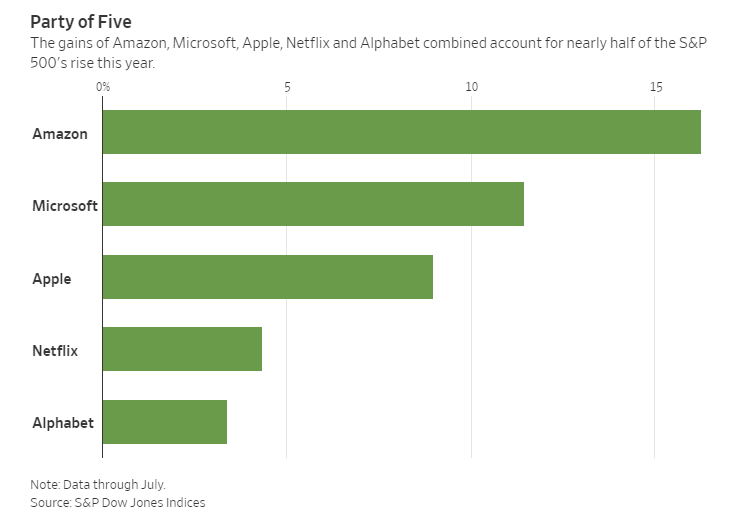

After slim profits, or losses, in many quarters, Amazon is the single-biggest driving force behind the S&P 500’s more than 6% gain in 2018.

Amazon, Microsoft, Apple, Netflix, and Alphabet (formerly Google) account for nearly half of the gains of a group of 500.

Amazon is no bargain, but Investors Keep Buying.

>Shares of companies like Amazon.com Inc., Netflix Inc. and Salesforce.com Inc. – have surged this year, driving the stock market higher but also pushing valuations to what some investors consider worrisome levels.

>The valuation of the average stock in the S&P 500 is now in the 97th percentile of historical levels, according to Goldman Sachs Group Inc., which analyzed 40 years of market pricing and valuation data. The valuation level is thanks in large part to the rise of high-flying tech stocks.

Crowded Trades

Purported Forward P/E Ratio

That chart from the article is a joke.

Not only does it presume earnings estimates will continue rising indefinitely, it is also pro-forma nonsense that ignores alleged “one time” costs that seen to occur with regularity.

Shiller Smoothed P/E Chart

This is the second most overvalued market in history according to the Shiller P/E Ratio.

Obviously this is not a timing mechanism but it is a monster big warning symbol.

New Ways of Thinking

To believe in this market requires new ways of thinking.

>“I don’t talk about multiples. That’s where the conversation stops,” Jonathan Curtis, a portfolio manager at Franklin Templeton’s Franklin Equity Group, says of discussions with others about tech companies. “I tell them, ‘Help me understand what this business looks like at maturity.’”

>He and others argue that investors have to take a longer-term view of high spending that depresses short-term profits, and so leads to elevated price/earnings multiples.

In other words, it’s different this time (until it isn’t). The reasons change, the end result won’t.

Mike “Mish” Shedlock

“To believe in this market requires new ways of thinking.”

Such as allowing banks to lie about the value of their assets? Such as rigged bank stress tests? Such as stating that banks are not financial services companies, in order to qualify them for a particular tax cut?

Formally, it requires is a mechanism for transferring an ever increasing share of the economic value created by those who perform productive work, into the hands of those who own shares.

Persistent, and ever increasing debasement of earnings, accompanied with obfuscating headfakes such as the CPI to fool the dumb, has done the heavy lifting so far. Along with made-up “property” classes and “protections” that the government and legal system supposedly “need” to enforce, and which facilitates the rent seekers charging the productive ever increasing unearned rent.

As things get tighter, and getting blood from ever more barren stones gets tougher; an acceleration in status of the security apparatuses, aimed at making the peasants work harder for less, and be less tempted to get uppity about their situation; will pick up steam as well. Along with inventions of new tradeable “property”, such as body parts, children, sexual favors etc. Peasants got to service “their” debt in something after all….

The end goal being that those who work, gets paid subsistence against working as hard as they can. Those who “own”, don’t have to work. And those in the middle, security apparatus, class, are elevated high enough above the workers, to buy their loyalty. Think Shogunate, Samurai and peasantry. Or Kings, Knights and ditto.

