Economists expected a rebound in housing this month so they are no doubt shocked by the Housing Residential Sales report.

New Home Sales

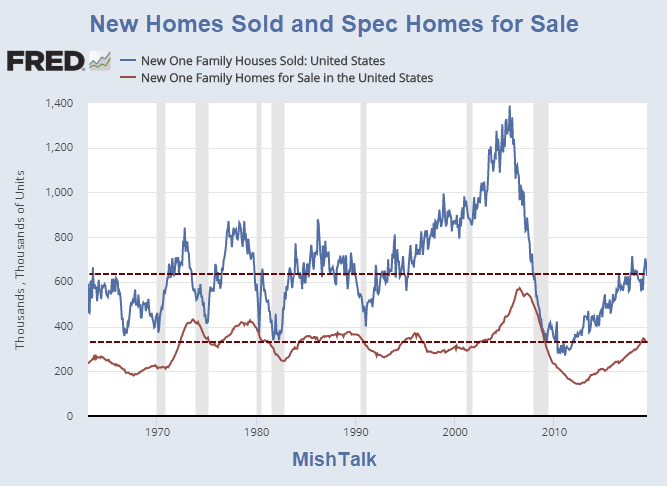

Sales of new single‐family houses in May 2019 were at a seasonally adjusted annual rate of 626,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 7.8 percent below the revised April rate of 679,000 and is 3.7 percent below the May 2018 estimate of 650,000.

Sales Price

The median sales price of new houses sold in May 2019 was $308,000. The average sales price was $377,200.

For Sale Inventory and Months’ Supply

The seasonally‐adjusted estimate of new houses for sale at the end of May was 333,000. This represents a supply of 6.4 months at the current sales rate.

Expectations

The Econoday consensus estimate was 680,000 units at a Seasonally-Adjusted-Annualized Rate (SAAR). 626,000 missed the mark by about 8%.

Econoday notes price data fell sharply, down 8.1 percent on the month to a median $308,000. Year-on-year, the median is down 2.7 percent and right in line with the 3.7 percent decline in sales.

Econoday’s closing remark is worth noting: “For the Federal Reserve, the sudden downturn in May new home sales coincides with their concern over recent weakness in other parts of the economy, namely business investment, and adds further to the odds for a July rate cut.”

New Homes by Region

Volatility

This report shows intense regional volatility. There may be huge revisions in the West, or other regions lower.

Supply

Home builders sit on 333,000 new homes for sale. This represents builder speculation. But where is it?

333,000 is a national number. The report does not break down the supply by region. If the West has huge oversupply, those builders are in trouble.

Attitudes

New home sales are below where they were in 1965.

Affordability and attitude changes by milennials towards the “ownership society” and family formation are the key reasons sales have gone nowhere.

When the Fed bailed out the banks and mortgage holders, it did so at the expense of the ascendant generation who now cannot afford homes and luxuries their parent did.

For a discussion of attitudes and blame, please see Millennials, the Screwed Generation, Blame Boomers For Making Their Lives Worse.

Mike “Mish” Shedlock

Correction, I do see how they were affected, I just don’t think it’s as big a deal as others make it. I think it has more to do with their attitudes towards work and entitlements. Not saying all, but they are now the majority.

I don’t see how the Fed bailout of the banks and mortgage holders affected the Millennials affording a house or luxuries?

“There may be huge revisions in the West, or other regions lower.”

I would not be surprised to see revisions higher. The pending new construction numbers from the largest new home market in the country certainly don’t match up with this Census report. DFW saw a 27 percent YoY increase in pending new home sales activity, and closed sales of new construction were up 11 percent in May. Houston also saw 10% bump in pending overall sales. Reasonable assumption that new construction was a contributor to that jump. Here in Texas it’s the resale market which is not keeping pace because sellers are not able to adapt to the shifting market and demand for more affordable homes.. link to aaronlayman.com

This is actually very frightening

“There is little to like in today’s residential sales report. New home sales dove 7.8% overall and prices also fell 8.1%.”

The only “little to like” about 8% cheaper housing, is that it wasn’t 80%.

“It’s hilarious that with the lowest interest rates, & lowest unemployment rate in history that millenials are crying that they can’t ‘afford it’. “

There is nothing hilarious about this. They genuinely cannot afford homes. On top of it, attitudes have changed. And yes, Obamacare screwed them further.

