early I’m taking my small divested fortune and moving back to Southern Illinois and get a little place for cheap and put on the money on auto-pilot and live modestly and donate the balance of the interest to charity.

Not surprising, I have spoken with many millenials that were more adept at insulting people that have experience in their fields than actually getting into the arena and competing.

Its hard to have any knowledge at all when you dont go out and obtain it.

Austin…..you can find a starter home that is FHA qualifying out in Round Rock or some other burb for about $275K…and with a first time buyer FHA lets them get in for 3.5%..which would mean a downpayment of less than 10K ($9625).

The median price is skewed by neighborhoods like mine, where the $1M mark is getting to be the new low end….3X what I paid in the early 90’s. Downtown condos are super expensive, especially for what they are…..not sure who buys those…but lots of people, apparently.

In my experience, millennials tend to be great savers…..and fairly financially adroit, many of them. They have come of age in a time when you can’t just fall off the turnip truck and do well.

My kids are all millennials…my eldest (now age 37) has been in her first house now for five years….she bought her house for $195K in 2015…To give you some idea of price movement, I bought the house next door to hers in 2018 for $259k. They are comparable.

The $62K downpayment number you cited is skewed…by people moving from high end markets to a lower one and moving up to more house…people further along in life. Also by the highest end cities.

Home ownership is still a good idea…but honestly….my experience has been that lower end homes appreciate faster than high end ones……in a market like Austin, a high end home is a trophy more than an investment.

Interesting that you looked at Corpus Christi. That town is a real sleeper. I would retire there…or at least buy something there with that in mind for the future…… if the missus would hear of it. Low growth has kept prices there very affordable…..not much gentrification yet….lots of potential. A world-class marina downtown that is so cheap it makes Florida or the West Coast look crazy in comparison.

Texas? Humidity and rain? Ick!

Yes, please stay in Cali. It’s horrible. 🙂

Well, Texas property taxes are horrendous compared to Florida. And Florida also has no state income tax and generally lower sales taxes. Plus, Corpus, like the rest of Texas, is vulnerable to cold spells in the winter, which are much less severe in Florida.

Corpus Christi property taxes are .65/$100. That’s more than 25% less than the Florida average of .98/100.

The average nighttime temp in CC in January, the coldest month, is just under 50 degrees F.

But by all means, please stay in Florida. 🙂

Does this really matter? Millenials get the downpayment from their Boomer parents, who have done massively well in the stock & housing markets. Just like the stock market, housing will keep going higher.

And before you judge, I’ve been largely out of the stock market since 2009 and I’m relatively young–worst decision I’ve ever made. I’ve been long gold since 2005…OK decision. I’ve been listening to the likes of Hussman for a decade now due to his analytical analysis (I’m a scientist). But, maybe I’ll mark the top of the stock market as I’m seriously about to dump many hundreds of thousands into it now after having missed out on a five fold gain over the last decade. But, if the Federal Reserve couldn’t stand to see Lehman fail, why would they let the (much much bigger) stock market fail. They won’t.

“Does this really matter?”

Nope, until it does.

If your parents were the type that were invested in the market since the last collapse (perhaps even despite your scientific arguments) “because it always goes up”, then you could view your conservative position as counterbalancing hedge for the family fortune. Picture if you went all in back then, but then Mr. Market showed up for good. Thanksgiving family dinner wouldn’t be as fun. Instead, you, the younger guy took the hit and is all the wiser, while your parents are brimming with glee because they are “geniuses” which is what one should want for their parents in their golden years.

Hussman returns have failed to impress for years. He is more about trying to be right then about the returns. Hussman failed to understand that liquidity matters and that the Fed can create money longer than you can stay solvent. The stock market and real estate market are stores of value because they will never be allowed to fail.

I got out of stocks for good in 2008…..I also missed a good run, but the market now is just as unstable as it was then. You might do very well, but I think tangible assets make more sense….and gold is not the only tangible asset. If I were going to own stocks, I certainly would not be “all in”.

You don’t have to punish yourself for missing a rally. Dow 29K doesn’t seem like the time to buy in. While it’s true that the Fed will CTRL+P forever, there will be corrections like there were earlier this year. Remember, only seven months ago the Dow was more than 10K lower than it is today.

Also important to remember that society isn’t meant to be this rigged without serious social repercussions, so it’s not a bad idea to keep that in mind whether investing or preparing for what’s bound to be a rocky future.

They learned nothing from the housing bubble.

Who learned nothing?

Banks learned they can get bailed out for making bad loans.