“That chart from the article is a joke. “

Really, everything is a joke. The DOW collapsed 89% in 1929-32.

On Wednesday, this becomes the longest bull market on record. The FED has run negative real rates for a record 123 months. Interest rates have been the lowest in 5,000 years- since the dawn of civilization. The meter is on TILT.

Meanwhile, the G20 has changed the rules for depositors. Obviously, something is very out of whack, if the Big 20 are unanimously changing the rules for depositors.

What is behind the curtain, that is being hidden from us? What is the financial calamity they are expecting and preparing for?

To make indentured servitude more formal than it currently is. After all, the peons “owe” the banksters money. With loans they “voluntarily” took out to for the right to use the air they where breathing, from those who were granted a license to manage the air. So now, the peons have to work off their debt. That’s only fair.

Besides, it’s not as if the peasantry is in any better position to do anything about that now, than they were under Louis IVX. Ever larger military budgets, and ever more militarized police apparatuses ostensibly to protect “us” from the horrors of virginity, for the King. Accompanied by a peasantry so dumb and indoctrinated, they even beg the King to disarm their fellow peasants even more thoroughly than he already has. So, pretty easy pickings there.

With Party of 5 making up more than 50% of the index rise this year, I wouldn’t be surprised if the plunge protection team supports them instead of the entire market.

Ding, ding, ding!

Winner, winner, chicken dinner.

One thing that seems different to me this go around for the markets in general is that there seem to be way more bears. I actually have a harder time finding bullish people then bearish people. 1999 and 2006 there were far fewer bears IMO, especially really, really negative bears. Or maybe since I was younger and there was less internet info, I just didn’t know the bears back then.

This cycle is the first market cycle that has really been fully accompanied by so many economic blogs, alt news sites, economic podcasts, newsletters, etc. This may create a lot of bear group think. In 1999 most people just had CNBC and the Wall Street Journal….maybe a few snail mail newsletters. When I listen to a panel of fund mgrs, RE private equity folks today, etc….everyone talks about what they are doing in case of a downturn, how they know we are late in a cycle, etc…. And many fellow investors I know constantly fret about a coming crash. I did not feel that much of a fear sentiment in 1999 and 2006. Especially 1999 seemed a lot more euphoric across the board.

I don’t know if this will mean anything for what comes next, as I count myself as a bear (and have been for a long time!). But just an observation. Its rare that so many people predict a crash before it happens.

The markets have never been so divorced from regular people either. Optimism isn’t taking root with Joe Sixpack for myriad reasons.

Put another way, what’s good for Wall St is no longer good for Main St. To have a nearly decade-long recovery with so little benefit for the average guy is stunning, and by now everyone has noticed that something is very wrong somewhere.

When we finally do get this coming crash/recession, it will be one of the most telegraphed, and well predicted crash/recessions in world history! Predicted annually since 2009!

It SHOULD have been predicted since 2009. The last crisis was huge and we did nothing to address the underlying structural problems, instead declaring firms TBTF and bailing everyone out with no charges filed against those responsible. We rewarded bad behavior on a massive scale, ensuring that another crisis would be in the works soon.

Thank asks about Etf influence and mntgoat bear attitudes.

I’m thinking etf buying by the uninformed contributes massively.

If that goes into reverse all he’ll will let loose.

Smaller cap, well valued will be left standing.

Question – is there a weakest link identifiable, that if breaks or turns, will cause an avalanche? One stock with an Achilles heel?

“One thing that seems different to me this go around for the markets in general is that there seem to be way more bears. I actually have a harder time finding bullish people then bearish people.”

People have been twice burned (2000 and 2007) and know the truth about the market. In 1999, people didn’t know the truth.

Where is the big bull market? One place, the U.S. The rest of the world isn’t going along for the ride.

The market is divorced from reality and some day reality will catch up with it, just as it did in 1929.

To much greater extent than in ’99, stock ownership is now concentrated amongst the bailed out classes. It’s much easier to be optimistic, when the Fed and government have signaled very clearly, that they will throw each and every non-stock-owning demographic under the bus and on the bonfire, in order to keep stock owners from taking more than a nominal loss.

Anecdotally this rings true – but positioning data are saying the exact opposite. Never have investors been more lopsidedly positioned for more upside with even remotely comparable leverage.