Sheeesh

So what is your solution to this?? Last time I checked housing prices and rents are dictated by supply and demand.

On Long Island and in Westchester County NY where it is well known that property taxes are some of the highest in the nation along with sales tax of over 8.8%, high commuting costs and tolls prices and sales have reached new highs each month in 2019.

Since the economy and job market are booming the population and businesses is pretty much fine with higher taxes and increased government spending despite the hyperbole and histrionics on talk radio and in these forums

“When the Fed bailed out the banks and mortgage holders, it did so at the expense of the ascendant generation who now cannot afford homes and luxuries their parent did.”

BINGO!!!

A major source of discontent in the western world that really is not discussed as such.

The regions with the worst declines are also the ones with the highest taxes; therefore, affected most by the limits of local and state taxes when itemizing the Federal tax retrun.

Uh real estate (and the overall economy) is still booming in the greater Boston & greater NYC metropolitan areas.. If you check actual figures from the MLS in Massachusetts, Long Island & NYC areas you will see double digit INCREASES in sales each month in 2019 vs 2019.. And single family homes are selling for 100.7% of asking price according to the Massachusetts association of realtors, and in Nassau county on Long Island (where property taxes are high but have been high for years) both median & average sales price hit a new high during this same reporting perios.

I can’t understand how some people can damn an entire population and their future by this rampant debt, home prices, and student loans.

The future depends on having children, and at a certain point the human body just can’t have children.

Millennials still want the same as other generations, they just can’t afford it.

“Millennials still want the same as other generations, they just can’t afford it.”

Consequently, just the (few) rich millenials and those that don’t give a crap about taking out loans they know they will never repay are the ones breeding from that generation. Nice set up for the country and western world at large for that matter.

Its hilarious that with the lowest interest rates, & lowest unemployment rate in history that millenials are crying that they can’t ‘afford it’. Playing victim & blaming others as expedient and politically popular it may be never made anyone rich save for a few poverty pimps like Al (call me reverend) Sharpton. Millenials can’t afford stuff because basically they are financial idiots — you also don’t get wealthy by spending over $1200 a year on a smartphone (that depreciates faster than a new car) and racking up high interest credit card debt eating out every night & using uber… At least now on a credit card statement they tell you how many years it will take to pay off a likely five figure credit card balance

Californians don’t need to buy homes. They park their sex robot in the closet.

New home sales for the first 5 months of 2019 are up 4% from 2018. One oddball month of data is really much ado about nothing.

You better check your stats again.

A deflationary collapse is finally here. I hedged for this a few years ago. Banks are looking like a good candidate for major shorting. I have no sympathy for the banks that made capital to accessible to poor credit risks or for those people who bought houses with little down payment. The hell with them all. Maybe this time around they will both learn to be more prudent.

In having no sympathy for them, keep in mind that Federal Regulations required them to lend to poor credit risks.

Greenspan took the lending standard to ZERO. He was warned within the FED in 2000, that the standard was too loose. As Krugman noted, Greenspan needed a housing bubble to recover the economy from the .com bubble. Thus Greenspan didn’t tighten lending standards, which he had congressional authority to do.

Bush Jr. then announce the Ownership Society program, which was not a coincidence.

In 2005, Greenspan praised bankers for getting people into homes they otherwise could not afford. In September 2004, the FBI warned congress of major mortgage fraud. I would think that Greenspan was aware of that fact when he praised the bankers.

“The hell with them all. Maybe this time around they will both learn to be more prudent.”

Know they won’t learn, as its intentional and part of the game that’s been played for centuries.

I meant to write “No they won’t learn”, but both spellings seem to work.

Since the Russian hoax was the biggest faux story over the last two year, one would think that it would be an even bigger story for a private company to try an rig an election. Yet, still nothing but crickets –

Millennials should blame the gov’t. Specifically liberal policies. Everyone should own a home and get a college education and the best way to accomplish this is to provide loans for everyone. Regardless of their ability to repay. Colleges could charge way more knowing people could pay by borrowing money from Sallie Mae. The same happened in housing because of Freddie Mac and Fannie Mae. Without these GSEs, education and housing costs would be far lower.