Those waiting for a full inversion before worrying about recession can start worrying today.

Yield Curve Spreads

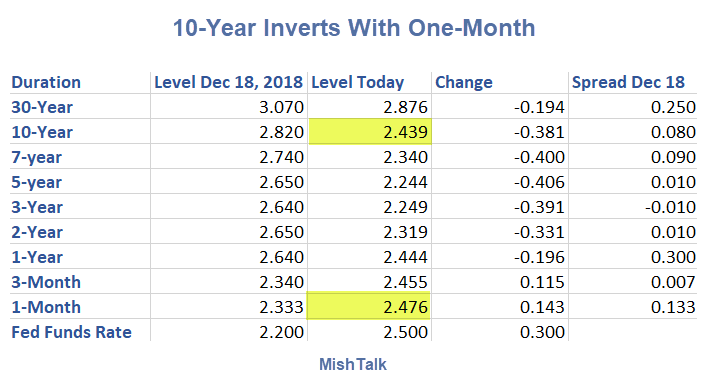

There are too many inversions for me to draw all the arrows. Suffice it to say the 10-year note has now inverted with the 1-month T-Bill.

And from the 5-Year Note through the 1-month T-bill, every duration level is inverted with every duration level beneath it.

We have near-full inversion except for the 30-year long bond.

Recession Time!

OK, the whole 10-year/2-year inversion thingy seems a lot of baloney to me. It looks far more like the 2 year treasury reacts to the Fed Funds rate far more closely than the 10-year rate – indicating that the volatility for the Fed Funds rate is far greater over 10 years than it is over 2 years, and thus the rates are impacted appropriately (i.e. no shit Sherlock).

So you either accept that: (1) the Fed triggers recessions by raising rates; (2) the Fed mitigates the extremes in upcoming recessions by letting the air gently out of the bubble before it bursts; (3) a combination of (1) and (2); (4) the Fed doesn’t know what it is doing and is triggering recessions by mistake; or (5) a combination of (3) and (4).

I’m going with (5). Thus worrying about “inversions” and “ranges of inversions” is akin to looking at clouds and wondering if it is going to rain on your parade.

“You make it sound like the US is already in recession.”

I don’t know if the US is in recession or not. It could be and would not surprise me.

The next couple of jobs reports may provide a clue. Then again, I have been pondering for a very long time, the notion that job losses will be minimal in the next recession. Why? Overexpansion. It takes a minimum number of people to staff stores no matter the level of business.

We’re likely not in a recession now. Yield curve inversion precedes recessions by many months. For instance, it inverted starting in July 2006, nearly 1.5 years before the 2007 recession. It also inverted in July 2000, 9 months before the 2001 recession; and May 1989, 14 months ahead. The inversion also has to be sustained. If it’s a short-lived inversion, there may not be a recession yet

Who’s worried? I’m in 10 yr treasuries. 🙂

Doesn’t the 3 month with a lower rate than the one month suggests at least some chance of a Fed cut in the next three months? If it does, I wonder what that chance is.

RECESSION. One is long overdue. Hopefully it will curb this addiction to debt and make everyone more responsible with regards to borrowing money, including government at all levels.