Delinquent/insolvent borrowers learned they can live rent free for 3 to 5 years before getting kicked out with a $20K “don’t tear out the piping” bonus.

“Landowners” renting from the bank learned they can continue to collect rent off “their property” and not remit payments to the bank for 3-5 years.

Prudent savers renting an apartment until they feel they could afford something they could pay off in their lifetime learned they are the bane of society.

RunnerDan, exactly right! What I learned, was that if enough people get into trouble, regardless if it was the result of illegal activity (such as “homebuyers” lying about their financial situation to buy a house using no money of their own and then being victimized in the media as a “struggling homeowner”), they will get bailed out and even left off far better than before. Living in California, many of my neighbors gamed the system just like you stated—living rent free for many years and banking the money. But most got only $7k as an incentive to not rip out the appliances by the time they were finally evicted…

Uhh..millenials were still in college during the last real estate bubble. Most of them were not even working.

I somehow doubt that Detroit, Pittsburgh, and Toledo rank high on the dream list of cities for millennials to live in.

They never will be. This is why more of the population is fleeing south and southwest. But even these places are becoming more expensive. My parents live in a Dallas suburb where the value of their home has doubled in the last 10 years. It is an old house in a below average school district. It is reminiscent of California in the early to mid 90s where even below average places boomed. In the end there is more money floating around to be lent to investors and above average speculators. Speculators can and do make money in real estate everywhere. Millennials should prepare to rent for a long time.

CA resident since 1988.

Early to mid 90s was a housing bust. They were giving houses away.

You mean late 80s or early to mid 00s.

Are these numbers for 1st time buyers? or all buyers? Because if they include all buyers, many would be rolling over profits from selling their existing homes. Not a good number to go off when comparing to 1st time millennial buyers.

The American Dream is now the American Fantasy.

What is the required down payment on the average used van?

Nebraska has a special finance program for first time buyers, called NIFA. The required downpayment is typically $1,000. For people with income less than 50% of the average income, they provide a grant of $5,000 which does not have to be paid back.

Other states probably have similar programs to help first time buyers.

But…but you have to live in Nebraska.

“…they provide a grant of $5,000 which does not have to be paid back.”

Nice! I’m sure the average Joe who isn’t “poor enough” to qualify is thrilled.

That’s a problem with the stupidity of the ad hoc welfare system we have. Made of pieces at the county level, state level, and national level, and each passed independent of the others. The net effect is numerous welfare cliffs, where people are better off making less, rather than more. We know that decreasing marginal rates does in fact motivate people. Why not apply it to lower incomes as well as high incomes? As an example, create this program so that the grant is $6,000, less 10% of your income.

“As an example, create this program so that the grant is $6,000, less 10% of your income.”

Well, that sounds like a good idea. The problem is, helping one group always comes at the expense of everyone else. That’s a physical law that can’t be changed. Really, the best way is the fair way which by definition is the government is out of the market place. Although with housing, prohibition of central bank intervention must also be specified in that definition.

I don’t think it’s well understood how much of the housing subsidy is/was aimed at leveling the playing field for minority buyers. The government keeps trying to make it easier…but lenders are adept at finding ways to exploit that segment no matter what the government tries to do.

I am torn….I’d like to see all people with a decent roof over their head……and a nest egg of wealth….and I do think a house is still a small but important way to build wealth. Perhaps the most common way we’ve had, over time. It doesn’t always work out well, but it can.

But the system of hand-outs does screw some people who don’t qualify, you are right about that..

And the way it worked out in 2008, a very large fraction of people who lost homes in the crash…turned out to be African-American…..for several reasons…but the primary one was because they were over-leveraged. This happened at least partly because the government made it possible with low down payments……but it was also due to predatory lending practices that put people who were financial babes-in-the-woods into ARM’s and above-market-rate mortgages,

“I don’t think it’s well understood how much of the housing subsidy is/was aimed at leveling the playing field for minority buyers.”

Part of the “systemic racism” that does not get discussed…

Exactly.

No social experiment that has been tried to date…to provide racial justice by tipping the scales….. has come without at least some unintended consequences. Nobody on the liberal side ever wants to look at that part.

In coastal California you might be able to find a house for less than $600k which means a down payment of $120k. The absolute minimum property tax on this house would be $6k (assuming no local taxes such as school bonds, improvement districts, etc.) or $500/month added to your mortgage payment.

A lot of false information here Mish. For example, in L.A, not everyone buys in the city of L.A. proper. Far and away most commute to areas like Santa Clarita, Riverside, even Temecula where home prices are much lower. Homes in L.A. are easily over $1 Million versus suburban homes from $350k to $750k depending on area.

Also, who puts down 20%? Most put down 3.5% and take a 0.5% increase in their interest rate instead of paying PMI. Then a couple years later refi to lower their rate and remove that “penalty”.

Home buying isn’t for everyone, in all cities. It’s a lot easier in the Midwest than it is on the coast, and not everyone will be buying on the coast. But if you take a typical professional couple, each bringing in $60k to $120k depending on profession, you’re talking a household income between $120k and $240k. In my circle that’s pretty common, but I also work for a huge company and attend a large church. In my neck of the woods, anecdotally, most people I know are homeowners and this is the 15 Freeway corridor, basically Fontana/Rancho, Eastvale, Corona/Riverside.

“Also, who puts down 20%?”

20% down with a 28% debt-to-income ratio on a 30 Year fixed seems like a quaint, old fashioned notion indeed!

My house was built in 1928… SoCal

Cool! I’ll bet its a craftsman. Those are gorgeous. Give me one of those with a couple jacarandas on the boulevard (not near the driveway though) and orange and avocado trees in the back, and that is paradise.

What really amazes me is the low median home price !….Here in Belgium, or Flanders rather, it is 260K euro on average, near Leuven, where I live you can buy nothing below 400K…

It varies greatly by location. In some cities in California you are looking at >$400,000 for a starter home. In other places, starter homes are much cheaper, especially in a town like Detroit where they had a huge outflow of people, so large that they ended up demolishing large numbers of houses.

I dont think the above list in the article is the norm, I live one east coast, Maryland and decent home prices start around $300K, you can get a good house in $300-500K range.

I’m from northern Europe, living in the US for the last 20 years.

What never ceases to amaze me is the shoddy quality of houses here. Instead of with bricks and concrete they build with lumber. Then they’re surprised there are so many fires, that a minor hurricane or tornado blows them over or they have to essentially raze the building and build new every 30-50 years.

And then there are the useless heating systems in most of the US: to heat they use the HVAC to blow hot air – totally unhealthy and uneconomic, but of course cheap to build.

In northern Europe houses are built to last 100+ years and have decent heating system based on some form of radiators which also heat the walls behind them and so create reflective heat that lasts long and feels comfortable; very different from the dusty air being blown around here that gives you a hot head, cold feet and sick lungs.

The difference in building quality explains a large part of the difference in price.

Not completely true.

Many houses are built to last 60 years, but are significantly run down after 30.

Northern Europe is very humid in the winter. Using radiators when it’s -30° would mean your house is bone dry (most HVAC systems have built in humidifier). Many houses here have poor insulation which is hard to ameliorate (no studs, bricks), and which means that your heat is more from radiation than from the air (uncomfortable), and many houses have huge temperature differences between the floor and the ceiling. Even in the 80’s they were still building houses here with substandard insulation and single pane leaky windows (it’s less cold in NW Europe, though Eastern Europe and Scandinavia have deeper winters). There are sitll plenty of houses here with a stove instead of central heating. Personally I always found HVAC more comfortable.

New homes here prefer floor heating which is much more comfortable. Older buildings often have the radiators and piping projected out in front of the wall instead of recessed into the wall. Besides being ugly, it often severely limits your possibilities to place cupboards, furniture, a piano, or a bed.

Don’t mean to contradict the comment completely, but as always, reality is more complicated and differentiated.

Typical Nordic/Northern European arrogance. Wood construction does not equate to ‘shoddy quality’ it is simply done in a different way. Most construction in Mexico is done with brick and concrete and many of these houses are likely to come tumbling down with a mid sized earthquake. I’ve seen plenty of them with massive cracks on walls. A wood house can often better withstand some of the shaking with out serious damage when an earthquake hits (I live in California) precisely because it has some sway. Webej also makes some good points about the differences.

So is this guy from Ask This Old House TV series. I can’t find a link where a building trade show in Germany features houses like from a space age. If you can peek into a prefab factory in some YouTube video, you will notice equipment made in Germany or such.

Houses here are not only shoddily built; they are also expensive due to relentless printing to prop up the financial casino.

American houses are built to make money for builders. Period.

We put the thermal mass (brick) on the outside….and the insulation….on the inside….exactly the reverse of what should be done to conserve energy, no matter what the climate.

My house, which is lovely and has a fine view…Is an energy hog that uses about 100 kWh/day on average in this hot climate….that alone is fairly shocking. What can I say, I bought the house many years ago, and I was less well-informed about such things. I’m not proud of the waste.

Millenials also under-estimated the cost of their college debt